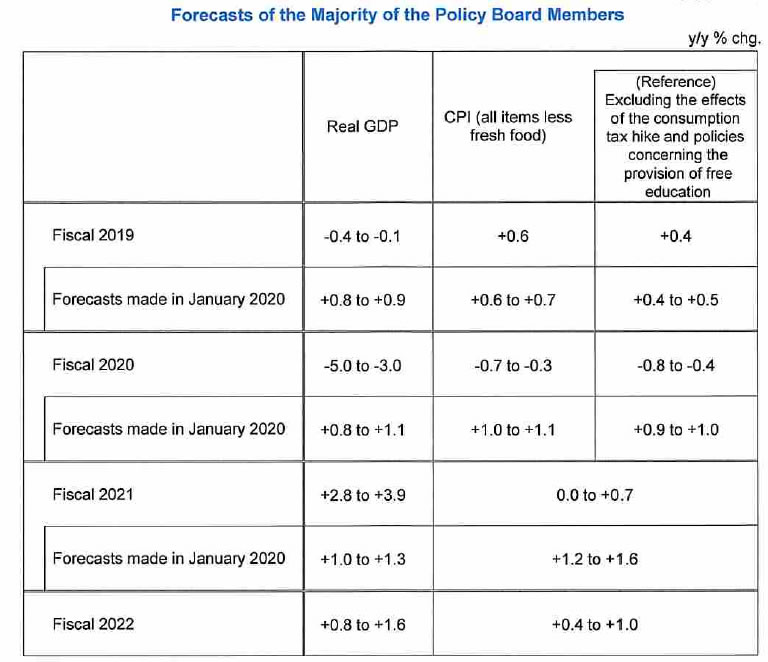

In the Outlook for Economic Activity and Prices, BoJ said the economy is “likely to remain in severe situation for the time being” due to the impact of the coronavirus pandemic. GDP could shrink as much as -5.0% to -3.0% in fiscal 2020. Japan could also return to deflation with core CPI down -0.7 to -0.4%. BoJ added that “future developments are extremely unclear” and risks to both economic activity and prices are “skewed to the downside”.

GDP growth forecast:

- Fiscal 2019 at -0.4% to -0.1% (down from 0.8% to 0.9%).

- Fiscal 2020 at -5.0 to -3.0% (down from (0.8 % to 1.1%).

- Fiscal 2021 at 2.8% to 3.9% (up from 1.0% to 1.3%).

- Fiscal 2020 at 0.8% to 1.6%.

Core CPI forecast (excluding sales tax hike effects):

- Fiscal 2019 at 0.4% (vs 0.4% to 0.5%).

- Fiscal 2020 at -0.7% to -0.4% (down from 0.9% to 1.0%).

- Fiscal 2021 at 0.0% to 0.7% (down from 1.2% to 1.6%).

- Fiscal 2022 at 0.4% to 1.0%.

China announces additional tariffs on 5207 US imports, valued at USD 60B, rates from 5% to 25%

More from China, the Finance Ministry announced the counter measures to US threat of imposing 25% products on USD 200B in Chinese goods. The State Council’s Customs Tariff Commission decided to impost additional levies on 5207 US products, totalling around USD 60B in value.

Additional 25% tariff will be imposed on 2493 products, additional 20% on 1078 products, additional 10% on 974 products and additional 5% on 662 products. The effect date is to be determined.

Here is the official statement in simplified Chinese.