BoE MPC member Catherine Mann, a known hawk, said in a speech that “we need to stay the course, and in my view the next step in Bank Rate is still more likely to be another hike than a cut or hold.”

She noted that “some (global) central bankers are seeing a turning point in data to which they are responding with an inflection in their respective policy paths”.

Also, “recent market chatter has focused on when central banks will stop hiking and if they will reverse, with fears torn between the risks of overtightening and stopping too soon.

But for assessment on the turning point, she is looking for “significant and sustained deceleration in higher frequency price increases and in the underlying inflation measures and expectations towards inflation rates that are consistent with achieving the 2% target”.

She emphasized, “uncertainty around turning points should not motivate a wait-and-see approach, as the consequences of under tightening far outweigh, in my opinion, the alternative.”

Full speech here.

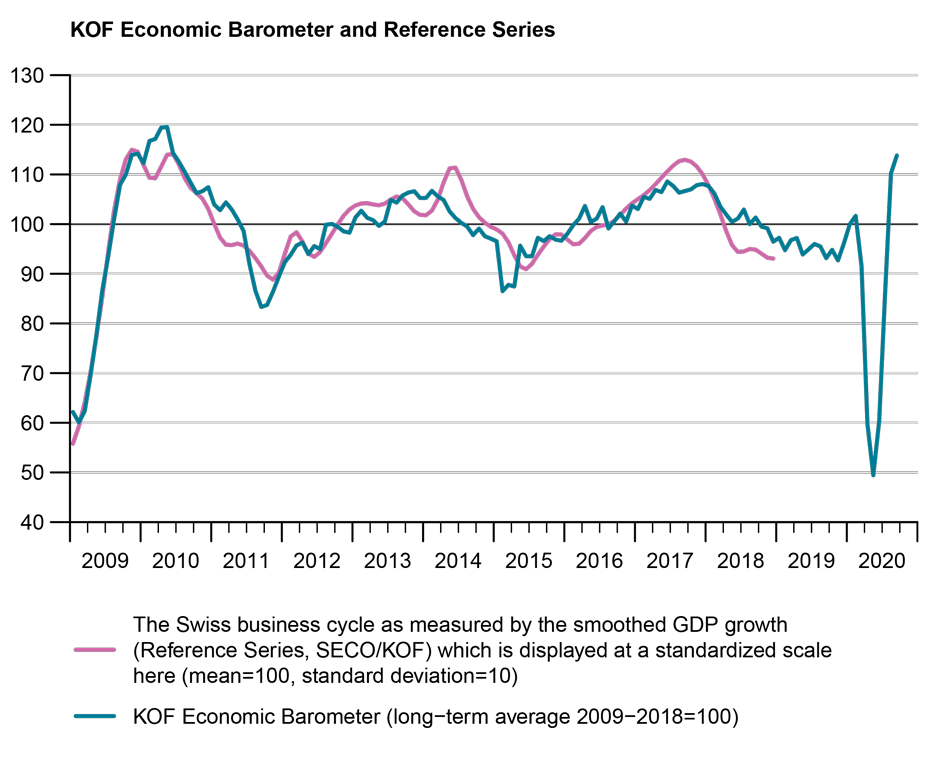

SNB Zurbruegg: Franc is still high, expansionary monetary policy remains appropriate

Swiss National Bank, Vice Chairman Fritz Zurbruegg, said in a Corriere del Ticino interview that, “we believe the franc is still high.” “If we look at inflation, it is still very low and GDP is not yet at the pre-crisis levels,” he said. “That is why we are convinced that our expansionary monetary policy remains appropriate.”

“We have to bear in mind that in a small and open country like ours, the exchange rate has a major impact on both inflation and economic growth,” he said. “For this reason, it is important to maintain the instrument of foreign exchange interventions alongside the classic interest rate instrument.”

“Without this expansionary policy, we would have a much stronger franc, lower growth and inflation and higher unemployment,” he said. “So the average Swiss citizen is better off thanks to our policy.”