Fed Governor Christopher Waller said in a speech yesterday, “Inflation is far from the FOMC’s goal and not likely to fall quickly. This is not the inflation outcome I am looking for to support a slower pace of rate hikes or a lower terminal policy rate”

Separately, Cleveland Fed President Loretta Mester echoed and said, “We have to bring interest rates up to a level that will get inflation on that 2% path, and I have not seen the compelling evidence that I need to see that would suggest that we could start reducing the pace at which we’re going,”

Chicago Fed President Charles Evans said, “We have to look at the momentum in sort of that central component of inflation, and that’s really the part that I believe has most of my colleagues and myself nervous about.” Be he declined to comment on whether Fed would continue with 75bps hike and noted, we “will have a discussion about that.”

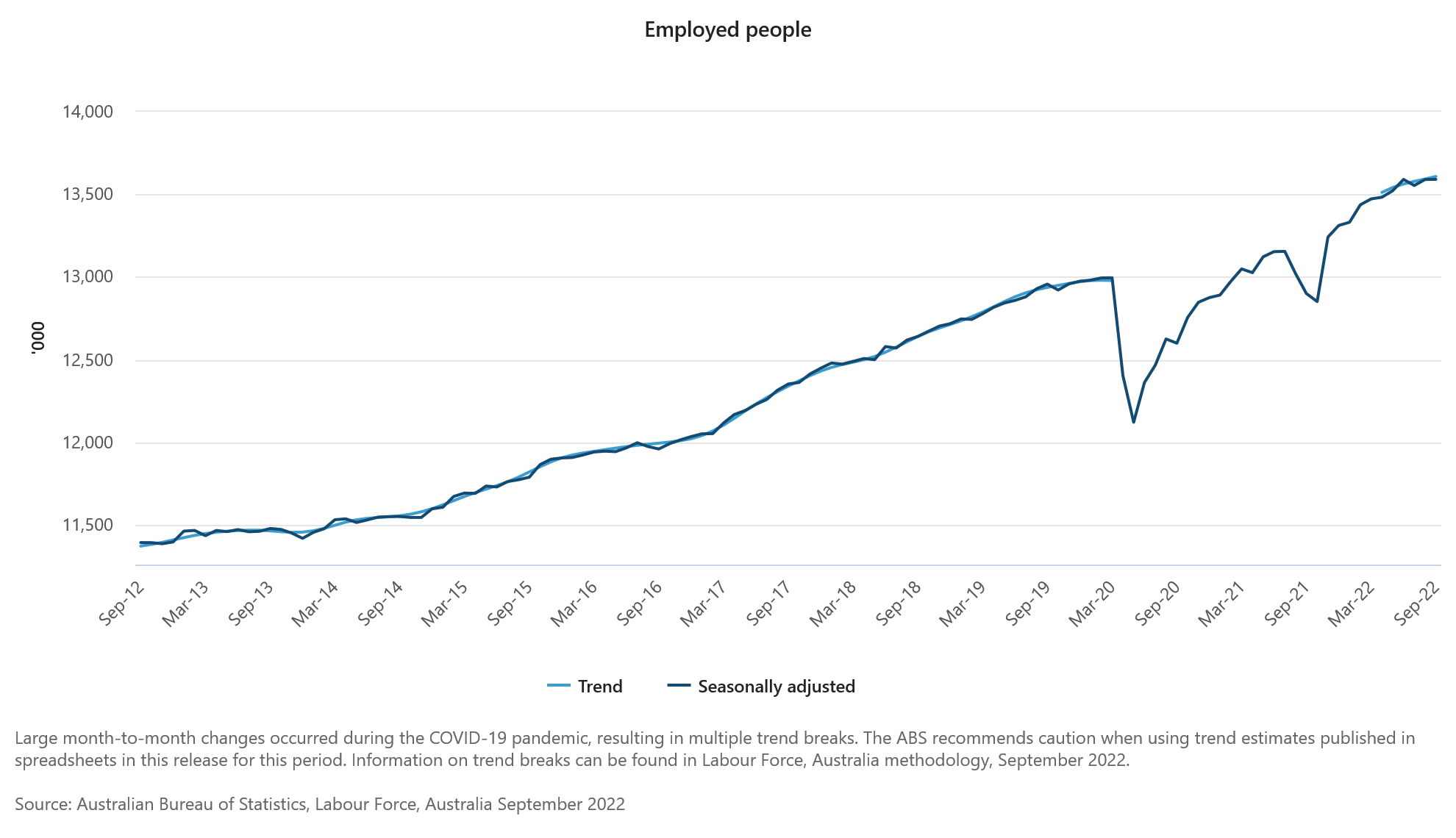

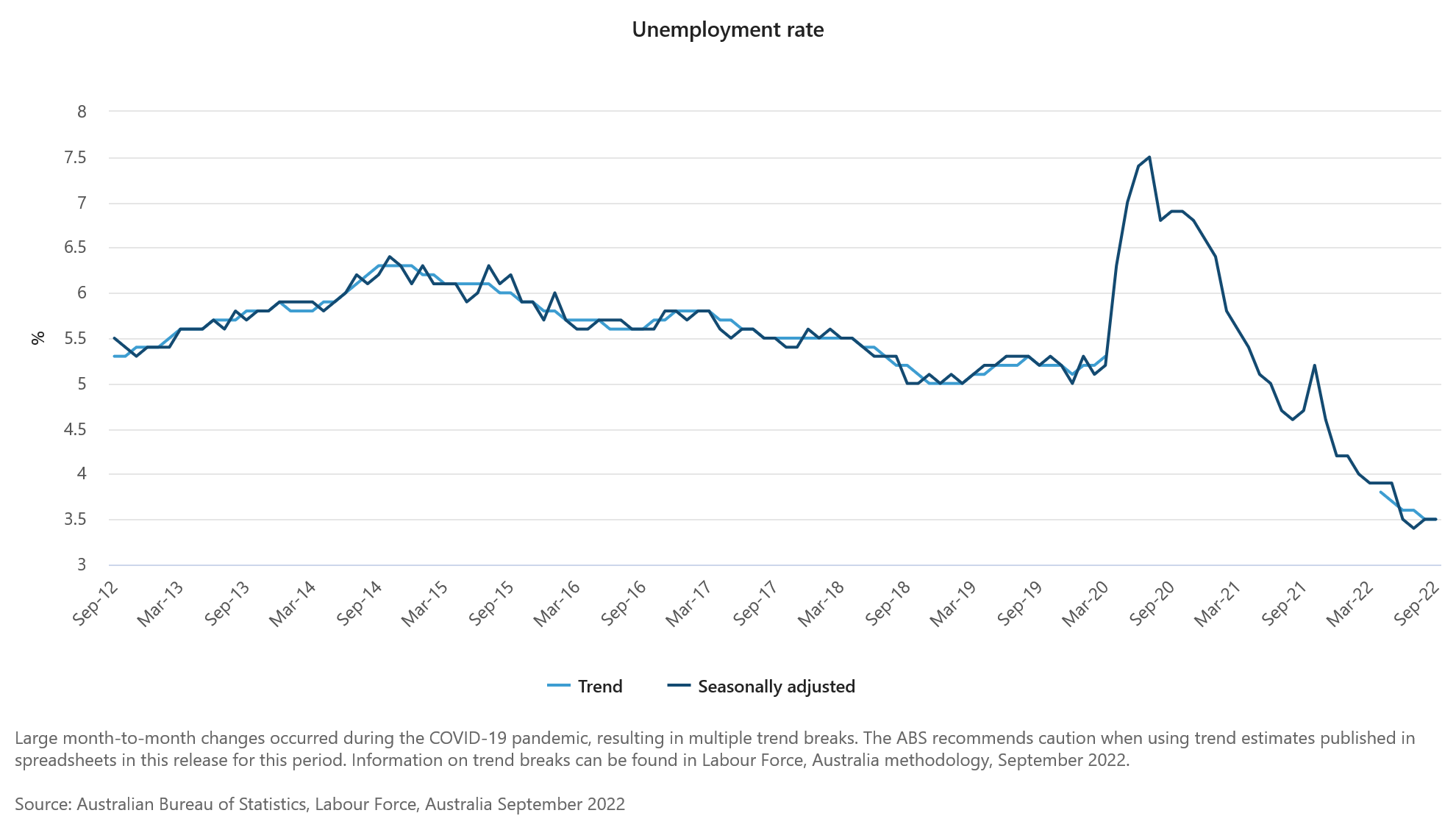

NZD/USD jumps as strong job data supports another RBNZ hike

New Zealand Dollar surges broadly today, as strong job growth data together with record annual wages growth basically seal the deal for another RBNZ rate hike on May 24.

Technically, NZD/USD’s fall from 0.6381 should have completed at 0.6110 already, and further rise is now in favor back towards this resistance. The favored case is that current rise is merely the third leg of the sideway pattern from 0.6083. Outlook remains bearish as long as 0.6381 resistance holds, for resumption of the corrective decline from 0.6537 at a later stage. Break of 0.6160 minor support should bring deeper fall through 0.6083.

Nevertheless, firm break of 0.6381 will argue that the correction from 0.6537 has completed, and the whole rally from 0.5511 might then be ready to resume through 0.6537 high.