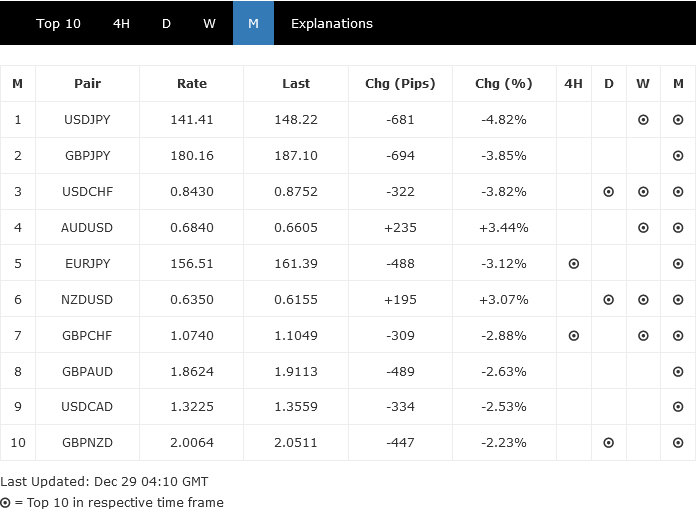

Risk aversion seems to be the main theme in the markets today, as Brexit and NAFTA(?) take a back seat. Instead, selloff in Turkish Lira and stocks are what’s driving the forex markets. Yen is trading as the strongest one for today, followed by Dollar and then Swiss Franc. Yen and the Swissy are clearly benefiting from risk aversion. The greenback continues to take advantage of slump in emerging market currencies.

Meanwhile, commodity currencies are all weak, including Canadian, Australian and New Zealand Dollar. Sterling also retreats mildly as the lift from Brexit optimism fades. Make no mistake that it’s still likely to have deal when both sides want to, but they have to deliver. And just like Canada-US trade talks, eyes will be on whether there is a conclusion by the end of tomorrow.

US stocks and yields are trading generally in red. DOW is down -0.40%, S&P 500 down -0.28%, NASDAQ down -0.07%. But remember that both S&P 500 and NASDAQ are on record runs. So such shallow retreat does nothing to change the trend. In Europe, FTSE closed down -0.62%, DAX down -0.54% and CAC down -0.42%.

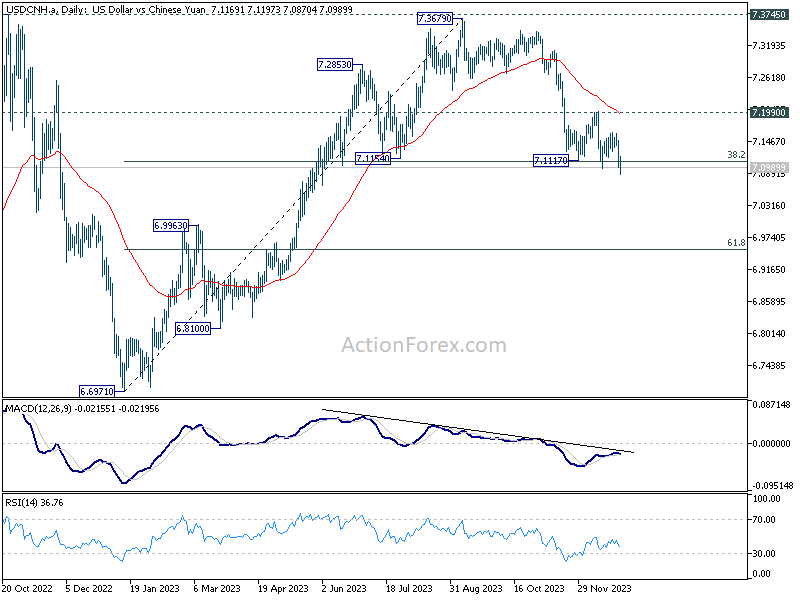

USD/CNH (offshore Yuan), is trading up more than 0.6% at the time of writing. Break of the near term channel resistance argues that pull back from 6.9586 could completed with three waves down to 6.7776 already. Immediate focus is on 6.8959, for tomorrow and early next week. Break will bring rest of 6.9586 and even resume the down trend in Yuan.

And as we mentioned early, USD/TRY’s break of 61.8% retracement of 7.2068 to 5.6919 at 6.6281 could pave the way to retest 7.2069 high.

Selloff in emerging market currency could come back into spot light. If that happens, Dollar and Yen would be the main beneficiary.

German government to revise down growth forecasts to 1.8% in both 2018 and 2019

Reuters reported, according to a document they obtained, German government slashed growth forecast for both 2018 and 2019 in the update to be released tomorrow. Growth is now projected to be at 1.8% in both 2018 and 2019, down from prior projections of 2.3% and 2.1% respectively. For 2020, growth is expected to be unchanged at 1.8%. Weak global trade, lowered state consumption and softer auto sector are the causes for slower than expected growth.

Inflation is projected to be at 1.9% in 2018 and rise further to 2.0% in 2019. The document also noted that “in view of the strong expansion of disposable income and moderate inflation, private consumption is likely to pick up noticeably.” House hold spending is expected to grow 1.6% in 2018 and 2.0% in 2019. State consumption is projected to grow 1.4% in 2018 and 2.5% in 2019. State investment is project to rise 5.9% in 2018 and 5.2% in 2019.

According to IMF’s latest forecasts released earlier this week, German growth is projected at 1.9% in 2018 and 1.9% in 2019, revised down from April forecasts of 2.5% and 2.0% respectively.