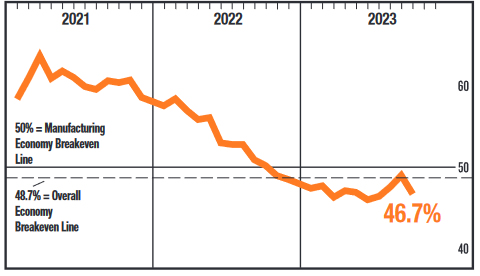

In an alarming development for the US economy, ISM Manufacturing PMI for October has nosedived to 46.7, a stark contrast from last month’s 49.0 and shattering expectations which had anticipated it to remain steady. This marks the twelfth month in a row where the PMI has stayed below the critical 50-point mark, signaling a contraction in manufacturing activity. This persistent downturn is reminiscent of the distressing times during the 2007-2009 Great Recession.

Digging deeper into the data, new orders saw a decrease, moving from 49.2 to 45.5. This now marks the 14th month where new orders have contracted. Production levels, too, experienced a decline, sliding from 52.5 to a borderline 50.4. Employment metrics were not immune either, plummeting from 51.2 to 46.8. However, there was a minor uptick in prices, which moved from 43.8 to 45.1.

The ISM’s statement offered some insight into the broader implications of this data. They pointed out, “The correlation between the Manufacturing PMI and the entirety of the US economy suggests that the October reading of 46.7 percent equates to a decrease of minus-0.7 percent in real GDP, when viewed on an annualized basis.”

Fed Evans: There’s benefits to adjusting tightening pace soon

Chicago Fed President Charles Evans said yesterday, “there’s benefits to adjusting the pace (of tightening) as soon as we can.”

“I’m hopeful that we’re getting to a point where the dynamics for inflation turning over and returning towards our 2% objective will be put in place, if not very soon, soon, and we’ll actually see it in inflation,” he said.

“If you don’t begin to think about adjusting the pace, taking account of lags, and you just keep increasing rates by a large amount every time you get a disappointing report,” then “next thing you know, you’re at a very high federal funds rate.”

“I’m going to continue to be nervous that, as we go higher than that, it could be that the economy is going to face more challenges, and that that could present risks on the ‘real’ side, the full employment mandate,” he said. “It’s a risk.”