US non-farm payroll employment grew 216k in December, above expectation of 168k. Unemployment rate was unchanged at 3.7%, below expectation of a rise to 3.8%. Participation rate fell from 62.8% to 62.5%. Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings increased 4.1% yoy.

Market watchers were in a frenzy after Japanese Yen surged from 150 to the 147 zone against Dollar overnight , fuelling speculation that Japan’s government may have stealthily intervened to push up the struggling currency. While evidence of a Yen-buying, Dollar-selling maneuver abounds, top officials in Japan remained tight-lipped today.

Finance Minister Shunichi Suzuki, when confronted by reporters, chose the path of silence over confirmation. He held back from validating the swirl of speculations about intervention. Suzuki reiterated a standard narrative, emphasizing the desirability of market-driven, stable currency movements that mirror economic fundamentals.

“Currency rates ought to move stably driven by markets, reflecting fundamentals. Sharp moves are undesirable,” Suzuki noted. “The government is monitoring market developments very carefully with a sense of urgency. We will take appropriate steps against excessive volatility without excluding any options.”

Masato Kanda, the top currency diplomat, provided insights into the government’s assessment mechanism for currency movements. “If currencies move too much on a single day or, say, a week, that’s judged as excess volatility,” Kanda explained.

The implied volatility stands as a critical metric, among others, shaping the official perspective on whether Yen’s moves are reaching alarming amplitudes.

Kanda further outlined that even in the absence of abrupt shifts, a gradual yet one-sided build-up of significant currency movements over time is also classified as excessive volatility. However, he too refrained from offering a direct commentary on the overnight upswing of Yen.

European Commission President Jean-Claude Juncker and UK Prime Minister Theresa May held “constructive” talks in Brussels yesterday. According to a joint statement, they discussed the guarantees that could be give to underline once again that the Irish backstop’s “temporary nature”. And the “role alternative arrangement” could play in “replacing the backstop” in future. Also, additions or changes to the Political Declaration could be made to “increase confidence in the focus and ambition of both sides in delivering the future partnership envisaged as soon as possible.” EU Chief Negotiator Michel Barnier and UK Secretary of State Stephen Barclay will follow up and progress will be reviewed in the coming days.

May said after meeting with Juncker that “I have underlined the need for us to see legally binding changes to the backstop that ensure that it cannot be indefinite. That’s what is required if a deal is to pass the House of Commons. We have agreed that work to find a solution will continue at pace. Time is of the essence and it is in both our interests that when the UK leaves the EU it does so in an orderly way. So, we have made progress.”

