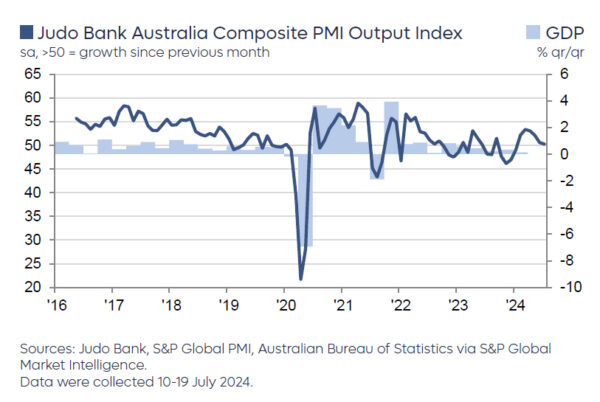

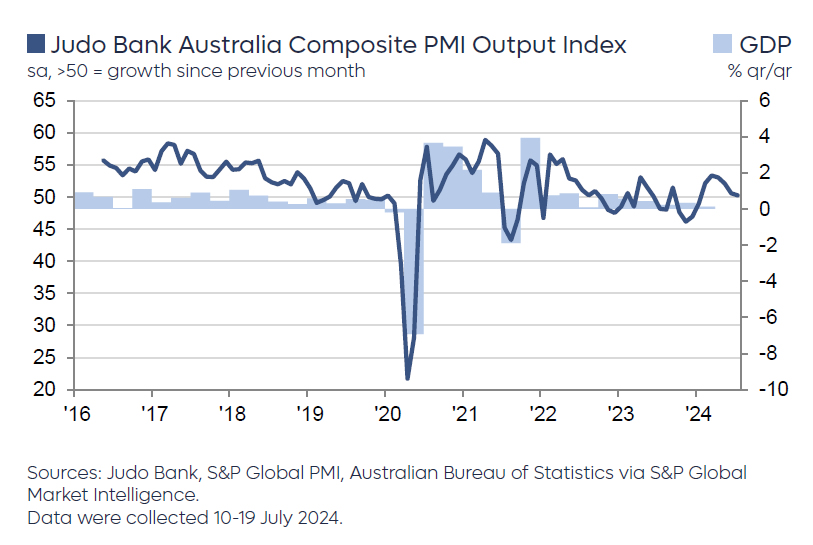

Australia’s PMI Manufacturing saw a marginal improvement in July, rising slightly from 47.2 to 47.4. Conversely, PMI Services dropped to a six-month low, moving from 51.2 to 50.8. PMI Composite also decreased from 50.7 to 50.2, the lowest in six months.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that despite a further moderation in the composite output index, “there are no signs of a significant slowdown in Australian business activity in 2024.” He noted that while manufacturing continues to struggle, services sector is still experiencing better activity compared to the end of 2023.

Hogan also mentioned that the impact of recent tax cuts and cost-of-living support measures has yet to fully manifest in the business conditions and should positively affect consumer spending in future months. Insights from the upcoming final PMIs for July and the reports for August are expected to provide a clearer picture of these effects.

Despite softer activity levels, inflation pressures have not eased significantly. The services sector saw a notable increase in input costs, which rose four points to 63.3—the highest since November 2023. In contrast, manufacturing input costs rose only slightly and are near their lowest in four years. The composite output price index nudged up to 54.1 in July, indicating a small increase but suggesting that inflation is likely stabilizing around an annualized rate of 4% as of mid-2024.

Full Australia PMI release here.

RBA’s Kent: Some further tightening may be required

In a speech, RBA Assistant Governor, Chris Kent, indicated that while the effects of previous monetary tightening have not yet been fully realized, “some further tightening ” might be on the horizon to keep inflation in check.

Kent asserted that the policies currently in place are beginning to stymie demand growth, a crucial step towards mitigating inflation.

“The lags of transmission mean that some further effects of rate increases to date are still to be felt through the economy, which will provide further impetus to lower inflation in the period ahead,” he added.

However, with inflation persisting at elevated levels, Kent hinted at the necessity for additional measures. “The Board is paying close attention to economic developments here and overseas, and some further tightening of monetary policy may be required to ensure that inflation, which is still too high, returns to target in a reasonable timeframe.”

Full speech of RBA Kent here.