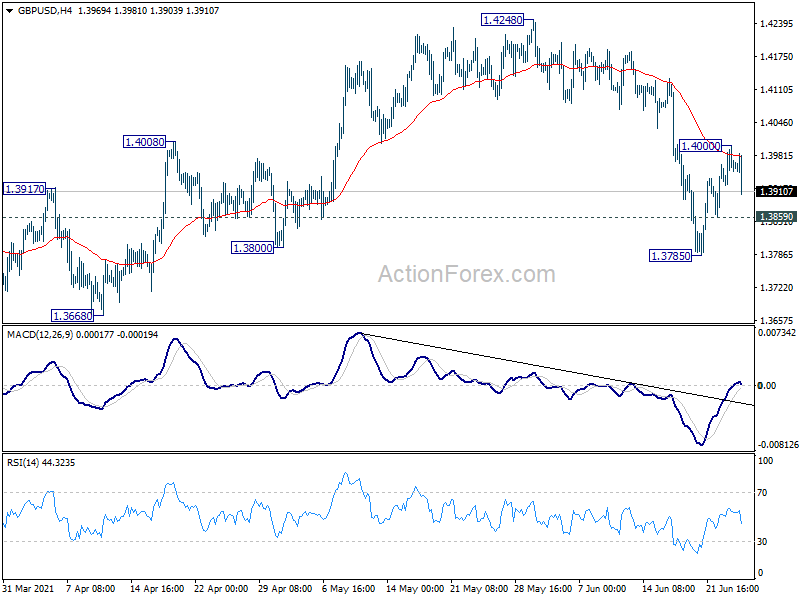

Dallas Fed President Robert Kaplan told Bloomberg News, “”As we make substantial further progress, which I think will happen sooner than people expect — sooner rather than later”.

“We’re weathering the pandemic, I think we’d be far better off, from a risk-management point of view, beginning to adjust these purchases of Treasuries and mortgage-backed securities,” he added.

“I’d rather start tapering, assuming we meet our conditions, sooner rather than later so that we have more flexibility in deciding what we want to do on rates down the road.”

“I think it’s a good thing for the Fed to emphasize that we’re vigilant and we’re committed to anchoring inflation at an average of 2% and that we’re committed to anchoring inflation expectations in a manner that’s consistent with 2% inflation,” Kaplan said. “I think just emphasizing that is probably a healthy thing.”

Kaplan expected one rate hike in 2022, without indicating his expectations for 2023.

Bundesbank Weidmann: PEPP must be ended when emergency is over

Bundesbank President Jens Weidmann said today that the “coming year would not be a crisis year if assumptions about the pandemic are confirmed.” Also, “PEPP must be ended when the emergency is over”.

He explained that the “preconditions” for ending net PEPP purchases are that “all major restrictions are lifted”, and the recovery is “solid”. Immediate measures should then be reduced in both the fiscal and monetary front.

Net PEPP purchases could be reduced “step by step” in advance.