BoJ keeps monetary policy unchanged as widely expected, by unanimous vote. Under the yield curve control, short-term policy interest rate is held at -0.10%. 10-year JGB yield will be kept at around 0% with bond purchases without upper limit. 10-year JGB yield will continue to be allowed to fluctuate in range of around plus and minus 0.50% from 0% level.

The central bank maintained the pledge to continue with Quantitative and Qualitative Monetary Easing with Yield Curve Control for “as long as it is necessary” for meeting inflation target in a “stable manner”. It “will not hesitate to take additional easing measures if necessary”. BoJ will conduct a “broad-perspective review of monetary policy”, with a planned time frame of around 12 to 18 months.

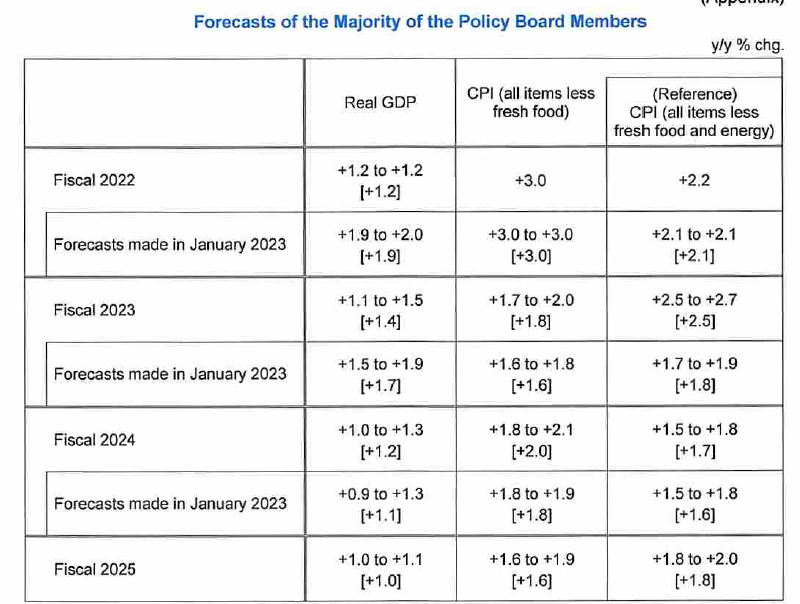

In the new economic projections, while core inflation forecasts were upgraded, it’s not expected to sustain at the 2% level throughout the horizon.

- Real GDP forecasts (versus January estimates):

- Fiscal 2023 at 1.4% (down from 1.7%).

- Fiscal 2024 at 1.2% (up from 1.1%).

- Fiscal 2025 at 1.0% (new)

- CPI Core forecasts (versus January estimates):

- Fiscal 2023 at 1.8% (up from 1.6%).

- Fiscal 2024 at 2.0% (up from 1.8%).

- Fiscal 2025 at 1.6% (new).

- CPI Core-Core forecasts (versus January estimates):

- Fiscal 2023 at 2.5% (up from 1.8%).

- Fiscal 2024 at 1.7% (up from 1.6%).

- Fiscal 2025 at 1.8% (new).

BoE to hold rates steady ahead of UK elections

BoE is widely expected to maintain interest rate at 5.25%, to avoid any perception of political interference ahead of the general election in the UK on July 4. Prime Minister Rishi Sunak’s unexpected call for an early election are seen by some as indirectly giving BoE additional time to monitor inflation trends and reassess the economic outlook. A more comprehensive decision is anticipated in August, when updated economic forecasts will be available.

Inflation data for May reinforces the case for a cautious, wait-and-see approach. Headline inflation has finally returned to BoE’s 2% target for the first time in almost three years, a positive development. However, services inflation remains stubbornly high at 5.7%, indicating underlying inflationary pressures that still need to be addressed.

Reflecting this development, money markets have adjusted their expectations, now pricing in only a 30% chance of a rate cut in August, down from 45% earlier in the week. There is still one quarter-point cut fully priced in for this year, likely by November, with a 60% chance of a second reduction, down from 80% earlier in the week.

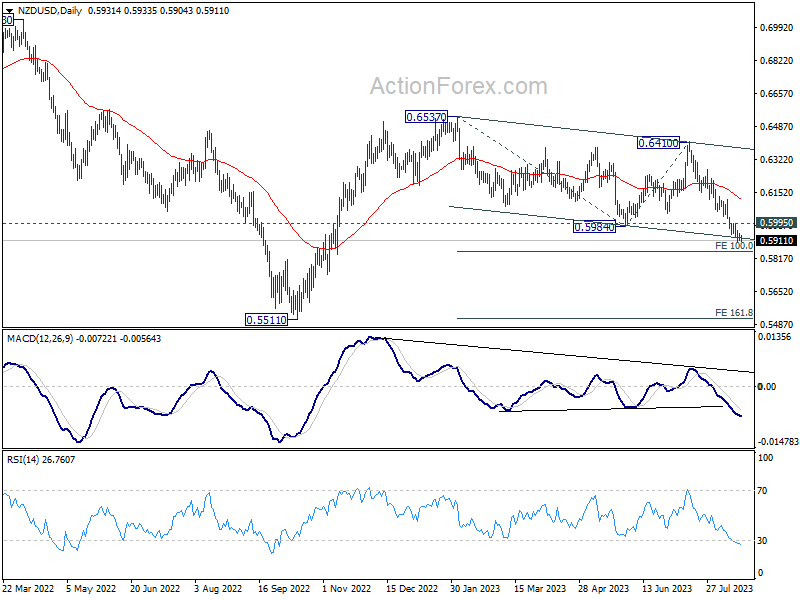

In the currency markets, EUR/GBP’s declined stalled after hitting 0.8396 last week. But near term outlook will stay bearish as long as 0.8482 support turned resistance holds. Any hawkish hints from BoE today could resume the down trend through 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.