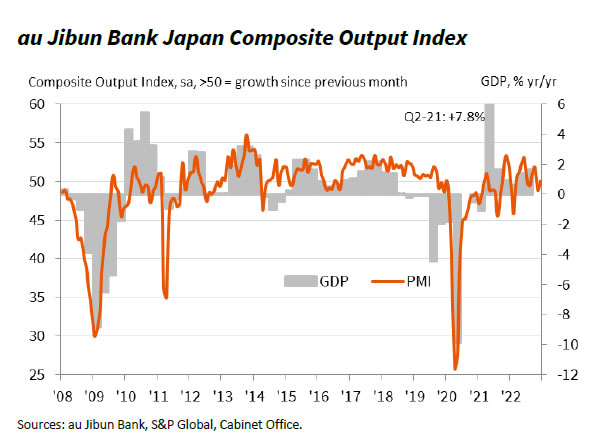

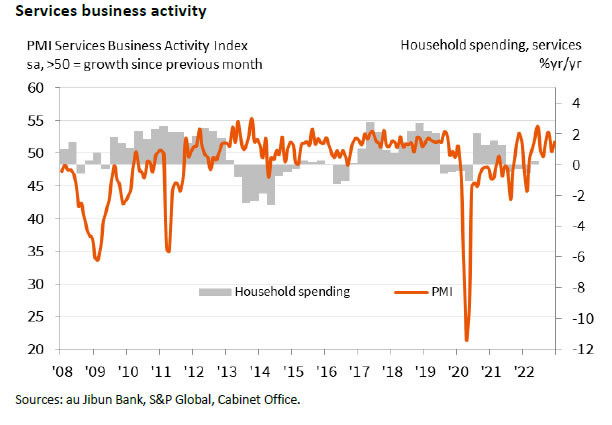

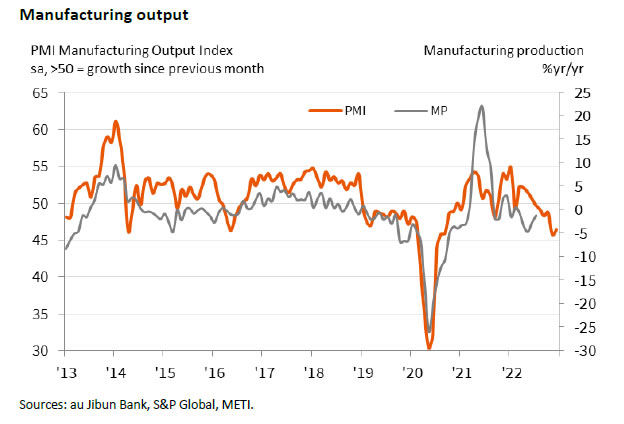

Japan PMI Manufacturing fell slightly from 49.0 to 48.8 in December, above expectation of 48.0. That’s the worst contractionary reading since October 2020. PMI Services, however, improved from 50.3 to 51.7. PMI Composite also rose back from 48.9 to 50.0.

Laura Denman, Economist at S&P Global Market Intelligence, said:

“The Japanese private sector economy saw a stabilisation in business activity in the final month of the year, with flash data indicating that the divergence between the manufacturing and services sectors has grown further. As has been the case since the launching of the National Travel Discount Programme in October, service providers have reportedly continued to profit from a boost in tourism volumes. Notably, firms have seemingly gained some pricing power as a result of improving demand within the sector and raised their selling prices at the sharpest rate since October 2019.

“Conversely, manufacturing firms continued to struggle in the face of subdued demand conditions and severe inflationary pressures with the latest flash PMI reading the lowest since October 2020. December data saw production and order books at Japanese manufacturers contract further, but at paces that were slower than in November. At the same time, though historically sharp, inflationary pressures cooled with the rate of input price inflation at the lowest level since September 2021.”

Fed’s Bowman flags energy as potential setback to disinflation progress; advocates more hike

Fed Michelle Bowman has made her hawkish stance clear on the pressing issue of inflation that continues to grip the US economy. In a speech today, Bowman emphasized the persistence of inflationary pressures, signaling the need for a more restrictive monetary policy to anchor inflation back to the Fed’s 2% target.

“Inflation continues to be too high, and I expect it will likely be appropriate for the Committee to raise rates further and hold them at a restrictive level for some time to return inflation to our 2 percent goal in a timely way,” Bowman stated.

Bowman pointed to the latest inflation reading based on the PCE index, noting a rise in overall inflation driven, in part, by escalating oil prices. “I see a continued risk that high energy prices could reverse some of the progress we have seen on inflation in recent months,” she warned.

Also, Bowman cited the Summary of Economic Projections released during the September FOMC meeting, where “the median participant expects inflation to stay above 2 percent at least until the end of 2025.” This expectation of prolonged inflationary pressures aligns with Bowman’s perspective that “further policy tightening” will be instrumental in steering inflation back towards target.

Full speech of Fed Bowman here.