UK PMI Manufacturing recovered to 48.3 in September, up from 47.4 and beat expectation of 47.0. However, Markit noted that downturn continues as rate of jobless accelerated to the worst level since February 2013. New orders and output also fell further. But purchasing and input stocks rose as Brexit preparations restarted.

Rob Dobson, Director at IHS Markit, which compiles the survey:

“The UK manufacturing downturn continued in September, adding to signs that the sector may be sliding into recession. Output, new orders and employment all fell further as rising political, trade and economic uncertainties exacerbated concerns about Brexit.

“Some manufacturers noted increased inventory building activity in preparation for the forthcoming exit date, but the impact of such Brexit-related stock building was dwarfed by weakening demand for other customers, due in part to clients routing supply chains away from the UK.

“The rate of job losses accelerated to a six-and-a-half- year high, highlighting how manufacturers are increasingly seeking to cut costs. Similarly, the investment goods sector was especially hard hit in September, seeing the sharpest drops in production and new business, as clients reined in capital spending while conditions remained volatile.

“The shroud of uncertainty also weighed on manufacturers’ confidence, which remained at one of its lowest ebbs in the survey history. These headwinds all ensure that manufacturing will likely remain a drag on UK economic growth during the months ahead.”

Full release here.

Into US session: Yen stays strongest even European stocks pared losses

Entering into US session, risk aversion seems to have eased a little bit in European markets, with major indices pared back much of earlier losses. But Yen remains overwhelmingly the strongest one, thanks to falling European yields. Canadian Dollar follows as the second strongest as WTI crude oil manages to stay in tight range above 45, for now. Dollar is the third strongest.

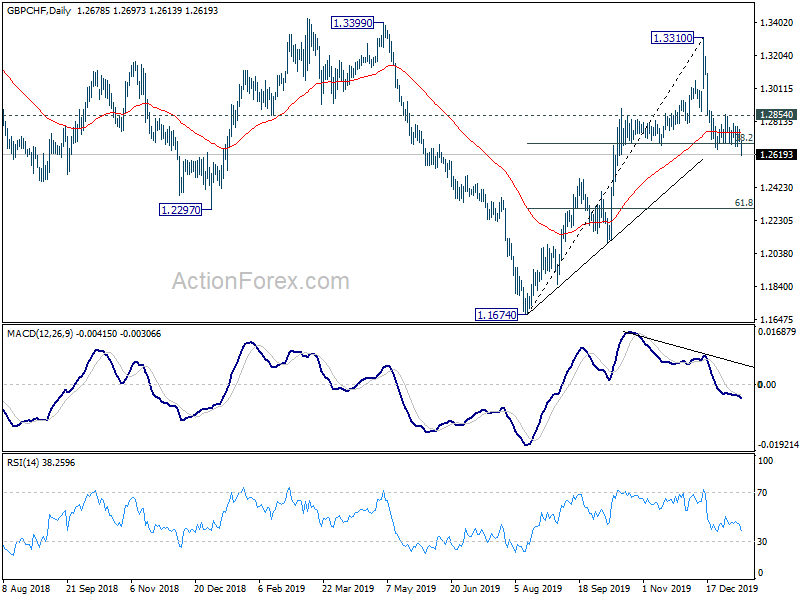

Meanwhile, Sterling is the worst performing one despite stronger than expected PMI manufacturing. The Pound is reversing the unexpected strong gains on Monday. Australian Dollar follows as second weakest. Euro and Swiss franc trail.

In Europe:

Earlier in Asia: