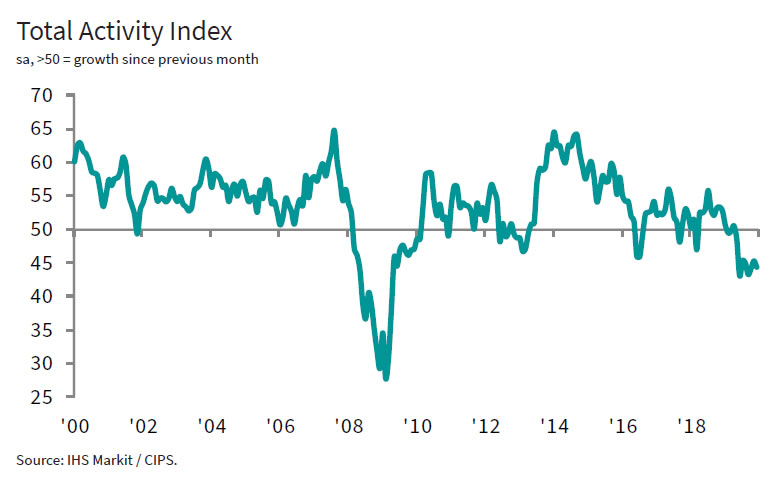

UK PMI Construction dropped to 44.4 in December, down from 45.3, missed expectation of 45.7. The index has been below the 50 no-change mark for the eighth consecutive month. It’s the longest period of contraction for almost a decade. Markit added there was the sharpest fall in civil engineering activity since March 2009. New business decreased for the ninth month in a row. Input cost inflation eased to the lowest level since February 2010.

Tim Moore, Economics Associate Director at IHS Markit, which compiles the survey:

“December data suggested that the UK construction sector limped through the final quarter of 2019, with output falling in all three major categories of work. Brexit uncertainty and spending delays ahead of the General Election were once again the most commonly cited factors highlighted by firms experiencing a drop in construction activity.

“Civil engineering saw its sharpest decline for more than ten years and remained the worst-performing area of construction work, followed by commercial development. House building has been the most resilient category in recent months, but still declined overall during December.

“The forward-looking survey indicators provide some hope that the construction sector malaise will begin to recede in the coming months. Latest data indicated that the downturn in order books remains much less severe than the low point seen last August, which has already helped to bring employment numbers closer to stabilisation.

“Moreover, construction companies signalled that business optimism has recovered to its strongest for nine months. Survey respondents cited confidence that a more predictable domestic political landscape and clarity on Brexit could deliver a much-needed boost to clients’ willingness-to-spend in 2020.”

Full release here.

ECB revised down growth in inflation projections after easing

ECB’s GDP growth projections are revised to 1.1% in 2019 (vs 1.2% in June), 1.2% in 2020 (vs 1.4%) and 1.4% in 2021 (unchanged).

Eurozone’s slowdown in growth mainly reflects “prevailing weakness of international trade in an environment of prolonged global uncertainties which are particularly affecting the euro area manufacturing sector.” But services and construction show “ongoing resilience. Risk to growth “remain tilted to the downside” due to “prolonged presence of uncertainties, related to geopolitical factors, the rising threat of protectionism and vulnerabilities in emerging markets.”

HICP inflation projections are revised down over the whole projection horizon, “reflecting lower energy prices and the weaker growth environment.” HICP projections are at 1.2% in 2019 (vs 1.3% in June), 1.0% in 2020 (vs 1.4%), 1.4% in 2021 (vs 1.6%).