Gold reached a new record high today, fueled by escalating geopolitical tensions in the Middle East and the prospect of easing policies from major central banks this year. Investors are flocking to the safe-haven asset following a series of unsettling events. On Sunday, a helicopter carrying Iranian President Ebrahim Raisi crashed in dense fog, heightening regional instability. Additionally, a China-bound oil tanker was hit by a Houthi missile in the Red Sea on Saturday, further exacerbating tensions. The anticipated shift towards more accommodative monetary policies by global central banks is also reducing the opportunity cost of holding Gold, providing further support for its rally.

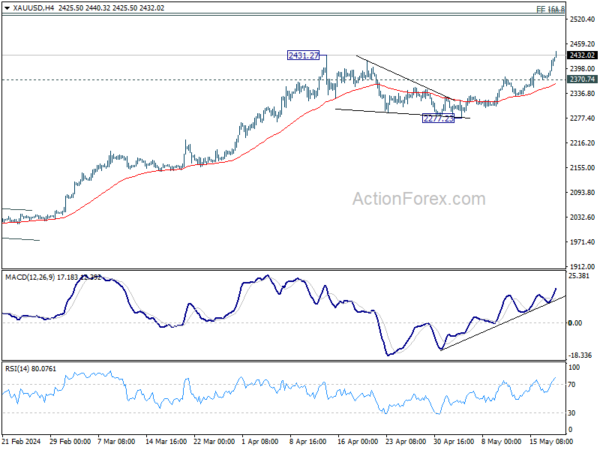

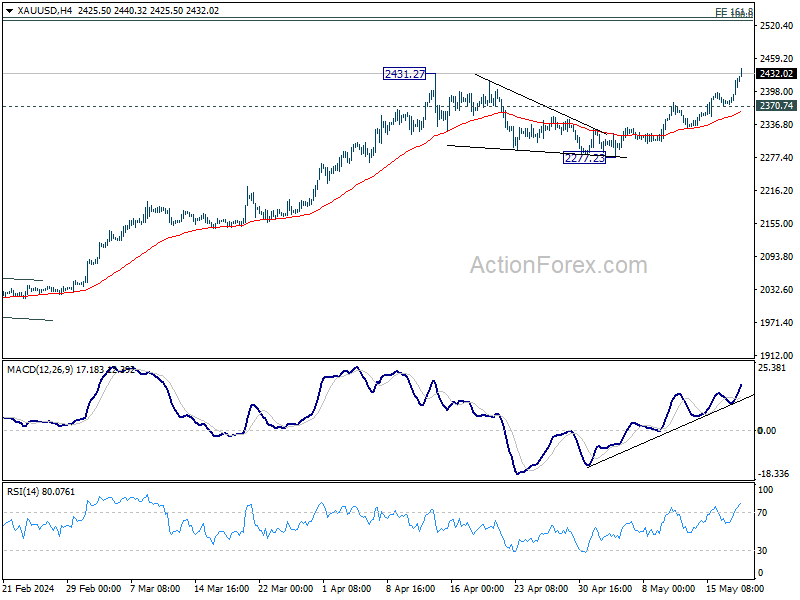

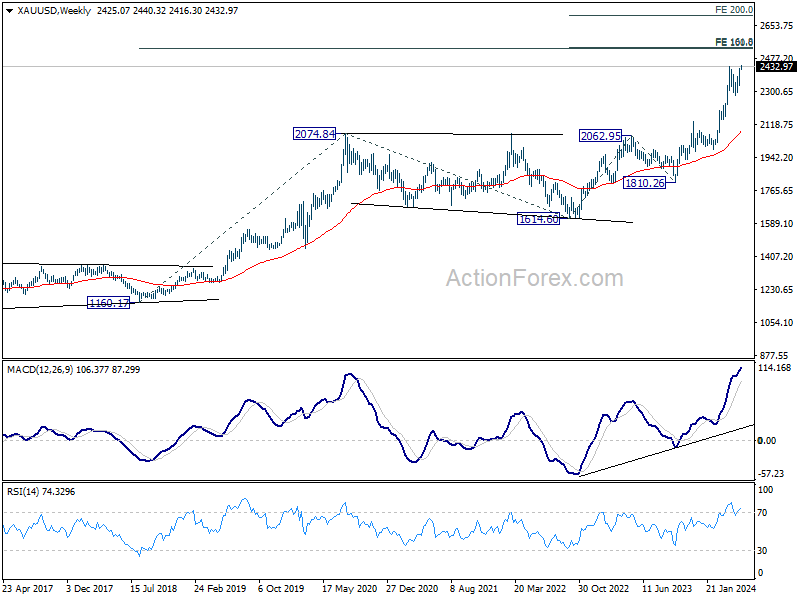

Technically, strong resistance could emerge at around 2500 to limit Gold’s up trend, at least on first attempt. There lies 161.8% projection of 1614.60 to 2062.95 from 1810.26 at 2535.69, and 100% projection of 1160.17 to 2074.84 at 1614.60 at 2529.27.

