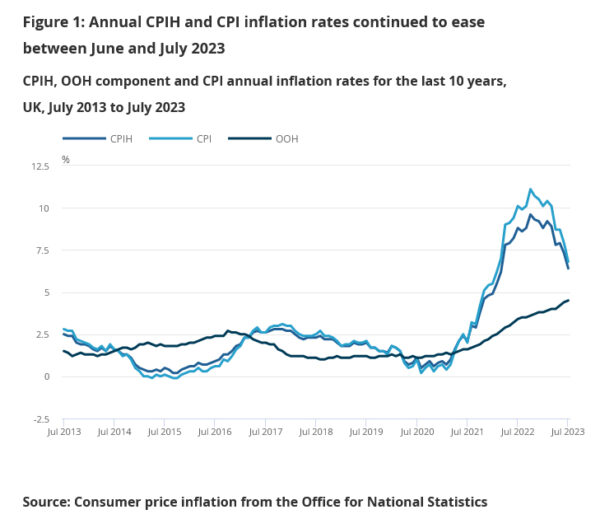

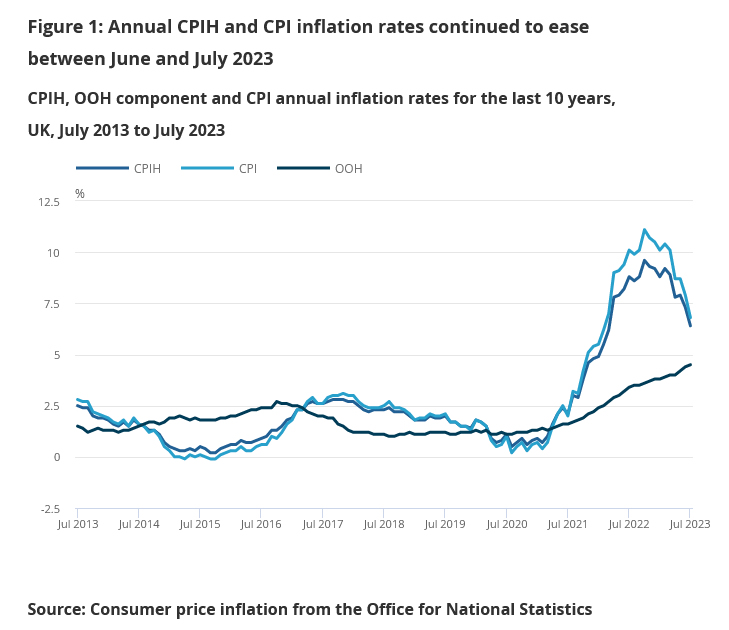

July saw a marked deceleration in UK’s CPI, falling from 7.9% yoy to 6.8% yoy , precisely in line with market expectations. Core CPI, which strips out variables like energy, food, alcohol, and tobacco, stood unchanged at 6.9% yoy, above the expected 6.8%.

CPI figures pertaining to goods showed a noticeable slowdown, dropping from 8.5% yoy to 6.1% yoy. On the flip side, CPI services ramped up from 7.2% yoy to 7.4% yoy , registering its peak since the staggering 9.5% yoy rate observed in March 1992.

On a month-to-month analysis for July, CPI receded by -0.4%, a figure slightly above than forecasted decline of -0.5%. Core CPI saw a monthly rise of 0.3% mom. While the CPI for goods plunged by -1.7% mom. , services CPI exhibited an increase, registering growth of 1.0% mom. .

Office for National Statistics remarked, “The slowdown in the annual CPI rate into July 2023 was driven by downward contributions to change from 8 of the 12 divisions.”

Notably, housing and household services emerged as the primary sectors applying downward pressure. Expanding on this, ONS stated, “Within this division, the downward effect came mainly from gas and electricity.”

Full UK CPI release here.

US ADP employment rises 192k in Apr, vs exp 180k

US ADP private employment grew 192k in April, above expectation of 180k. By sector, goods-producing jobs rose 47k, service-providing jobs rose 145k. By establishment size, small companies added 38k jobs, medium companies added 62k, large companies added 98k.

Year-over-year pay gains for job-stayers were little changed in April at 5%. Pay growth for job- changers fell from 10.1% in March to 9.3%.

“Hiring was broad-based in April,” said Nela Richardson, chief economist, ADP. “Only the information sector – telecommunications, media, and information technology – showed weakness, posting job losses and the smallest pace of pay gains since August 2021.”

Full US ADP release here.