In the minutes of October 2 meeting, RBA noted that global economic conditions had continued to be positive for Australia, despite risks including trade policies. Also, elevated energy and bulk commodity prices supported its terms of trade. Broad based appreciation of the US dollar “had raised risks for some economies, particularly the more fragile emerging market economies”. But the “resultant modest depreciation of the Australian dollar was likely to have been helpful for domestic economic growth.

Domestically, RBA maintained that GDP growth would be “above potential over the following two years”. Forward-looking indicators of labour demand continued to point to above-average growth”. And wage growth is expected increase “gradually”. However, subdued household income growth remained an “important source of uncertainty for the outlook for consumption and inflation.”

Overall, RBA also maintained that ” the next move in the cash rate was more likely to be an increase than a decrease.” However, “since progress on unemployment and inflation was likely to be gradual, they also agreed there was no strong case for a near-term adjustment in monetary policy.”

Chinese President Xi Jinping met US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin at the Great Hall of the People in Beijing today, as the week-long trade negotiations conclude.

According to a report by the official Xinhua, Xi said that the talks will continue in Washington next week. And he hoped that both sides would reach a mutually beneficial deal.

Xinhua also reported that Lighthizer and Mnuchin said in-depth discussions were held in the past two days. New progress has been made on difficult issues. But there is still a lot of work to be done.

San Francisco Fed President Mary Daly told CNBC that “consumers are preparing for slower economy, that’s a good start.” She added that Fed wants to see “economy slow” to “get inflation down”, and “slower inflation, labor market are encouraging “.

She also said “pausing” the tightening cycle is “not part of the discussion” right now. The focus is on “level of rates”. She added, “I still think 5% is reasonable” as an “ending place for rates”. Also, “a range of 4.75% – 5.25% is reasonable for policy rate end-point.”

ECB Governing Council member Martins Kazaks, in an interview overnight, indicated that the most likely period for rate reductions could be around the “middle of next year”, specifically pointing to June or July as probable months.

However, Kazaks expressed caution about reducing rates too soon, stating, “But in the spring at the current moment that’s too early.” He also noted a disparity between his outlook and market expectations, particularly concerning the possibility of an initial rate cut in March, which he views as overly “optimistic”.

Kazaks also noted that interest rates are likely to remain at 4% for a while before any reduction is considered.

US commercial crude oil inventories dropped -8m barrels in the week ending October 30, versus expectation of 0.3m barrels rise. At 484.4m barrels, oil inventories are about 7% above the five year average of this time of year. Gasoline inventories rose 1.5m barrels. Distillate dropped -1.6m barrels. Propane/propylene dropped -2.6m barrels. Commercial petroleum inventories dropped -14.7m barrels.