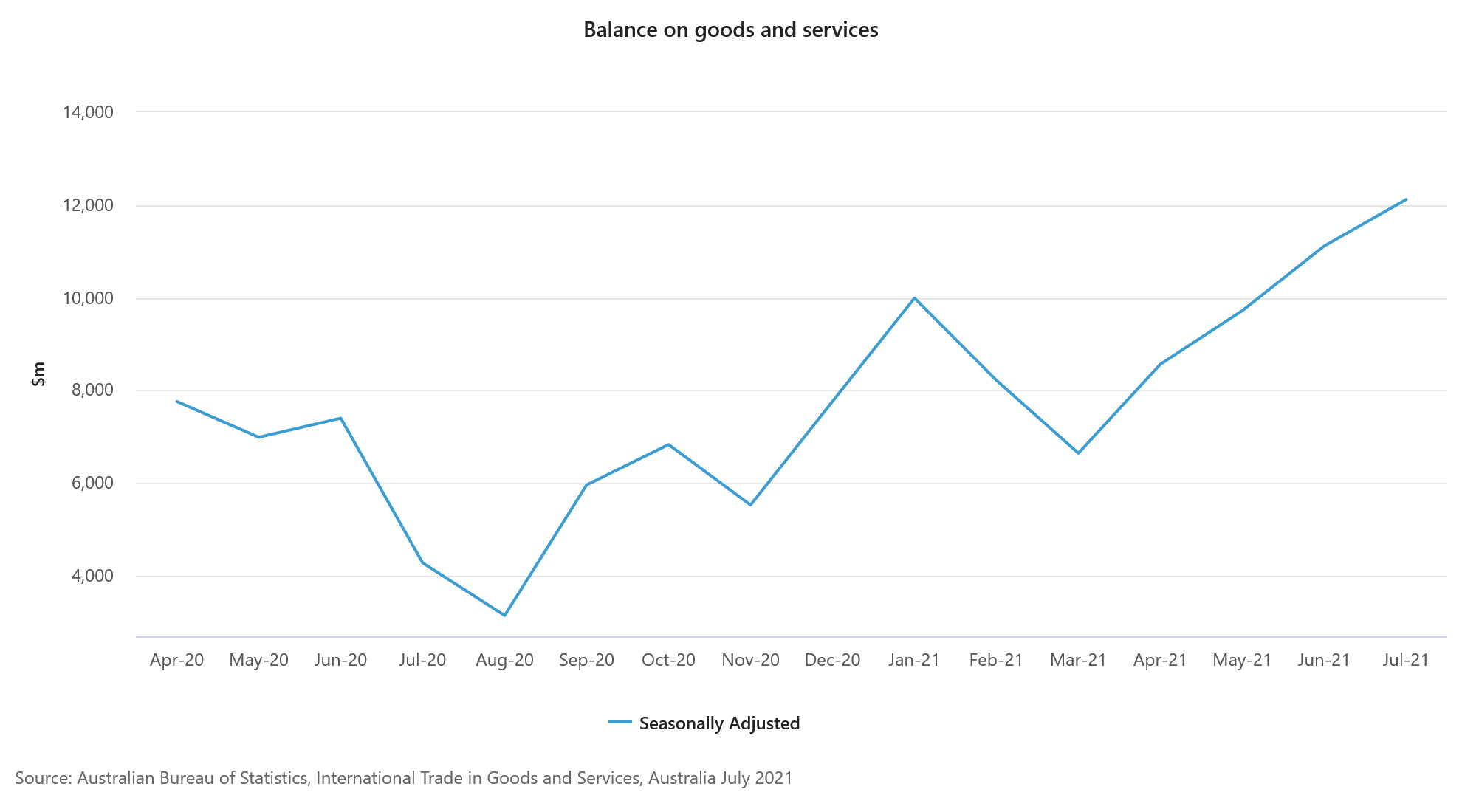

Australia current account surplus widened notably to AUD 8.4B in Q1, up from AUD 1.7B and beat expectation of AUD 6.3B. The current account surplus was driven by a trade surplus of AUD 19.2B and a narrowing of net income deficit to AUD 10.6B. In seasonally adjusted chain volume terms, the balance on goods and services surplus should contribute 0.5% to Q1 GDP growth.

ABS Chief Economist Bruce Hockman said: “The impact of COVID-19 was evident across the Balance of Payments this quarter, with falls for imports and exports of both goods and services in volume terms”.

Also released, sales of manufacturing goods and services rose 2.2% qoq in Q1. Whole sale trade rose 1.6% qoq. Inventories dropped -1.2% qoq. Company gross operating profits rose 1.1% qoq. wages and salaries were flat.

ECB meeting will be a focus today and attention will mainly be on the PEPP purchase plan in Q4. The pace of purchases was significantly higher in Q2 and Q3. But with improvement in economic activities, as well as financing conditions, it’s time for the central bank to re-calibrate the program. Chief Economist Philip Lane sounded cautious as he indicated there could be a “local adjustment” of the program but not a “pure taper situation”. The plan for the emergency purchase program beyond the end date of March 2022 is probably still a bit “far away” for the council members.

New economic projections will be published and there were already some indications on upgrade in growth forecasts for this year. But that could also be offset by a slight downgrade for next year. So the overall impact could be muted. The key is indeed on how ECB views the inflation path. CPI was at a 10-year high of % in August and the projections would show how it will peak and then slow, to reflect how transitory inflation would be.

