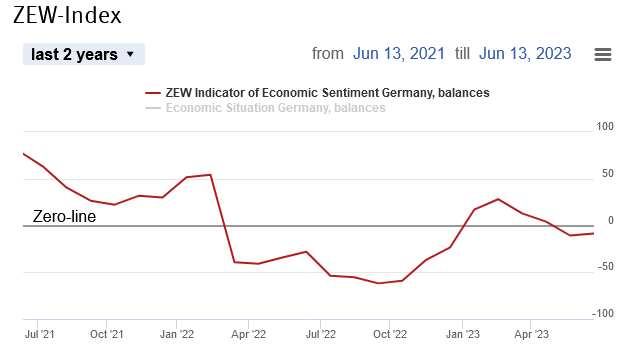

Germany ZEW Economic Sentiment rose slightly from -10.7 to -8.5 in May, above expectation of -14.7. Current Situation index, however, fell “very sharply” from -34.8 to -56.5, much worse than expectation of -40.

“The ZEW Indicator of Economic Sentiment shows a slight improvement, but it remains in negative territory. This means that experts do not anticipate an improvement in the economic situation during the second half of the year. Particularly, sectors focused on exports are likely to perform poorly due to a weak global economy. However, the current recession is generally not considered particularly alarming,” comments ZEW President Achim Wambach.

Eurozone ZEW Economic Sentiment dropped from -9.4 to -10.0, above expectation of -13.1. Current Situation index dropped from -14.4 to -41.9.

Eurozone balance for short-term interest rates stands at 72.3, indicating anticipated rate hikes. On the other hand, balance for short-term interest rates for the US stands at 16.6, indicating no change in interest rates.

Fed Daly: Appropriate to start tapering by later this year

San Francisco Fed President Mary Daly said, “by the end of the year, if things continue as I expect them to with the economy, then I would expect us to hit that ‘substantial further progress’ goal, threshold, by later this year and it would be appropriate to start dialing back” asset purchases.

Daly also noted that Fed has set a different, higher bar for rate hike. “If we should get there in the time frame of next year that would be a tremendous win for the economy,” she said, but “I don’t expect that to be the case.”