Investor attention is set to pivot towards Japan’s Q2 GDP data in the upcoming Asian session. Preliminary forecasts project a qoq growth of 0.8%, translating to an annualized expansion of 3.1%. In today’s trading, Nikkei took a significant hit, sliding by -1.27% or -413.7 points, largely influenced by bearish sentiments rooted in China’s property sector. Meanwhile, Yen showed signs of wavering post an initial surge, setting the stage for a keen watch on its reaction, as well as Nikkei’s, to the impending GDP figures.

After some initial volatility following BoJ’s adjustment on YCC on July 28, Nikkei has weakened notably. Technically, it’s now pressing 55 D MEA and looks vulnerable to deeper decline. Nevertheless, Overall price actions from 33772.89 are just viewed as a corrective move to the long term up trend only, as also supported by the structure. Hence, even in case of a deeper pull back, strong support should be seen from 38.2% retracement of 25661.89 to 33772.89 to contain downside. Meanwhile, strong rebound from current level, would bring retest of 33772.89 high.

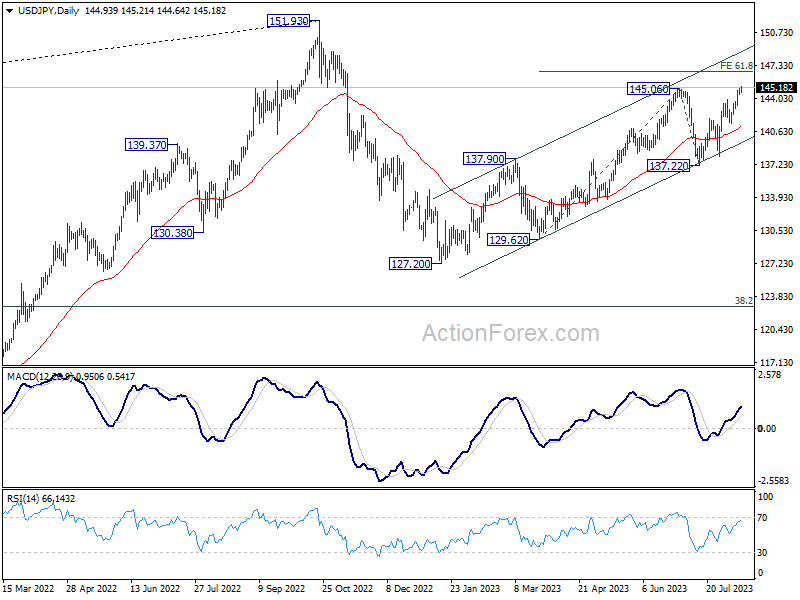

Meanwhile, Yen continued to weaken after brief post-BoJ spike, with USD/JPY breaking through 145 handle today. Market chatter suggests a potential pushback by Ministry of Finance in the 145-148 range, though tangible signs of intervention remain absent. Yet it’s a wait-and-watch game to discern if Japan would act beyond the 145 mark. Nevertheless, technically, 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 doe present a resistance to overcome.

EU downgrades 2022 Eurozone GDP forecasts, upgrades inflation

In the Winter 2022 interim forecasts, EU downgrades 2022 Eurozone GDP growth forecasts from 4.3% to 4.0%. Nevertheless, 2023 GDP growth forecast was upgraded from 2.4% to 2.7%. Eurozone 2022 HICP inflation forecast was raised from 2.2% to 3.5%. 2023 HICP inflation forecast was also upgraded from 1.4% to 1.7%.

Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People said: “The EU economy has now regained all the ground it lost during the height of the crisis, thanks to successful vaccination campaigns and coordinated economic policy support. Unemployment has reached a record low. These are major achievements. As the pandemic is still ongoing, our immediate challenge is to keep the recovery well on track. The significant rise in inflation and energy prices, along with supply chain and labour market bottlenecks, are holding back growth. Looking ahead, however, we expect to switch back into high gear later this year as some of these bottlenecks ease. The EU’s fundamentals remain strong and will be boosted further as countries start to put their Recovery and Resilience Plans into full effect.”

Paolo Gentiloni, Commissioner for Economy said: “Multiple headwinds have chilled Europe’s economy this winter: the swift spread of Omicron, a further rise in inflation driven by soaring energy prices and persistent supply-chain disruptions. With these headwinds expected to fade progressively, we project growth to pick up speed again already this spring. Price pressures are likely to remain strong until the summer, after which inflation is projected to decline as growth in energy prices moderates and supply bottlenecks ease. However, uncertainty and risks remain high.”

Full release here.