Three major central banks – SNB, BoE and ECB – are set to announce their policy decisions. All three will keep their interest rates unchanged. This comes in the wake of Fed’s outlined plans for rate cuts in 2024 in the dot plot released overnight. Now, that raises questions about whether these central banks will follow and signal policy loosening for the next year.

SNB is expected to hold its key policy rate steady at 1.75%. This decision is supported by forecasts from Swiss State Secretariat for Economic Affairs released yesterday, projecting a slowdown in inflation to 1.9% in 2024 and further to 1.1% in 2025. Economic growth in Switzerland is also expected to decelerate to 1.1% in 2024 before rebounding to 1.7% in 2025.

BoE is anticipated to maintain interest rates at 5.25%. Traders have increased their bets on the BoE cutting rates following the unexpectedly sharp contraction in UK’s monthly GDP for October. The market has fully priced in 100bps easing in monetary policy for 2024, bringing borrowing costs down to 4.25%. The first rate cut is anticipated in June. Today’s voting pattern and accompanying statement from BoE will be under close scrutiny.

Similarly, the ECB is expected to keep its main refinancing rate at 4.50% and deposit rate at 4.00%. The focus will likely be on new DP and inflation forecasts and their implications for the rate path in the coming year. Money markets are currently pricing in almost 150bps of rate cuts for the next year.

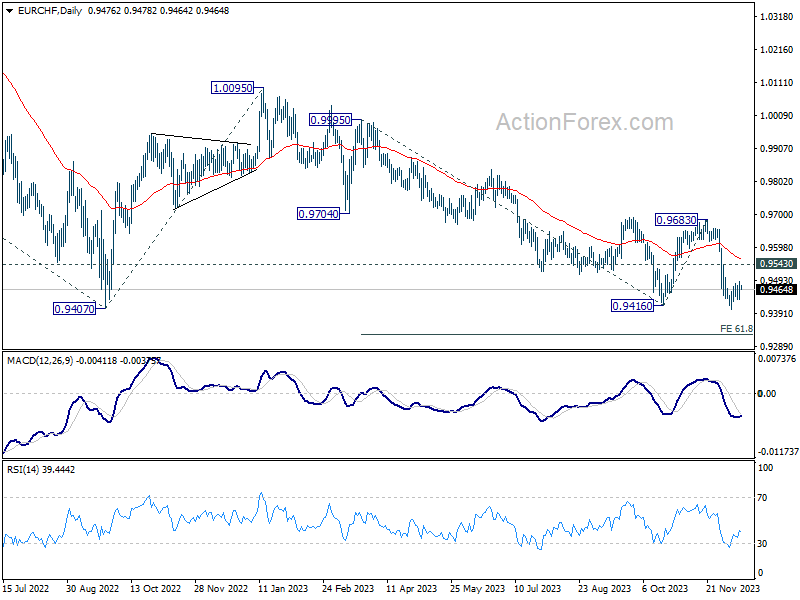

In terms of currency performance, Swiss Franc appears to be the firmer one for the near term. As long as 0.9543 resistance holds, outlook in EUR/CHF remains bearish. Decisive break of 0.9402 support will resume larger down trend to 61.8% projection of 0.9995 to 0.9416 from 0.9683 at 0.9325.

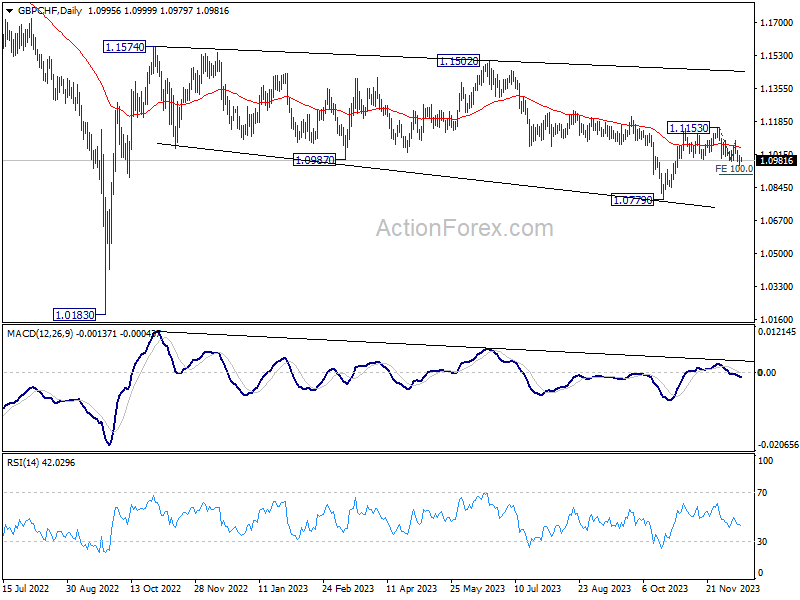

GBP/CHF’s fall from 1.1153 resumed this week, and should be on track to 100% projection of 1.1153 to 1.0978 from 1.1085 at 1.0910. Sustained break there could prompt downside acceleration to 1.0779 and below, to resume larger down trend from 1.1574.

