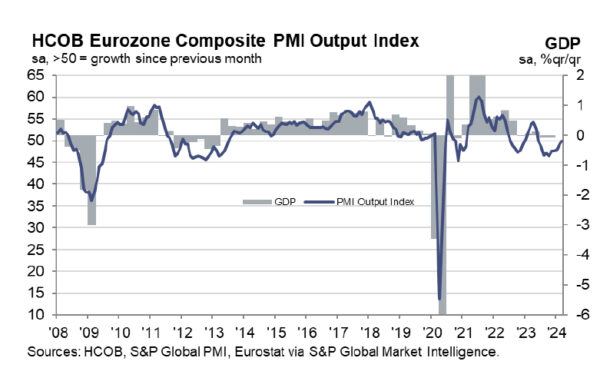

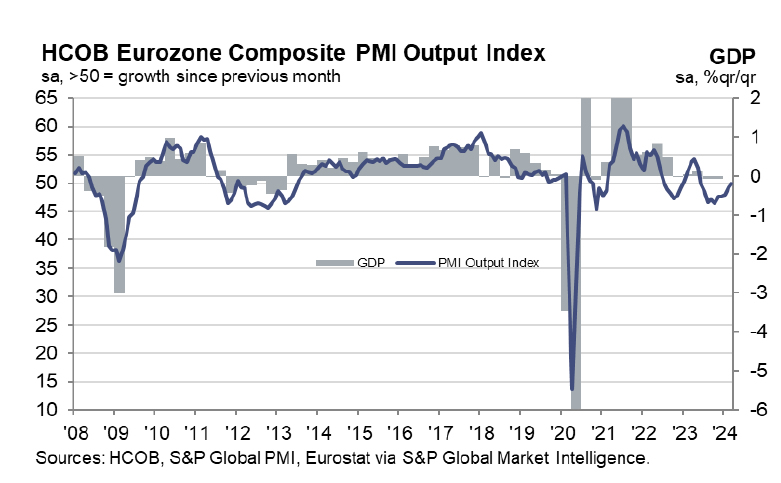

Eurozone PMI Manufacturing from 46.5 to 45.7 in March, below expectation of 47.0. PMI services, on the other hand rose from 50.2 to 51.5, above expectation of 50.5 a 9-month high. PMI Composite ticked up from 49.2 to 49.9, also a 9-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted the “clear weakness” in manufacturing, attributing it largely to Germany’s industrial performance. On a brighter note, the further expansion in the services PMI is considered a “positive development.”

From a monetary policy perspective, ECB may find some solace in the report’s implications on inflationary pressures. Notably, the services sector, which is typically sensitive to wage dynamics, has not seen a further escalation in price pressures.

However, these developments, as de la Rubia notes, are “not enough” to alter the ECB’s tentative plan to commence rate cuts in June, rather than an earlier move in April.

Also released, France PMI Manufacturing fell from 47.1 to 45.8. PMI Services fell from 48.4 to 47.8. PMI Composite fell from 48.1 to 47.7.

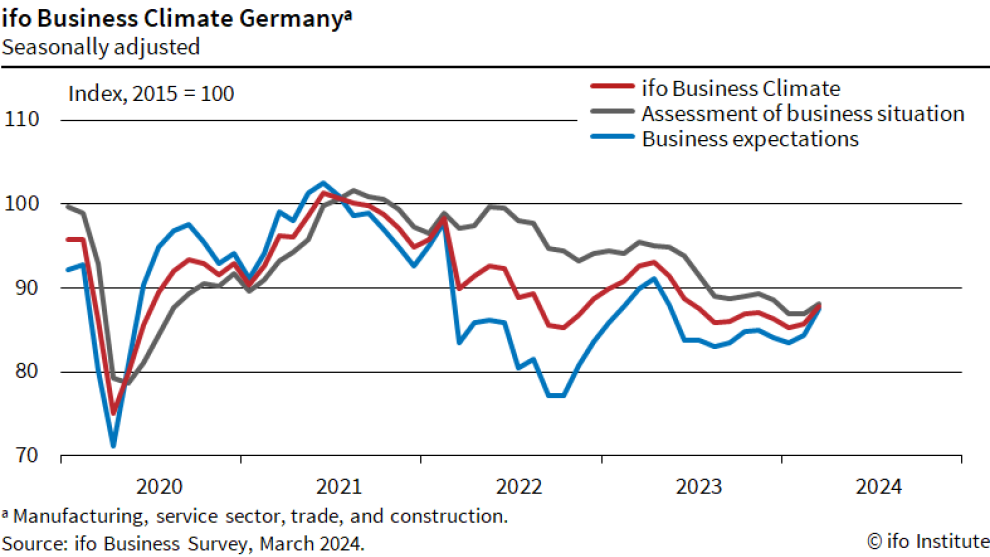

Germany PMI Manufacturing fell from 42.5 to 41.6. PMI Services rose from 48.3 to 49.8. PMI Composite rose from 46.3 to 47.4.

Full Eurozone PMI release here.

Fed’s Bostic eyes single rate cut in 2024, credits robust economy

Atlanta Fed President Raphael Bostic reiterated his anticipation just one interest-rate reduction within this year. Also, the first cut could happen later than previously envisioned, as Fed can “afford to be patient” as long as the economy holds up.

Bostic’s noted that as long as the economic indicators—such as GDP growth, employment rates, and business activity—remain robust, “I’m not in a hurry to get inflation down to 2%.”

“If it continues on a trajectory, I’m happy with that,” he added.