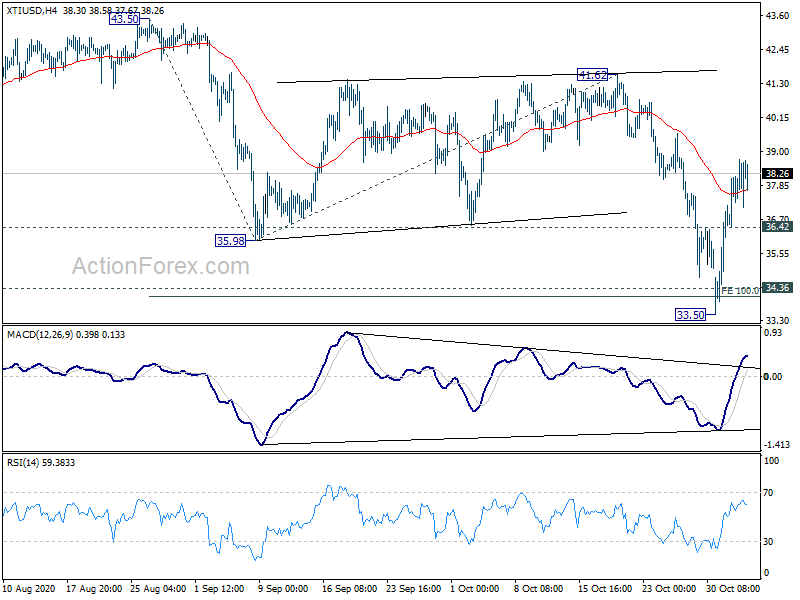

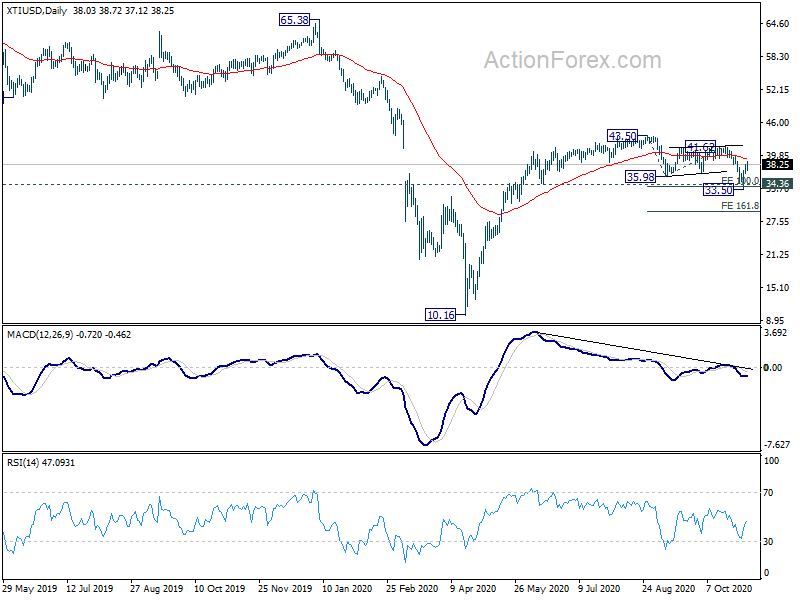

WTI rebounded strongly after drawing support from 34.10/36 support zone, despite breaching to 33.50. For now near term outlook will stay neutral first. WTI needs to sustain above 55 day EMA (now at 39.28) to provide the first sign of uptrend resumption. Nevertheless, even in case of another fall, we’d continue to expect strong support from 33.50 to contain downside.

China’s ambassador to WTO, Zhang Xiangchen said that “the US is blocking selection of new Appellate Body members, taking restrictive trade measures under Section 232 and threatening to impose tariff measures of US$50 billion of goods imports from China under Section 301 of US domestic law.” And, he warned “any one of these, if left untreated, will fatally undermine the functioning of the WTO.”

The US was reported to have requested China to cut its trade surplus with it by USD 200b by 2020. Zhang criticized that “such practices clearly violate the non-discrimination principle of the GATT, therefore have long been abandoned” by the WTO.

And he pointed out the contradiction in what the US is trying to do. He said “the US is blaming the Chinese Government for state intervention on the one hand, while pressing China, by way of issuing government orders, to increase imports, restrict exports, and reduce excess capacity on the other hand.” Also, “governments can make efforts to promote trade, but cannot force companies to do business by pointing gun at their heads.”

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the President of the Eurogroup, Mr Centeno.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, our net purchases under the asset purchase programme (APP) will end in December 2018. At the same time, we are enhancing our forward guidance on reinvestment. Accordingly, we intend to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

While incoming information has been weaker than expected, reflecting softer external demand but also some country and sector-specific factors, the underlying strength of domestic demand continues to underpin the euro area expansion and gradually rising inflation pressures. This supports our confidence that the sustained convergence of inflation to our aim will proceed and will be maintained even after the end of our net asset purchases. At the same time, uncertainties related to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility remain prominent. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. Our forward guidance on the key ECB interest rates, reinforced by the reinvestments of the sizeable stock of acquired assets, continues to provide the necessary degree of monetary accommodation for the sustained convergence of inflation to our aim. In any event, the Governing Council stands ready to adjust all of its instruments, as appropriate, to ensure that inflation continues to move towards the Governing Council’s inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.2%, quarter on quarter, in the third quarter of 2018, following growth of 0.4% in the previous two quarters. The latest data and survey results have been weaker than expected, reflecting a diminishing contribution from external demand and some country and sector-specific factors. While some of these factors are likely to unwind, this may suggest some slower growth momentum ahead. At the same time, domestic demand, also backed by our accommodative monetary policy stance, continues to underpin the economic expansion in the euro area. The strength of the labour market, as reflected in ongoing employment gains and rising wages, still supports private consumption. Moreover, business investment is benefiting from domestic demand, favourable financing conditions and improving balance sheets. Residential investment remains robust. In addition, the expansion in global activity is still expected to continue, supporting euro area exports, although at a slower pace.

This assessment is broadly reflected in the December 2018 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 1.9% in 2018, 1.7% in 2019, 1.7% in 2020 and 1.5% in 2021. Compared with the September 2018 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised slightly down in 2018 and 2019.

