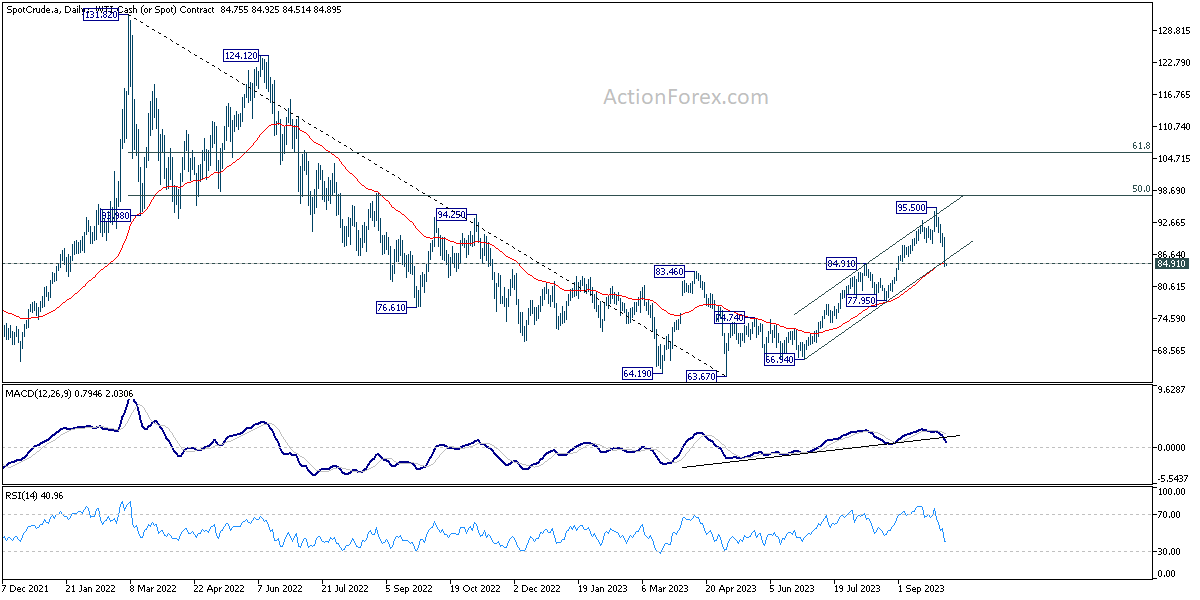

Oil prices took a significant dip overnight, with WTI now trading USD 10 beneath last week’s peak of 95.50. This decline is notably perplexing given the absence of a clear triggering event. OPEC+’s resolution to uphold output cuts is conventionally a precursor for a bullish response in the market. However, the rapid and profound dip has spurred conversations around the onset of demand destruction, provoked by the Q3 oil price spike.

In this week’s meeting, the OPEC+ ministerial panel opted for status quo, maintaining its existing oil output policy. Saudi Arabia pledged to persist with its voluntary cut of 1 million barrels per day through the end of 2023, while Russia committed to retaining its voluntary export reduction of 300k bpd until December’s end.

A note from JPMorgan’s commodity analysts titled “Demand destruction has begun (again)” highlighted that the repercussions of surging oil prices are re-emerging in the form of demand restraints in regions including US, Europe, and certain Emerging Markets.

The crux of global oil demand growth, anchored by China and India, is also showing signs of waning. China’s decision to utilize domestic crude inventories following the surge in oil prices is indicative of this trend.

In the US, gasoline consumption has plummeted to a 22-year low. The considerable 30% hike in fuel prices in Q3 has reportedly dampened demand, leading to an atypical decline of 223k barrels per day.

From a technical standpoint, WTI crude oil finds itself at a pivotal support juncture, which comprises the 84.91 resistance-turned-support and the 55 D EMA, currently pegged at 84.90. While a solid rebound from this position remains plausible, it’s expected to be restrained well below 95.50 high.

On the other hand, sustained break of 84.91 would confirm rejection by 50% retracement of 131.82 to 63.67 at 97.74. WTI could then be reversing whole rally from May’s low at 63.67, and risk falling further to 77.95 support.

EU Moscovici: Brexit has to be dealt with in London first

European Commissioner for Economic and Financial Affairs Pierre Moscovici reiterated the EU’s stance that regarding Brexit, the ball is in UK’s court now. He said “Certainly the EU is there, the EU is waiting, the EU is ready but first we need to know clearly what are the British intentions and we need some clarifications from London”.

He added that “Of course the door is always open for discussion but it’s not up to us to tell now the British side where it wants to go. The ball clearly is in the British side again. It’s not a problem that can be solved by Brussels, maybe in Brussels later, but it has to be first dealt with in London.”

Also on the possibility of hard Brexit, Moscovici said “Nobody wants a no-deal (Brexit), that is clear. The British parliament doesn’t want a no-deal, the British government doesn’t want a no-deal, and the EU is not willing a no-deal, so we need to explore all options which are not a no-deal.”