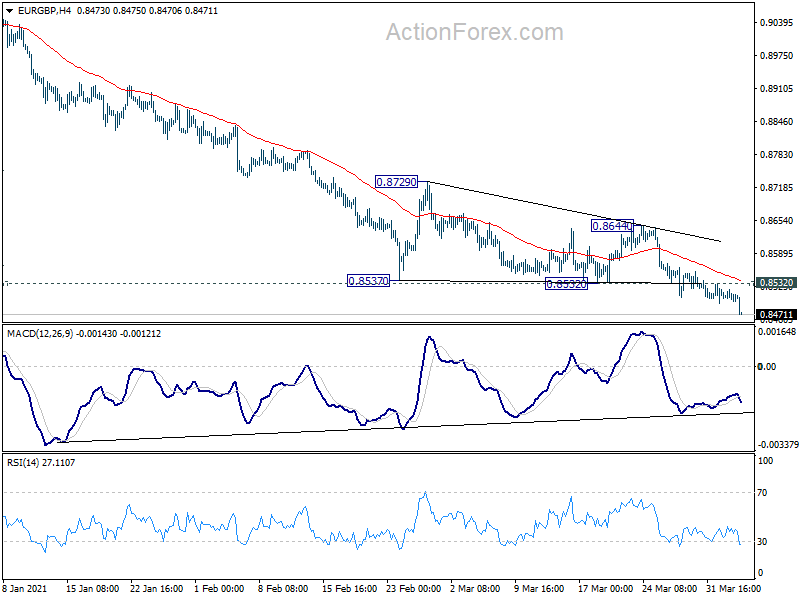

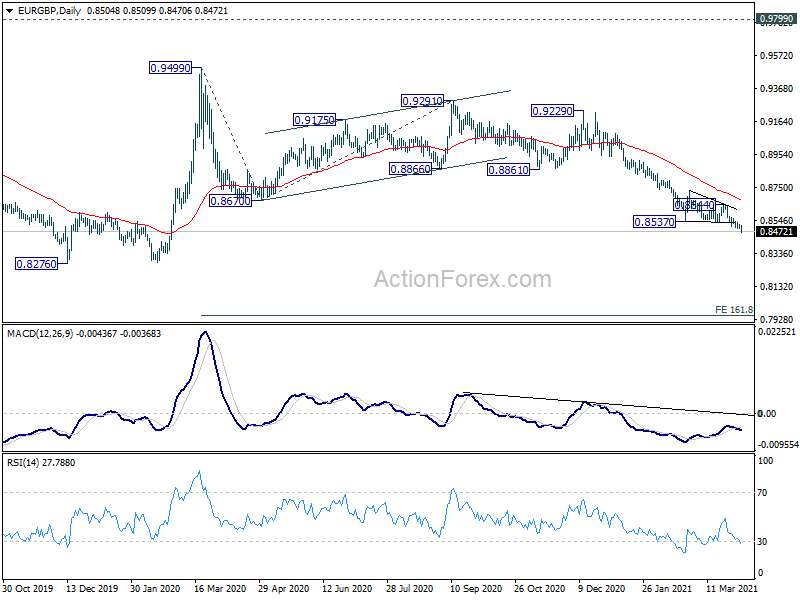

CAD/JPY lost momentum after after hitting 88.28 last week. But overall, outlook remains bullish as long as 86.05 support holds. Current up trend from 73.80 is likely reversing the down trend from 106.48. 91.62 long term resistance is the next upside target. Sustained break there will confirm long term bullishness.

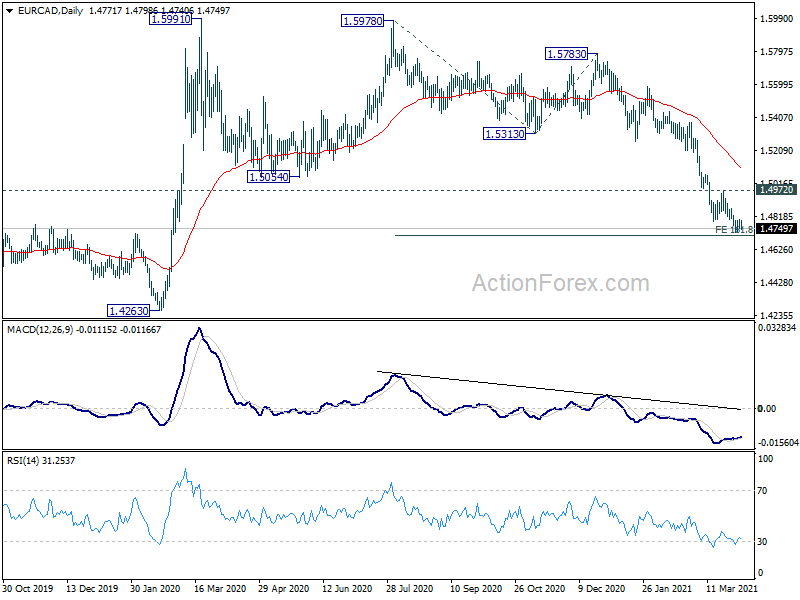

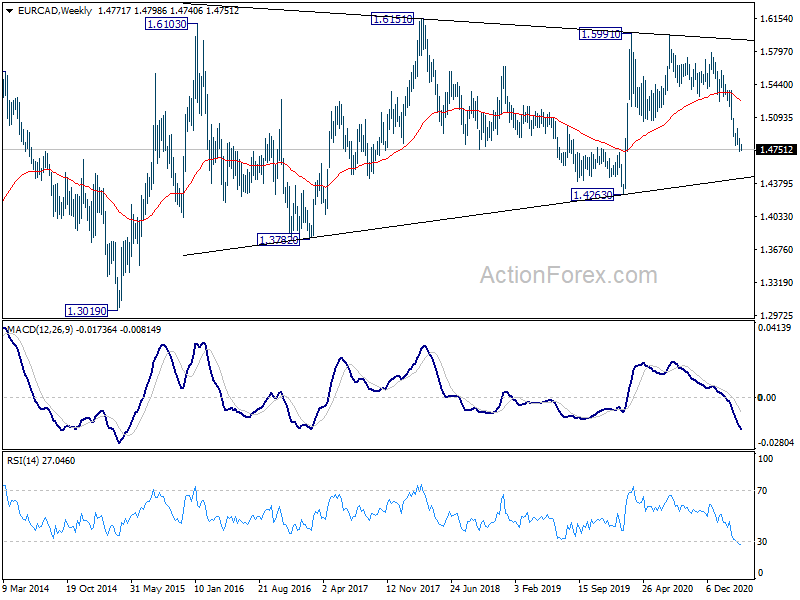

EUR/CAD also lost downside momentum after hitting 1.4737 last week. But overall, outlook stays bearishness with 1.4972 resistance intact. Focus is now on 161.8% projection of 1.5978 to 1.5313 from 1.5783 at 1.4707. Sustained break there will pave the way towards 1.4263 key support level. However, as current decline from 1.5991 could be just a leg inside the long term sideway pattern from 1.6103. We’d look for more signs of bottoming as it approaches 1.4623.

US ISM services rose to 63.7, corresponds to 5.1% annualized GDP growth

US ISM Services jumped to 63.7 in March, up from 55.3, above expectation of 58.5. Looking at some details, business activity/production rose 13.9 pts to 69.4. New orders rose 15.3 pts to 67.2. Employment rose 4.5 pts to 57.2. Prices rose 2.2 pts to 74.0.

ISM said: “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for March (63.7 percent) corresponds to a 5.1-percent increase in real gross domestic product (GDP) on an annualized basis.”

Full release here.