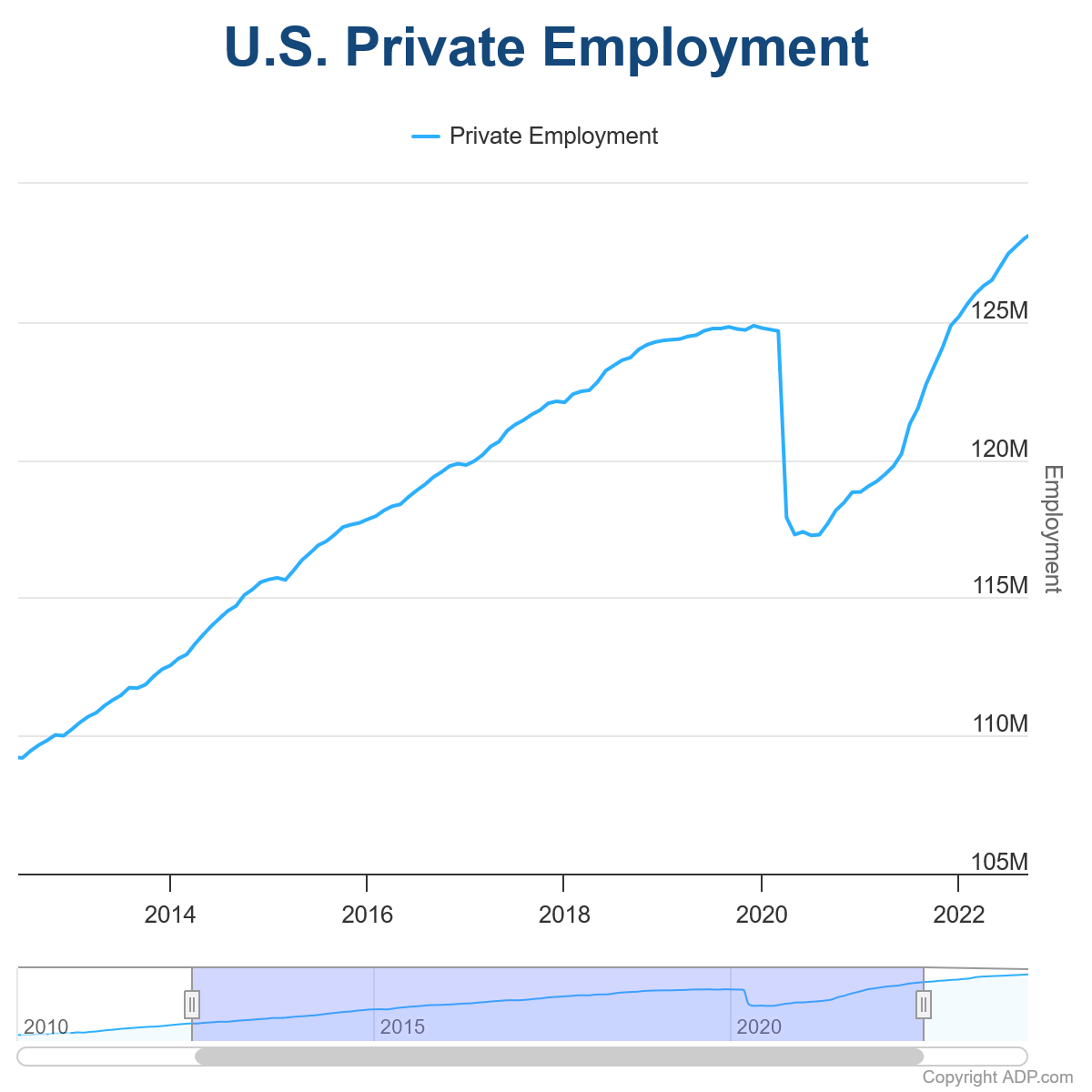

US ADP private employment grew 184k in March, above expectation of 150k. By sector, goods-producing jobs increased 42k while service-providing jobs increased 142k. By establishment size, small companies added 16k jobs, medium companies added 93k, large companies added 87k.

For job-stayers, year-over-year pay gains was unchanged at 5.1%. Annual pay growth for job changes accelerated sharply from 7.6% to 10.0%.

Nela Richardson, Chief Economist at ADP, said: “March was surprising not just for the pay gains, but the sectors that recorded them. The three biggest increases for job-changers were in construction, financial services, and manufacturing. Inflation has been cooling, but our data shows pay is heating up in both goods and services.”

Fed’s Bostic eyes first rate cut in Q4, citing sluggish inflation decline

In a CNBC interview today, Atlanta Fed President suggested that rate cuts could be on the horizon by the end of 2024, contingent on the economy’s performance. Bostic outlined a scenario where “continued robustness in GDP, unemployment, and a slow decline of inflation through the course of the year” could warrant a policy adjustment in the fourth quarter.

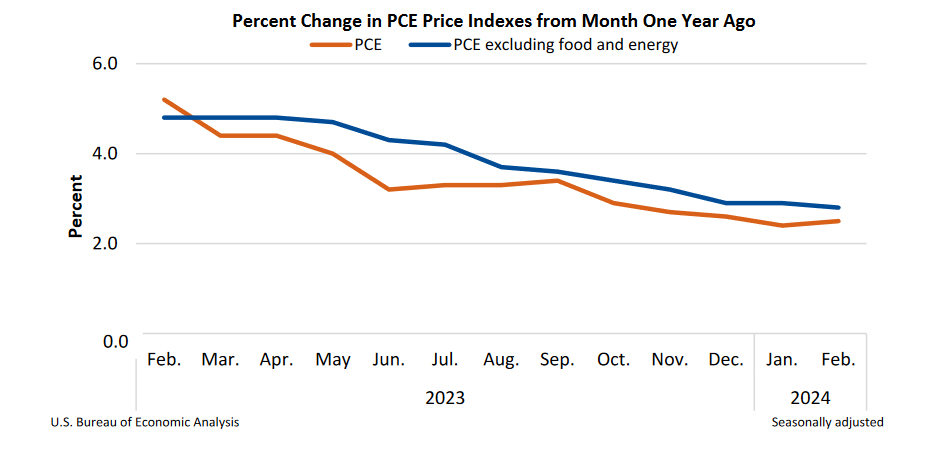

He also acknowledged the persistence of inflationary pressure into the current year, “hasn’t moved very much relative to” levels observed at the end of 2023. “There are some secondary measures in the inflation numbers that have gotten me a bit concerned that things may move even slower,” he warned.

“Those are much higher now than they were before and they’re starting to trend back to what we saw in the high inflation period,” Bostic added. “They’re moving away from what we’d like to see. So I’ve got to make sure that those aren’t hiding some extra upward pressure and pricing pressure before I’m going to want to move our policy rate.”