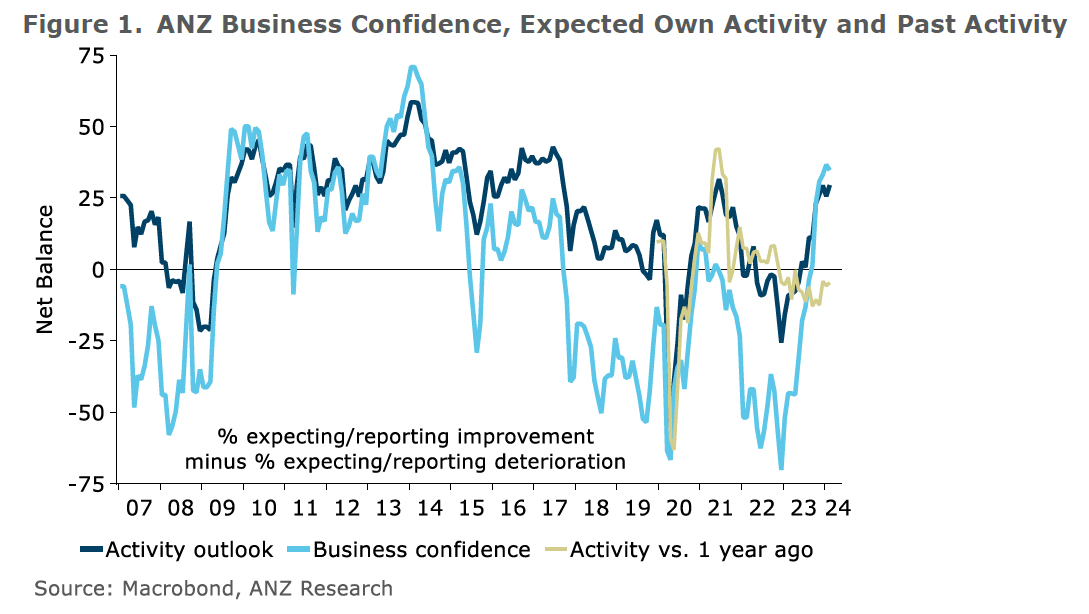

New Zealand ANZ Business Confidence fell from 36.6 to 34.7 in February. Own activity outlook rose from 25.6 to 29.5. Inflation expectations fell from 4.28% to 4.03%. Pricing intentions eased from 50% to 48%, continuing their sideways trend of recent months. Cost expectations fell from 75.6 to 73.5. Wages expectation fell from 81.4 to 78.9.

ANZ’s describes the economy as “patchy,” with visible “green shoots” in some sectors, yet acknowledges the “ongoing challenges” facing other segments. The survey does not imply the “economy is rolling over” or that “inflation has been beaten”.

Canada’s CPI accelerates to 2.9% yoy, driven by service sector price hikes

Canada’s CPI recorded a notable increase in May, climbing to 2.9% yoy from 2.7% yoy the previous month, surpassing the anticipated rate of 2.6%. This acceleration in headline CPI was primarily fueled by a significant uptick in service prices, which rose by 4.6% yoy in May, following a 4.2% yoy increase in April.

Diving deeper into the components, CPI median—which represents the midpoint of price changes—escalated from 2.6% yoy to 2.8% yoy, again outstripping the forecast of 2.6%. CPI trimmed, another measure that excludes extreme price movements, held steady at 2.9% yoy, also exceeding expectations of 2.8%. In contrast, CPI common, which reflects the common price changes across categories, slowed slightly from 2.6% yoy to 2.4% yoy, falling below the anticipated 2.6%.

On a monthly basis, the CPI rose by 0.6% mom in May, doubling the expected 0.3% mom increase. Similarly, the core CPI also increased by 0.6% mom, well above the forecast of 0.2%. This indicates a broader upward pressure on prices beyond just volatile categories.

Full Canada CPI release here.