The risks surrounding the euro area growth outlook can still be assessed as broadly balanced. However, the balance of risks is moving to the downside owing to the persistence of uncertainties related to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility.

According to Eurostat’s flash estimate, euro area annual HICP inflation declined to 2.0% in November 2018, from 2.2% in October, reflecting mainly a decline in energy inflation. On the basis of current futures prices for oil, headline inflation is likely to decrease over the coming months. Measures of underlying inflation remain generally muted, but domestic cost pressures are continuing to strengthen and broaden amid high levels of capacity utilisation and tightening labour markets, which is pushing up wage growth. Looking ahead, underlying inflation is expected to increase over the medium term, supported by our monetary policy measures, the ongoing economic expansion and rising wage growth.

This assessment is also broadly reflected in the December 2018 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.8% in 2018, 1.6% in 2019, 1.7% in 2020 and 1.8% in 2021. Compared with the September 2018 ECB staff macroeconomic projections, the outlook for HICP inflation has been revised slightly up for 2018 and down for 2019.

Turning to the monetary analysis, broad money (M3) growth stood at 3.9% in October 2018, after 3.6% in September. Apart from some volatility in monthly flows, M3 growth continues to be supported by bank credit creation. The narrow monetary aggregate M1 remained the main contributor to broad money growth.

In line with the upward trend observed since the beginning of 2014, the growth of loans to the private sector continues to support the economic expansion. The annual growth rate of loans to non-financial corporations stood at 3.9% in October 2018, after 4.3% in September, while the annual growth rate of loans to households remained unchanged at 3.2%. The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing – in particular for small and medium-sized enterprises – and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that an ample degree of monetary accommodation is still necessary for the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the Governing Council reiterates the need for rebuilding fiscal buffers. This is particularly important in countries where government debt is high and for which full adherence to the Stability and Growth Pact is critical for safeguarding sound fiscal positions. Likewise, the transparent and consistent implementation of the EU’s fiscal and economic governance framework over time and across countries remains essential to bolster the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council welcomes the ongoing work and urges further specific and decisive steps to complete the banking union and the capital markets union.

Further information on the technical parameters of the reinvestments will be released at 15:30 CET on the ECB’s website.

European Commission President Jean-Claude Juncker will meet UK Prime Minister Theresa May later today, with the latter seeking for changes in the Brexit agreement so as to pass UK parliament. Juncker said ahead of the meeting that, “The deal we achieved is the best possible. It’s the only deal possible. There is no room whatsoever for renegotiation.”

Nevertheless, he added “there is room enough to give further clarifications and further interpretations without opening the withdrawal agreement”. But he reiterated that “the withdrawal agreement will not be reopened.”

Regarding the backstop, Juncker somewhat echoed what May has said before. That is, “We have a common determination to do everything to be not in a situation one day to use that backstop but we have to prepare. It’s necessary for the entire coherence of what we have agreed. It’s necessary for Britain and it’s necessary for Ireland. Ireland will never be left alone.”

Eurozone retail sales dropped sharply by -6.1% mom in November, well below expectation of -3.0% mom. Volume of retail trade decreased by -10.6% mom for automotive fuels, by -8.9% mom for non-food products (within this category mail orders and internet increased by 1.8% mom) and by -1.7% mom for food, drinks and tobacco.

EU retail sales dropped -5.0% mom. Among Member States for which data are available, the largest decreases in the total retail trade volume were observed in France (-18.0% mom), Belgium (-15.9% mom) and Austria (-9.9% mom). The highest increases were registered in the Netherlands (+2.6% mom), Croatia (+2.5% mom) and Germany (+1.9% mom).

In an OECD survey report, Deputy Secretary-General Ludger Schuknecht, warned that “China is at a crossroads, facing serious domestic and external challenges to maintaining its strong position over the long-term.”. He urged that “policy should seek to ensure a better functioning economy that delivers stable and inclusive growth for all.”

OECD said China should aim to “further lower import tariffs and dismantle non-tariff barriers and barriers on the entry and conduct of foreign firms, in particular requirements to form joint ventures or transfer technology.” Also, “ongoing fiscal stimulus should avoid directing credit to state-owned enterprises and local governments”

Additionally, there are :wide scope to improve efficiency across the economy, notably by reducing the internal barriers that hinder product market competition and labour mobility.”. And measures include “stronger protection of intellectual property rights; gradual removal of implicit guarantees to state-owned enterprises, allowing them to default; and reduction of state ownership in commercially-oriented, non-strategic sectors.”