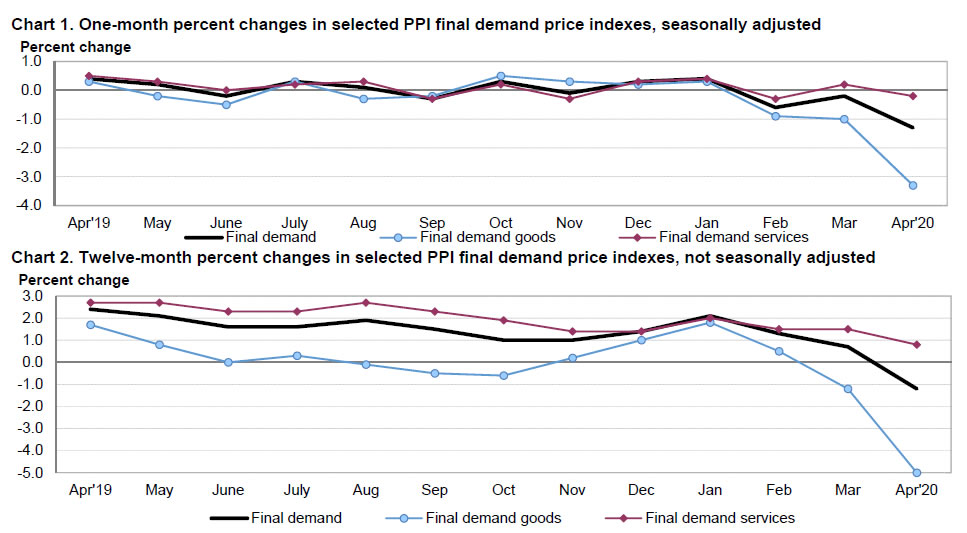

US PPI final demand dropped -1.3% mom in April, below expectation of -0.5% mom. That’s the largest monthly decrease since December 2009. Core PPI dropped -0.3% mom, below expectation of 0.0% mom.

Annually, PPI dropped -1.2% yoy, dropped from 0.7% yoy, versus expectation of -0.4% yoy. That’s also the largest decline since November 2015. PPI core rose 0.6% yoy, slowed from 1.4% yoy, below expectation of 0.9% yoy.

BoJ has reaffirmed its commitment to continuing with its current monetary easing policy, including yield curve control, to achieve the price stability target, according to the minutes of its meeting in January 17-18.

One member noted that there is “still a long way to go to achieve the price stability target”, and thus the Bank should continue with the current monetary easing to firmly support the economy.

To encourage firms’ efforts with regard to business transformation until sustained wage increases can be expected, the Bank needs to “curb interest rate rises across the entire yield curve” while paying attention to the functioning of bond markets, according to another member.

Another member added that it was “inappropriate to rush to an exit” from the current monetary policy, as overseas economies were currently heading toward slowdowns.

However, one member recognized that “at some point in the future”, it will be necessary to examine and assess the balance between the positive effects and side effects of the current monetary easing policy.

The Bank’s “basic stance on its future conduct of monetary policy” is to “continue with the current monetary easing — including the conduct of yield curve control — and thereby achieve the price stability target in a sustainable and stable manner accompanied by wage increases,” the minutes read.

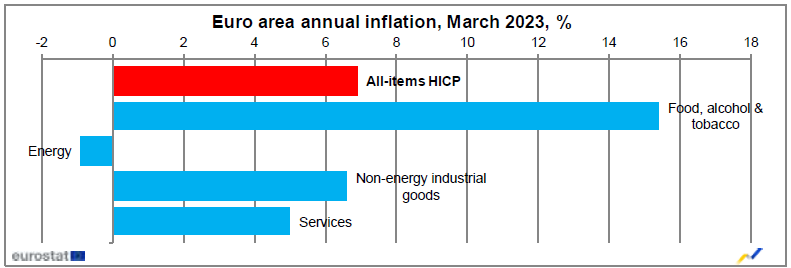

Eurozone CPI slowed from 8.5% yoy to 6.9% yoy in March, below expectation of 7.2% yoy. CPI core (all item ex energy, food, alcohol & tobacco) roes from 5.6% yoy to 5.7% yoy, matched expectations.

Looking at the main components , food, alcohol & tobacco is expected to have the highest annual rate in March (15.4%, compared with 15.0% in February), followed by non-energy industrial goods (6.6%, compared with 6.8% in February), services (5.0%, compared with 4.8% in February) and energy (-0.9%, compared with 13.7% in February).

