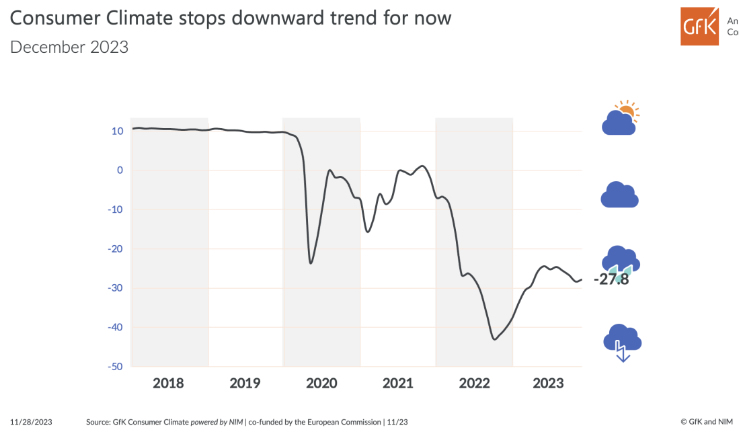

Germany’s Gfk consumer sentiment index for December showed a marginal improvement, rising from -28.3 to -27.8, slightly better than expected -28.5. This slight uptick indicates a subtle shift in consumer sentiment as the year ends.

In November, economic expectations had a minor increase from -2.4 to -2.3. However, income expectations dropped from -15.3 to -16.7. There was a slight rise in willingness to buy, from -16.3 to -15.0, while willingness to save decreased from 8.5 to 5.3.

Rolf Bürkl, consumer expert at NIM,noted that “after three consecutive months of decline, consumer sentiment is stabilizing as the year draws to a close.”

Despite this stabilization, Bürkl pointed out that consumer confidence remains at a very low level, with no indications of a sustainable recovery in the upcoming months. He emphasized that the overall mood is still “characterized by uncertainty and concern.”

UK CBI: Worrying falls in services volumes, profitability and employment

According to a CBI survey for the three months to August, UK business and professional services employment dropped at the quickest pace since 2009, with balance at -32%, down from -9%. Consumer services employment was even worse on record, with balance dropping from -31% to 063%. CBI added, “next quarter, employment is set to continue to fall, but the rate of decline is set to ease slightly.”

Ben Jones, CBI Principal Economist, said: “This quarter has shown some worrying falls in volumes, profitability and employment for the services sector. Although the pace of these declines is expected to ease, the impact of COVID-19 remains clear, with the services sector still facing challenges in terms of demand, revenues and cash flow… As we head into the autumn, the UK needs a bold plan to protect jobs as the job retention scheme draws to an end, to support the services sector.”

Full release here.