Oil prices surges sharply in Asian session and there was a significant influx into safe-haven assets such as Gold, Dollar, Swiss Franc, and Japanese Yen.

This market reaction was triggered by escalating tensions in the Middle East, following a report by ABC News on a retaliatory missile strike by Israel against Iran. Meanwhile, Iran’s Fars news agency also reported that explosions were heard near the Isfahan airport,m even though the causes were unknown.

The missile launches are continuation of hostilities following last Saturday when Iran targeted Israel with over 300 drones and missiles, a majority of which were intercepted by Israel and its allies.

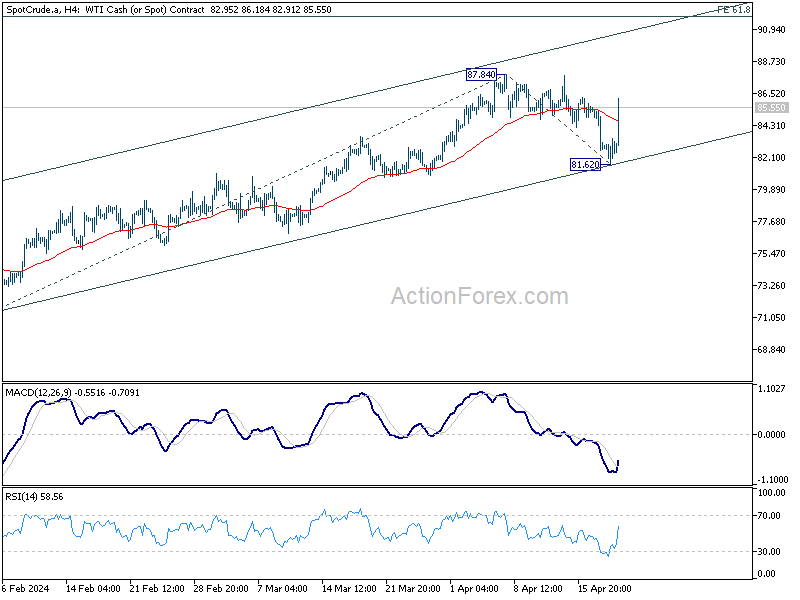

WTI oil’s strong rebound today suggests that corrective pullback from 87.84 has completed at 81.62 already. Further rise would be seen to retest 87.84 resistance first. Decisive break there will resume whole rally from 67.79 and target 61.8% projection of 71.32 to 87.84 from 81.62 at 91.82 next.

Also, note that rise from 67.79 is seen as the third leg of the pattern from 63.67 (2023 low). Hence, break of 95.50 is possible in the medium term, depending on whether WTI could sustain its upside momentum.

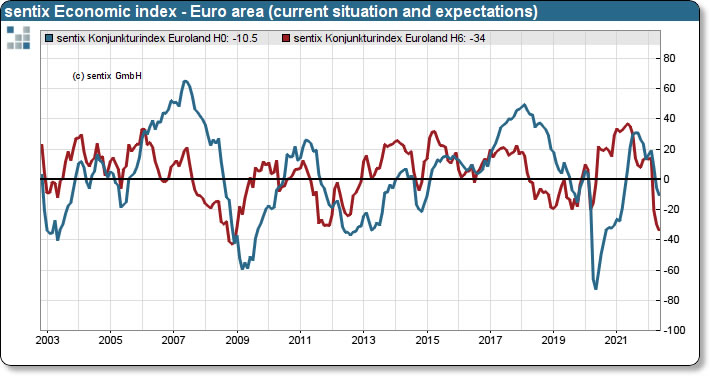

German ZEW economic sentiment rose to 31.7, but current situation dropped to 12.5

Germany ZEW Economic Sentiment rose to 31.7 in November, up from 22.3, well above expectation of 20.3. That’s also the first rise since May. Current Situation, however, worsened again and dropped sharply from 21.6 to 12.5, well below expectation of 19.4.

Eurozone ZEW Economic Sentiment rose from 21.0 to 25.9, above expectation of 20.6. Current situation dropped -4.3 pts to 11.6. Inflation expectations for Eurozone dropped very sharply by -31.4 pts to -14.3. This shows that the experts expect the inflation rate in the eurozone to decline over the next six months.

“Financial market experts are more optimistic about the coming six months. However, the renewed decline in the assessment of the economic situation shows that the experts assume that the supply bottlenecks for raw materials and intermediate products as well as the high inflation rate will have a negative impact on the economic development in the current quarter. For the first quarter of 2022, they expect growth to pick up again and inflation to fall both in Germany and the eurozone,” comments ZEW President Professor Achim Wambach on current expectations.

Full release here.