Mario Draghi, President of the ECB,

Luis de Guindos, Vice-President of the ECB,

Frankfurt am Main, 13 September 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the Commission Vice-President, Mr Dombrovskis.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, we will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of this month. After September 2018, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and we anticipate that, subject to incoming data confirming our medium-term inflation outlook, we will then end net purchases. We intend to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The incoming information, including our new September 2018 staff projections, broadly confirms our previous assessment of an ongoing broad-based expansion of the euro area economy and gradually rising inflation. The underlying strength of the economy continues to support our confidence that the sustained convergence of inflation to our aim will proceed and will be maintained even after a gradual winding-down of our net asset purchases. At the same time, uncertainties relating to rising protectionism, vulnerabilities in emerging markets and financial market volatility have gained more prominence recently. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council’s inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.4%, quarter on quarter, in the second quarter of 2018, following growth at the same rate in the previous quarter. Despite some moderation following the strong growth performance in 2017, the latest economic indicators and survey results overall confirm ongoing broad-based growth of the euro area economy. Our monetary policy measures continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by rising wages. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the expansion in global activity is expected to continue, supporting euro area exports.

This assessment is broadly reflected in the September 2018 ECB staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.0% in 2018, 1.8% in 2019 and 1.7% in 2020. Compared with the June 2018 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised down slightly for 2018 and 2019, mainly due to a somewhat weaker contribution from foreign demand.

The risks surrounding the euro area growth outlook can still be assessed as broadly balanced. At the same time, risks relating to rising protectionism, vulnerabilities in emerging markets and financial market volatility have gained more prominence recently.

According to Eurostat’s flash estimate, euro area annual HICP inflation was 2.0% in August 2018, down from 2.1% in July. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening and broadening amid high levels of capacity utilisation and tightening labour markets, which is pushing up wage growth. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion and rising wage growth.

This assessment is also broadly reflected in the September 2018 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2018, 2019 and 2020, which is unchanged from the June 2018 Eurosystem staff macroeconomic projections.

Turning to the monetary analysis, broad money (M3) growth declined to 4.0% in July 2018, from 4.5% in June. Apart from some volatility in monthly flows, M3 growth is increasingly supported by bank credit creation. The narrow monetary aggregate M1 remained the main contributor to broad money growth.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 4.1% in July 2018, while the annual growth rate of loans to households stood at 3.0%, both unchanged from June.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing – in particular for small and medium-sized enterprises – and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that an ample degree of monetary accommodation is still necessary for the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt is high and for which full adherence to the Stability and Growth Pact is critical for safeguarding sound fiscal positions. Likewise, the transparent and consistent implementation of the EU’s fiscal and economic governance framework over time and across countries remains essential to bolster the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

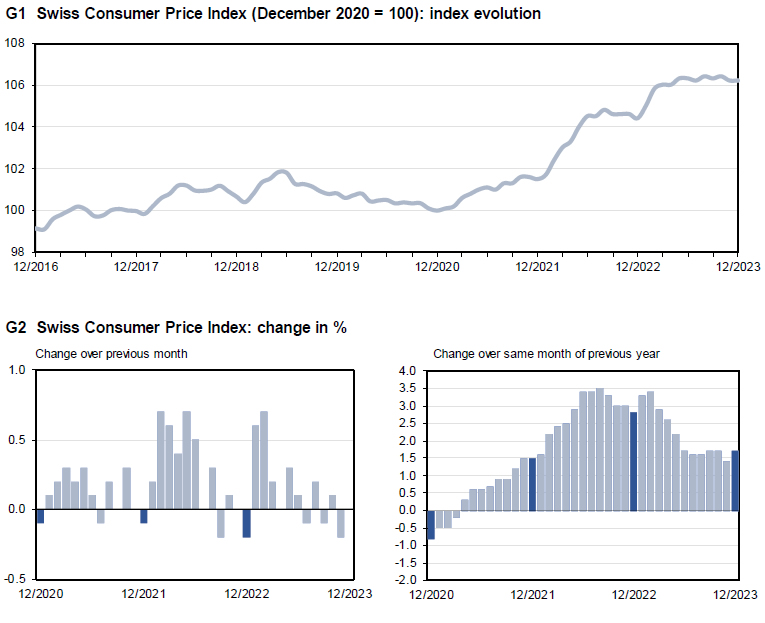

Swiss CPI was flat at 0.0% mom in December, above expectation of -0.1% mom. Core CPI (fresh and seasonal products, energy and fuel) rose 0.2% mom. Domestic products prices rose 0.3% mom. Import products price fell -0.7% mom.

