BoC cut overnight rate target by -50bps to 1.25% and warned that “, the COVID-19 virus is a material negative shock to the Canadian and global outlooks, and monetary and fiscal authorities are responding.” The central bank “stands ready to adjust monetary policy further if required”.

The central bank added, globally, the coronavirus is a “significant health threat” to people “in a growing number of countries”. Business activity in some regions has “fallen sharply” and supply chains have been “disrupted”. As the coronavirus spreads, ‘business and consumer confidence will deteriorate, further depressing activity.”

For Canada, Q1 will be “weaker than the Bank had expected”. The drop in terms of trade will weigh on income growth. Business investment “does not appear to be recovering”. Rail line blockades, strikes by Ontario teachers and winter storms are also dampening activity.

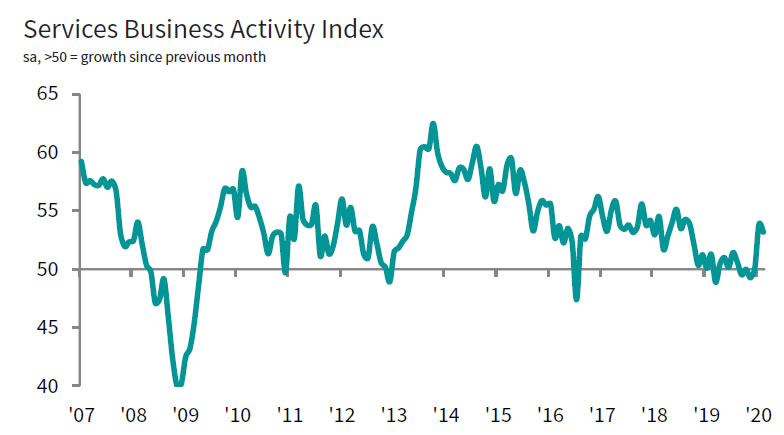

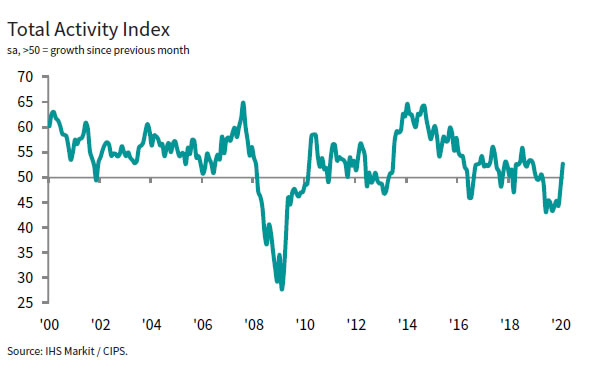

US ISM non-manufacturing rose to 57.3, corresponds to 3% annualized GDP growth

US ISM Non-Manufacturing Index rose to 57.3 in February, up from 55.5, beat expectation of 54.9. Looking at some details, production dropped -3.1 to 57.8. New orders jumped 6.9 to 63.1. Employment rose 2.5 to 55.6.

ISM said, “most respondents are concerned about the coronavirus and its supply chain impact. They also continue to have difficulty with labor resources. They do remain positive about business conditions and the overall economy.”

“The past relationship between the NMI® and the overall economy indicates that the NMI® for February (57.3 percent) corresponds to a 3-percent increase in real gross domestic product (GDP) on an annualized basis.”