However, decisive break of 2500 would set the stage for 200% projection of 1614.60 to 2062.95 from 1810.26 at 2706.96 next. In any case, near term outlook will stay bullish as long as 2370.74 support holds.

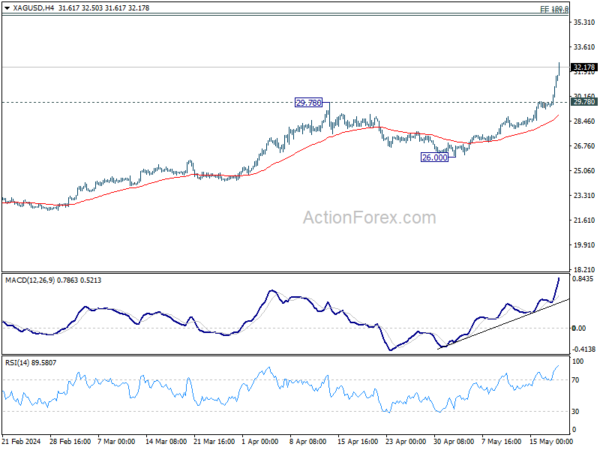

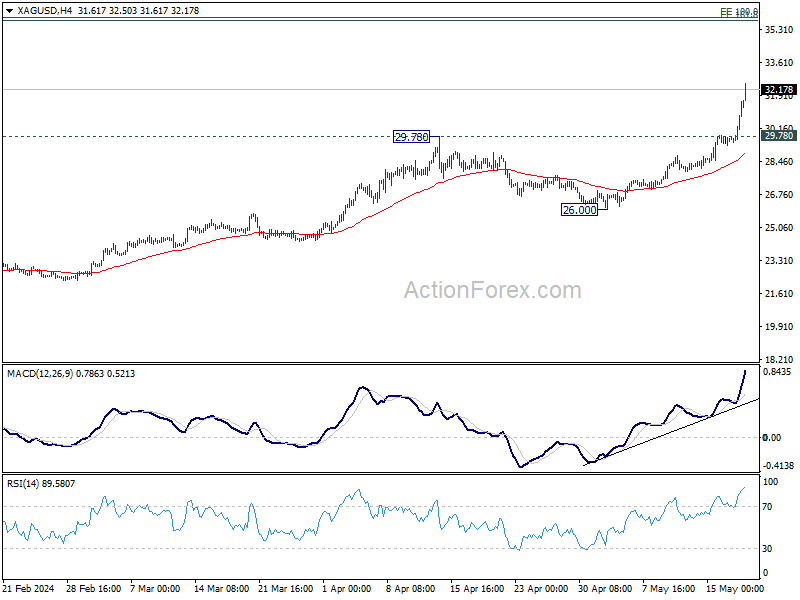

Silver is also in strong rally at this point. Near term outlook will stay bullish as long as 29.78 resistance turned support holds. Next target is cluster projection level at 35.80/94, 161.8% projection of 17.54 to 26.12 from 21.92 at 35.80 and 100% projection of 11.67 to 30.07 from 17.54 at 35.94.

Fed officials express caution on inflation, uncertainty over rate cuts

Fed Governor Philip Jefferson issued a cautious message in a speech last night, stating that while April’s inflation data was “encouraging,” it remains “too early to tell” if the recent slowdown in disinflation will be “long lasting.” He described current monetary policy as restrictive and declined to predict whether rate cuts will happen this year. He emphasized the importance of continuing to closely monitor incoming economic data, the outlook, and the balance of risks.

Separately, Cleveland Fed President Loretta Mester told Bloomberg Television that she is reconsidering her earlier forecast of three interest rate cuts this year. Although not her “base case,” Mester noted that if progress on reducing inflation stalls or reverses, Fed is “well positioned” to increase rates if necessary.

San Francisco Fed President Mary Daly also shared her views, expressing doubt about achieving the 2% inflation target in the near term. Daly highlighted that while there are expectations for improvement in shelter inflation, the progress is not expected to be rapid.