For the 12-month period, CPI rose from 1.4% yoy to 1.7% yoy, matched expectations. Core CPI rose from 1.4% yoy to 1.5% yoy. Domestic products prices rose from 2.1% yoy to 2.3% yoy. Imported products prices from also rose from -0.6% yoy to -0.2% yoy.

Germany CPI dropped -0.2% mom in August, worse than expectation of -0.1% mom. Annually, CPI slowed to 1.4% yoy, down from 1.7% yoy, missed expectation of 1.5% yoy.

Released earlier today, German unemployment rose 4k in August, matched expectations. Unemployment rate was unchanged at 5.0%, also matched expectations.

In an editorial in the official China Xinhua, it’s set that China and the US “reached agreements” on some issues in the trade talks. And both sides agreed to set up a “work mechanism” to keep close communications.

But there are “considerable differences” that still exist on some issues and “continued hard work is required for more progress”.

Responses from EU regarding UK’s request for Article 50 extensions are generally hardline. European Council President Donald Tusk said EU will only approval short Article 50 extension if UK Parliament passes the Brexit deal. And, if the vote is passed in the Commons next week, the extension can then be finalized using a written procedure. Tusk is also ready to call a summit next week if needed.

Full statement of Tusk.

“In the light of the consultations that I have conducted over the past days, I believe that a short extension would be possible.

But it would be conditional on a positive vote on the withdrawal agreement in the House of Commons.

The question remains open as to the duration of such an extension.

At this time, I do not foresee an extraordinary European council.

If the leaders approve my recommendations and there is a positive vote in the House of Commons next week, we can finalise and formalise the decision on extension in the written procedure.

However, if there is such a need, I will not hesitate to invite the members of the European council for a meeting to Brussels next week.

Although Brexit fatigue is increasingly visible and justified, we cannot give up seeking until the very last moment a positive solution – of course, without opening up the withdrawal agreement.

We have reacted with patience and goodwill to numerous turns of events and I am confident that also now we will not lack the same patience and goodwill at this most critical point in this process.”

Earlier French Foreign Minister Jean-Yves Le Drian said also said the extension will only be granted if May could provide guarantee for passing the deal. He said: “A situation in which Mrs May was not able to present to the European Council sufficient guarantees of the credibility of her strategy would lead to the extension request being dismissed and opting for a no-deal exit.”

German Foreign Minister Heiko Maas said “We’ve always said that if the Council has to decide on a deadline extension for Britain, then we’d like to know why and what for.”

ECB left interest rates unchanged as wildly expected. Interest rates on the marginal lending facility and the deposit facility are held at 4.25%, 4.50% and 3.75% respectively.

In the accompanying statement, ECB noted that incoming information broadly support the Governing Council’s medium-term inflation outlook. Most measures of underlying inflation were “either stable or edged down” in June. Impact of high wage growth has been “buffered by profits”.

Nevertheless, domestic price pressures are “still high” while services inflation is “elevated”. Headline inflation is “likely to remain above the target well into next year”.

ECB also pledge to keep policy rates “sufficiently restrictive for as long as necessary”, and will continue to follow a “date-dependent and meeting-by-meeting” approach, while “not pre-committing” to a particular rate path.

Ethereum staged an upside breakout over the weekend, and edged above 3100 mark. For the moment, it’s outperforming Bitcoin is stuck in range after breaching 53000 briefly earlier in the month. There is prospect for Ethereum to continue to outshine Bitcoin in the near term, in anticipation of a new wave of spot crypto ETF on the world’s second-largest digital asset.

The approval of the first spot Bitcoin ETFs by US regulators in January has already marked a significant milestone. These ETFs have attracted over USD 5B in net inflows since their inception on January 11. There is growing speculation that Ether ETFs could receive regulatory approval as soon as the second quarter, possibly in May.

