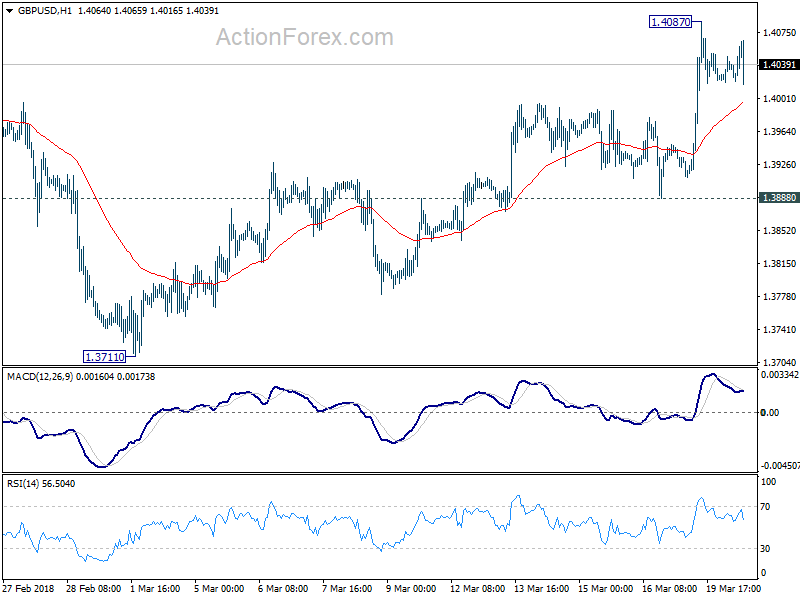

Entering into US session, Sterling is trading as the strongest one for today so far. Weaker than expected UK GDP triggered very brief retreat in the Pound. And Sterling quickly find its footing on Brexit optimism again. At the time of writing, Euro is the second strongest as Italian yield drops for another day. The selling climax in Italian bonds could have passed the climax for the near, possibly until credit agency rating actions. Dollar trades mildly high as consolidative price actions extend. Yen is the weakest one as sentiments stabilized and turned mixed. Kiwi is the second weakest, followed by Loonie.

In Europe, CAC leads the way down by -0.71%, DAX is down -0.64% and FTSE is down -0.05%. Italian 10 year yield is dropping -0.0361 at 3.475. German 10 year bund yield is up 0.0049 at 0.556. German-Italian spread is no back below 300. Earlier in Asia, Nikkei rose 0.16%, Hong Kong HSI rose 0.08%, China Shanghai SSE rose 0.18%. But Singapore Strait Times dropped -1.11%. 10 year JGB yield dropped -0.0065 to 0.156, still way above BoJ’s allowed band of -0.1 to 0.1%.

Powell led a chorus of hawkish Fedspeaks

Fed Chair Jerome Powell repeated his upbeat comments today. He said the US is experiencing “a remarkably positive set of economic circumstances, and we’re working hard to try to sustain the expansion and keep unemployment low and keep inflation right on target”. And, “there’s really no reason to think that this cycle can’t continue for quite some time.” On interest rates, he said they are “still accommodative” and “we’re gradually moving to a place where they’ll be neutral.” He added that “we may go past neutral. But we’re a long way from neutral at this point, probably.”

Other comments from Fed officials were generally hawkish. Chicago Fed President Charles Evans said “getting policy up to a slightly restrictive setting — 3, 3.25 percent — would be consistent with the strong economy and good inflation that we are looking at.”

Philadelphia Fed President Patrick Harker said he preferred Fed’s rate hike schedule to avoid inverting the yield curve and “it’s just a question of timing”. He added there is no need to “rush the normalization process”. For now his forecasts are “”three this year, two next year, two year after.”

Cleveland Fed President Loretta Mester said she supported a gradual pace of hiking. But she also noted that “if we end up having inflation move high up” or if it goes too much above target, “then we need to move policy faster.”

Richmond Fed President Tom Barkin said “growth is solid, unemployment is low, and inflation is at target”. He didn’t touch directly on monetary policy but struck a tone of caution on flattening yield curve which “could suggest markets are losing confidence in the outlook.”