The Thomson Reuters/INSEAD Asian Business Sentiment Index dropped sharply from 63 to 53 in Q2. Worries over US-China trade war sent sentiments down to the worst reading since Q2 of 2009. The index tracks companies’ six-month outlook. The survey interviewed 95 companies in 11 Asia-Pacific countries that together contribute about a third of GDP and are home to 45% of the world’s population. It was conducted from May 31 to June 14.

Antonio Fatas, professor at global business school INSEAD said “it was the uncertainty about the trade war and people were worried about the future”. And, “after four quarters of low numbers that now, it’s not just uncertainty. This is a true slowdown in growth. We see activity declining — it’s not just the expectation that activity will decline.”

It’s still early to tell. But trade data from China showed that Trump’s trade policy failed for another month.

It’s clear that China increased imports from other regions in August like EU (10.6% yoy) and AU (34.0% yoy). Import from US slowed drastically to 2.7% yoy. On the other hand, exports to the US still grew steadily at 13.2% yoy comparing to EU (8.3% yoy) and AU (23.3% yoy). In the end, trade surplus with the US grew 18.4% yoy. And, trade surplus with EU just rose 4.0% yoy. Trade deficit with AU has indeed jumped 45.7% yoy.

For year-to-August, exports to USD rose 13.0% yoy while imports rose 10.3% yoy. Trade surplus rose 14.6% yoy. At the same time, imports from EU rose 14.9% yoy, from AU rose 14.6% yoy. Trade surplus with EU just rose 2.6% yoy. And trade deficit with AU rose 12.2%.

In the end, it’s not the size of trade that matters, but how elastic the demand and supply that matter. For now, it seems like the US is maintaining the pace of growth in Chinese imports. But China is quickly turning to other countries for goods.

Below are some more details.

In CNY terms in August, China’s total trade rose 12.7% yoy to CNY 2.71T. Exports rose 7.9% yoy to CNY 1.44T. Imports rose 18.8% yoy to CNY 1.26T. Trade surplus came in at CNY 180B, wider than July’s CNY 177B.

Year-to-August, total trade rose 9.1% yoy to CNY 19.4. Exports rose 5.4% yoy to CNY 10.3T. Imports rose 13.7% yoy to CNY 9.1T. Trade surplus came in at CNY 1246B.

In USD terms in August, total trade rose 14.3% yoy to USD 407B. Exports rose 9.8% yoy to USD 217B. Imports rose 20.0% yoy to 190B. Trade surplus came in at USD 27.9B, narrowed from July’s USD 28.1B.

Year-to-August, total trade rose 16.1% yoy to USD 3.02T. Exports rose 12.2% yoy to USD 1.60T. Imports rose 20.9% to USD 1.41T. Trade surplus came in at USD 193.6B.

Looking at some details, for the month of August:

Exports to EU rose 8.3% yoy to USD 37.0B, imports from EU rose 10.6% yoy to USD 24.9B, trade surplus rose 4.0% to USD 12.1B

Exports to US rose 13.2% yoy to USD 44.4B, imports from US rose 2.7% yoy to USD 13.3B, trade surplus rose 18.4% to USD 31.1B

Exports to AU rose 23.3% yoy to USD 4.3B, imports from AU rose 34.0% yoy to USD 9.0B, trade deficit rose 45.7% to USD -4.7B

For year-to-August

Exports to EU rose 10.7% yoy to USD 265.6B, imports from EU rose 14.9% yoy to USD 180.4B, trade surplus rose 2.6% yoy to USD 84.2B

Exports to US rose 13.0% yoy to USD 303.4B, imports from US rose 10.3% yoy to USD 110.8B, trade surplus rose 14.6% to USD 192.6B

Exports to AU rose 18.1% yoy to USD 30.1B, imports from AU rose 14.6% yoy to USD 71.2B, trade deficit rose 12.2% yoy to USD -41.2B.

Swiss GDP grew faster than expected by 0.7% qoq in Q2, versus expectation of 0.5% qoq. The government also raised growth forecast for this year.

A government economist Ronald Indergand said that “for the year as a whole we could be looking at a growth rate much nearer to the 3 percent rate than 2 percent, which would be above the long-term average.”

In the prior forecast, the government projected Swiss GDP to grow 2.4% in 2018, comparing to 1.6% in 2017.