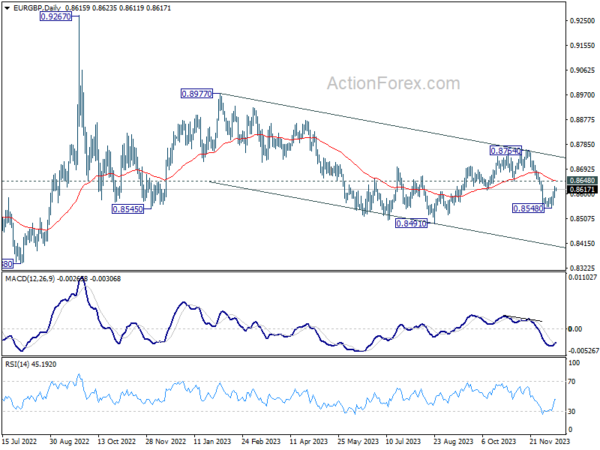

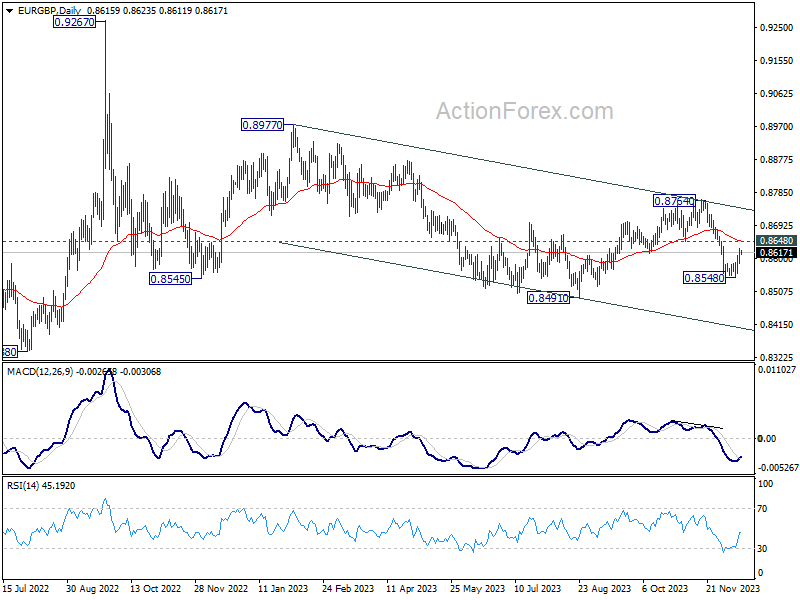

While Euro appears to be light strong then Sterling in the past few days, risk in EUR/GBP remains on the downside as long as 0.8648 resistance holds. Break of 0.8548 will likely bring deeper decline through 0.8491 to resume the medium term down trend.

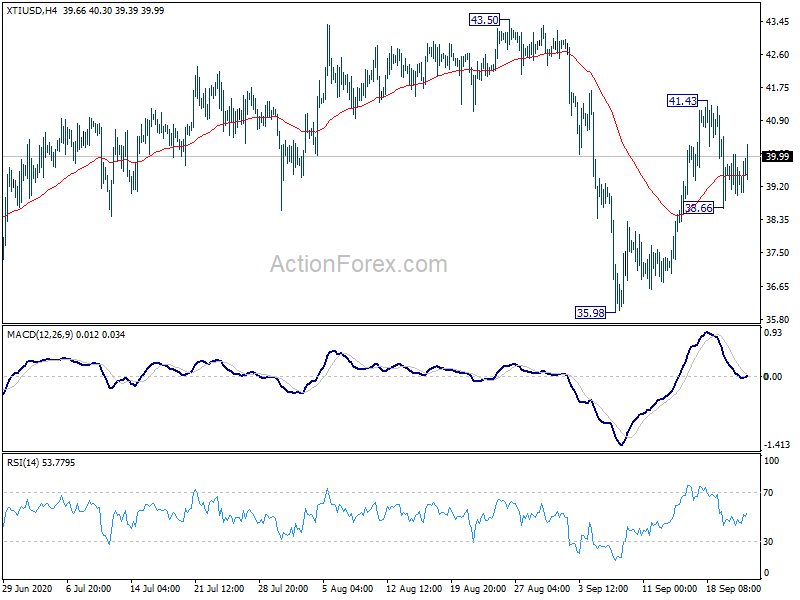

UK PMIs retreated, but still point to solid Q3 GDP rebound

UK PMI Manufacturing dropped slightly to 54.3 in September, down form 55.2, above expectation of 54.0. PMI services dropped to 55.1, down form 58.8, missed expectation of 56.0. PMI Composite dropped to 55.7, down form 59.1.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The UK economy lost some of its bounce in September, as the initial rebound from Covid-19 lockdowns showed signs of fading… It was not surprising to see that the slowdown was especially acute in services… Encouragingly, robust growth in manufacturing, business services and financial services has offset weakness in consumer-facing sectors, meaning the overall rate of expansion remained comfortably above the survey’s long-run average, which adds to expectations that the third quarter will see a solid rebound in GDP from the collapse seen in the second quarter.

Full release here.