Live Comments

Australia Westpac consumer sentiment dips -2.6% mom after RBA hike, but impact contained

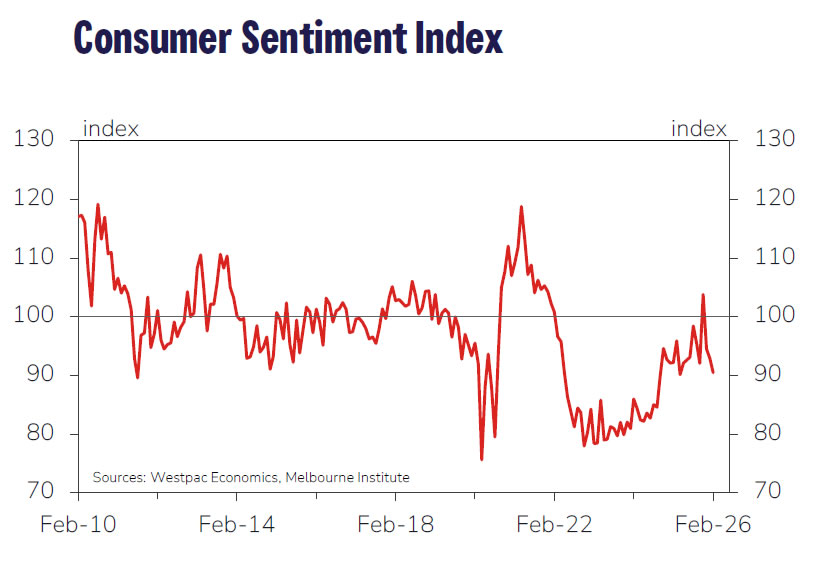

Australia’s Westpac Consumer Sentiment Index fell -2.6% mom to 90.5 in February, reflecting the immediate impact of the RBA’s first rate hike in more than two years. However, Westpac noted that the overall hit to confidence was "relatively mild" by historical standards. The February decline was smaller than the average fall typically seen after rate hikes, and sentiment remains well above the extreme lows recorded through much of 2022–2024.

Looking ahead, Westpac expects the RBA to remain cautious. While another hike at the March meeting cannot be ruled out, the more likely outcome is a pause as policymakers wait for additional data, particularly quarterly inflation updates.

With the RBA placing greater weight on trimmed-mean inflation and the next quarterly CPI report due in late April, Westpac continues to see May as the more probable window for a follow-up 25bp rate hike if inflation remains uncomfortably high.

Lagarde, Nagel reinforce ECB pause as medium-term inflation anchors hold

ECB President Christine Lagarde reiterated overnight that the Governing Council remains comfortable with its current policy stance, telling European lawmakers that inflation is still expected to stabilise at the 2% target over the medium term. In an environment marked by elevated uncertainty, Lagarde stressed that a "data-dependent, meeting-by-meeting approach to monetary policy serves us well."

That message was reinforced by Bundesbank President Joachim Nagel, who said “many factors” point to the current level of interest rates being appropriate. Nagel downplayed recent inflation softness, arguing that the shortfall is "small, temporary deviations", while medium-term inflation dynamics remain firmly aligned with the ECB’s target.

Nagel emphasised that policy action would only be warranted if medium-term inflation expectations deviated “sustainably and noticeably” from target — something he said is clearly not happening.

Eurozone Sentix jumps to 4.2, growth hope without inflation alarm

Eurozone investor confidence showed notable improvement in February, with the Sentix Investor Confidence Index rising from -1.8 to 4.2, above expectations of -0.2 and marking the highest reading since July 2025. The improvement was broad-based. Current Situation Index climbed from -13.0 to -6.8, its strongest level since April 2023. Meanwhile, Expectations Index rose from 10.0 to 15.8, also the highest since last summer, pointing to growing belief that the worst of the downturn has passed.

Sentix described the data as a “silver lining” for the Eurozone economy, arguing that the recession phase has likely ended and an upturn is beginning. While private investors remain somewhat cautious, institutional investors appear to be turning decisively more optimistic, with professional expectations reportedly rising to +24 points.

Inflation concerns have not re-emerged despite volatility in commodity markets and firmer oil prices. Investors surveyed see little risk of renewed inflation pressure, a backdrop that should allow the ECB to maintain its current policy stance. Markets continue to expect monetary policy to remain mildly supportive, and "definitely do not anticipate a restrictive phase."