Eurozone PMI Services was finalized at 51.6, down from August’s 53.5. PMI Composite was finalized at 50.1, down from August’s 51.9. That’s the lowest level since June 2013. Looking at the member states, Germany PMI Services dropped to 48.5, an 83-month low. Italy rose to 2-month high of 50.6. France hit 5-month low of 50.8. Ireland hit 78-month low of 51.0. Spain also hit 2-month low at 51.7.

Chris Williamson, Chief Business Economist at IHS Markit said:

“The eurozone economy ground to a halt in September, the PMI surveys painting the darkest picture since the current period of expansion began in mid-2013. GDP looks set to rise by 0.1% at best in the third quarter, with signs of further momentum being lost as we head into the fourth quarter, meaning the risk of recession is now very real. Inflows of new business are falling at the fastest rate for over six years and employment growth has hit the lowest since early 2016. Companies are increasingly looking to reduce overheads and tighten belts in the face of falling demand and an uncertain outlook.

“The downturn also shows further signs of spreading from manufacturing to services. While the goods-producing sector is stuck in its deepest downturn since 2012, the service sector has also seen its growth rate slow sharply to one of the weakest for six years.

“The deteriorating picture is being led by a downturn in Germany, but France and Italy are also close to stalling and Spain has seen growth slow to the joint-lowest in around six years.

“The growing risk of recession, coupled with a further moderation of inflationary pressures, will add to expectations that the ECB will need to do more to stimulate the economy in coming months.”

ECB President Christine Lagarde, said at Bundesbank event today that the central bank has “already done a lot” in fighting inflation, referring to the series of rate hikes. Now, given the “amount of ammunition” being deployed, ECB is positioned to “observe very attentively”.

With observations on how tightening have impacted people’s economic life, ECB can decide, “how long we have to stay there and what decision we have to make — up or down, she added.

However, despite these efforts, Lagarde emphasized that “the battle is not over and we’re certainly not declaring victory.”

According to the latest data from People’s Bank of China, the country’s foreign exchange reserves dropped to a five month low in April. Reserves dropped USD 17.97B in April from USD 3.143T to USD 3.125T. In SDR terms, Foreign currency reserves rose 11.3 B from 2.162T to 2.173T.

Gold reserves was unchanged at 59.24 Million oz.

Total reserves dropped from USD 3.240T to USD 3.221T. In SDR terms, total reserves rose from 2.229T to 2.240T.

Kevin Hassett, chairman of the Council of Economic Advisers of the US, said in an interview yesterday that Fed Chair Jerome Powell’s job is 100% safe. He told the WSJ that “The president has voiced policy differences with Jay Powell, but Jay Powell’s job is 100% safe. The president has no intention of firing Jay Powell”.

In addition to Trump’s dissatisfaction on Powell, there were also reports that he has turned his anger to Treasury Secretary Steven Mnuchin. Mnuchin is the one whose’s meeting Powell once a week regularly. And it’s said that Trump is considering to add one of his advisers to the regular meetings. But Hassett said “I am highly confident that the president is very happy with Secretary Mnuchin.”

Canadian Foreign Minister Chrystia Freeland attended the Munich Security Conference over the weekend. There she also met US House Speaker Navy Pelosi and urged to remove the steel and aluminum tariffs. Freeland noted that Canada is now in the process of domestic ratification of the so called USMAC, US-Mexico-Canada agreement on trade. And Canada’s position remains strongly opposed to the section 232 steel tariffs. She also told reporters that “the Canada position is now that we have concluded (USMCA) that is all the more reason why the tariffs must be lifted.”

Separately at the conference, Freeland also urged to reinforce “rules-based international order”. And she proposed to bring together specific coalitions around specific issues.”

Two central banks will announce monetary policy decisions today. BoE is generally expected to deliver a back-to-back rate hike and raise Bank Rate by 25bps to 0.50%. The central bank would also reveal the approach to wind down the GBP 895B asset purchases. Looking ahead, more tightening is expected ahead to bring the Bank Rate to 1.00% level by the end of the year. That should be reflected in the new economic projections in the Monetary Policy Summary.

On the other hand, ECB is expected to stand pat and maintain a cautious tone even though inflation surged to another record in January. Markets are seeing the first rate hike, at 10bps, by July. But President Christine Lagarde would likely talk down such expectations.