Technically, Ethereum is in upside acceleration mode as seen in D MACD, and the break of channel resistance. Next target is 100% projection of 1519 to 2715 from 2164 at 3360. Considering overbought condition as seen in D RSI, upside might be limited there on first attempt and bring consolidations first. But in any case, outlook will stay bullish as long as 2715 resistance turned support holds. Meanwhile, decisive break of 3360 will pave the way to 161.8% projection at 4099 next, which is above 4k psychological level.

As for Bitcoin, outlook will stay bullish as long as 55 D EMA (now at 46376 holds). Decisive break of 61.8% projection of 24896 to 49020 from 38496 at 53404 will pave the way to 100% projection at 62620.

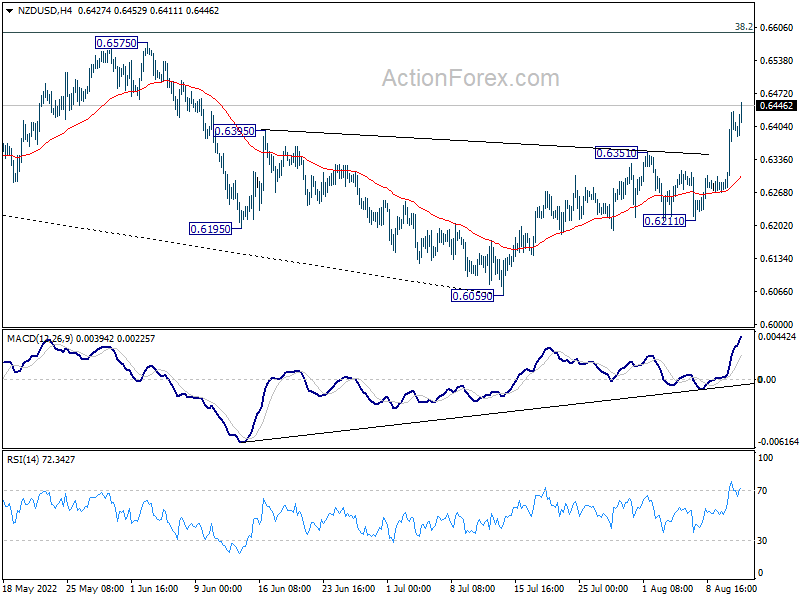

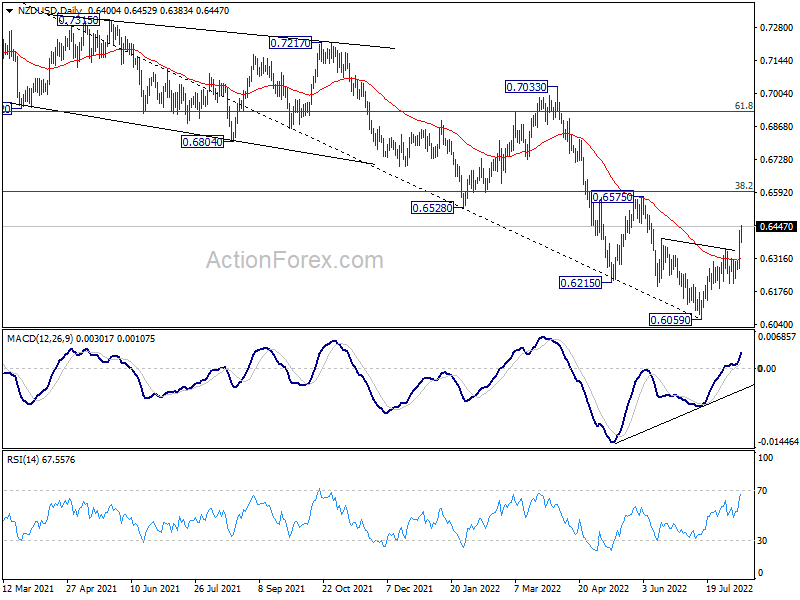

NZD/USD surges to as high as 0.6452 so far today and it’s still in upside acceleration mode. This week’s break of 0.6351 resistance completes a head and shoulder bottom pattern (ls: 0.6195, h: 0.6059, rs: 0.6211). The strong break of 55 day EMA, and bullish convergence condition in daily MACD are both bullish signs too.