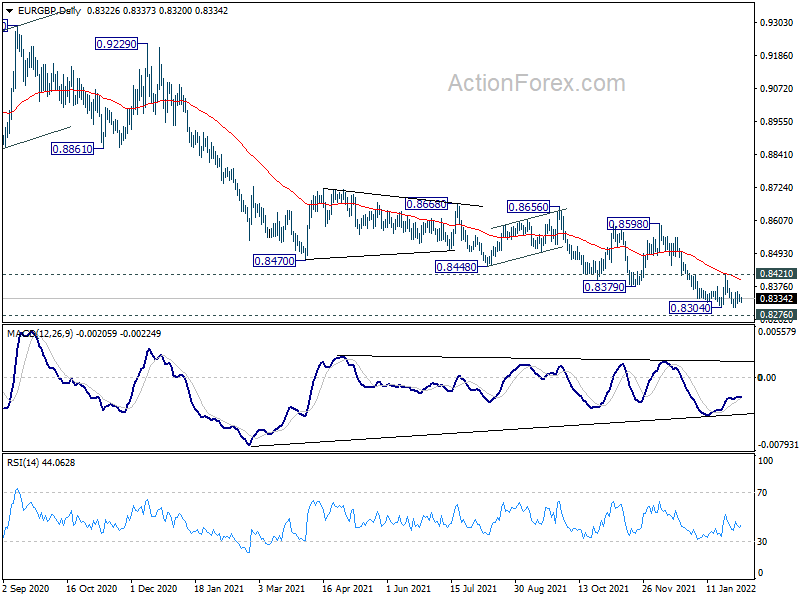

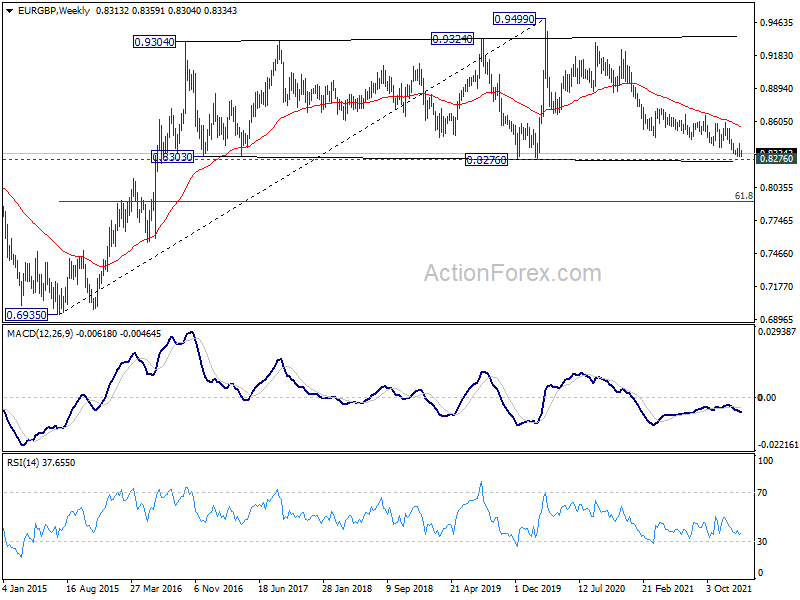

EUR/GBP is a pair to watch today. It should be noted that it’s now very close to a key long term support level at 0.8276, with bullish convergence condition in daily MACD. The conditions are there for a trend reversal. Break of 0.8421 resistance will complete a small double bottom pattern (0.8304, 0.8304), and bring stronger rebound. Further break of 0.8598 resistance should confirm medium term bottoming and turn outlook bullish.

However, sustained break of 0.8276 would argue that fall from 0.9499 is developing into a long term down trend rather than a correction. Deeper decline would then be seen for the rest of the year towards 61.8% retracement of 0.6935 to 0.9499 at 0.7917, and possibly below.

RBA minutes: USD appreciation raised risks for emerging economies, but helpful to Australia

In the minutes of October 2 meeting, RBA noted that global economic conditions had continued to be positive for Australia, despite risks including trade policies. Also, elevated energy and bulk commodity prices supported its terms of trade. Broad based appreciation of the US dollar “had raised risks for some economies, particularly the more fragile emerging market economies”. But the “resultant modest depreciation of the Australian dollar was likely to have been helpful for domestic economic growth.

Domestically, RBA maintained that GDP growth would be “above potential over the following two years”. Forward-looking indicators of labour demand continued to point to above-average growth”. And wage growth is expected increase “gradually”. However, subdued household income growth remained an “important source of uncertainty for the outlook for consumption and inflation.”

Overall, RBA also maintained that ” the next move in the cash rate was more likely to be an increase than a decrease.” However, “since progress on unemployment and inflation was likely to be gradual, they also agreed there was no strong case for a near-term adjustment in monetary policy.”

Full minutes here.