Further rise is now expected as long as 0.6351 resistance turned support holds. Next target is 0.6575 cluster resistance zone (38.2% retracement of 0.7463 to 0.6059 at 0.6595). This is the major resistance zone for NZD/USD to overcome. Decisive break there will raise the chance of medium term bullish reversal. Meanwhile, rejection by 0.6575/95 will maintain medium term bearishness.

Australia goods and services exports rose 5% mom in July to AUD 45.94B. The strong rise is exports was based on strong Asian demand for LNG and thermal coal, combined with sharply higher prices for iron ore. Exports to China also rose to record AUD 19.4B. Goods and services imports rose 3% mom to AUD 33.83B, due to sharp increase in parts and accessories for telecommunications equipment.

Trade surplus widened to AUD 12.12B, above expectation of AUD 10.1B., hitting a new record.

Japan’s Ministry of Economy, Trade and Industry reported 2.0% mom increase in industrial production in June, below expected 2.4%. This places the seasonally adjusted index of production at factories and mines at 105.3, with 2020 as the base of 100.

Motor vehicles led industrial production growth, surging 6.1% thanks to robust demand in both domestic and overseas markets. Out of 15 industrial sectors covered , 10 sectors saw increased output, while production in five dropped.

Despite the production growth coming in lower than expected, the Ministry maintained its basic assessment, noting that industrial production was “showing signs of moderately picking up.”

Looking ahead, the Ministry’s forecast based on a poll of manufacturers anticipates slight output decline of -0.2% in July, followed by climb of 1.1% in August.

Also released, retail sales rose 5.9% yoy in June, above expectation of 5.4% yoy, picked up from prior month’s 5.7% yoy.

Japan PMI manufacturing was finalized at 50.3 in January, revised up from 50.0. But that’s still the lowest level in 29 months. And, new export orders decline at sharpest pace since July 2016. Also, business confidence falls for the eighth month running.

Commenting on the Japanese Manufacturing PMI survey data, Joe Hayes, Economist at IHS Markit, which compiles the survey, said:

“Japan Manufacturing PMI data brought bad news for the global trade cycle at the start of 2019, with new export orders falling at the sharpest rate in two-and-a-half years. Anecdotal evidence suggested that sales of goods relating to semi-conductors had particularly suffered, which bodes ill for other Asian exporters. Meanwhile, domestic markets also showed signs of frailty as total demand declined for the first time since September 2016.

“With Abe set to levy the consumption tax this year, and Sino-US trade tensions still lurking, domestic weakness in Japan further adds to already existing challenges. Business sentiment continued to drop, with survey data registering an eighth straight month where confidence has slipped. Falling inventories and cut backs to production suggest that manufacturers are bracing for further economic difficulty.”

In response to Trump’s probe on auto tariffs, Japanese Chief Cabinet Secretary Suga noted that Japan is closely monitoring the situation and emphasized that any trade steps should be in accordance with WTO rules. Trade Minister Seko said the potential auto tariffs are regrettable and warned that the would cause confusion in the global economy.

As a recap on recent Japanese trade statistics, the Finance Ministry reported JPY 626B surplus in April, up 30.9% from a year ago. Exports jumped 7.8% to JPY 6.8T, up fro the 17th straight months. Import rose 5.9% JPY 6.2T.

Japan’s trade surplus with the US rose 4.7% to JPY 616B as export rose 4.3% and import rose 3.9%.

Transport equipment is a major contributor to the export to US, and overall export growth in April. Total transport equipment contributed to 39.4% of exports to the US and grew 5.3% to JPY 507B. Motor vehicles was a large part, at 30.2% of total exports to the US, grew 10.0% to JPY 389B.

Japan is one of the few top 10 steel importers to the US who’s not even granted a temporary exemption on steel tariffs. Though, iron and steel products exports to the US rose 13.7% in April to JPY 18.2B.

US NFP rises 216k, unemployment rate unchanged at 3.7%

US non-farm payroll employment grew 216k in December, above expectation of 168k. Unemployment rate was unchanged at 3.7%, below expectation of a rise to 3.8%. Participation rate fell from 62.8% to 62.5%. Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings increased 4.1% yoy.

Full US non-farm payrolls release here.