US stocks surged, with DOW hitting new record, while treasury yields and the Dollar tumbled following Fed’s decision to leave interest rates unchanged at 5.25-5.50%. This decision, widely anticipated by the markets, was overshadowed by the Fed’s indication of potential rate cuts in 2024. Fed suggested that three 25 bps cuts could be implemented next year, to bring federal funds rate back to 4.50-4.75%.

Fed Chair Jerome Powell, in the post-meeting press conference, acknowledged the emerging discussion within about reducing policy restraint. Powell stated, “The question of when it will be appropriate to begin dialing back the amount of policy restraint in place begins to come into view, and is clearly a topic of discussion out in the world and also of discussion for us at our meeting today.” He further noted the general expectation that this issue will be a key focus for Fed going forward.

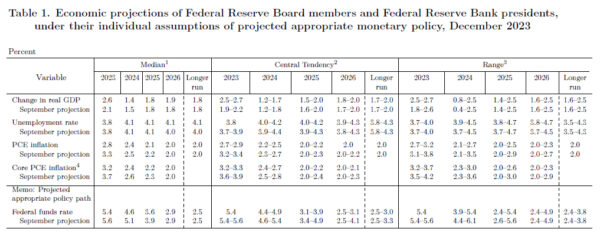

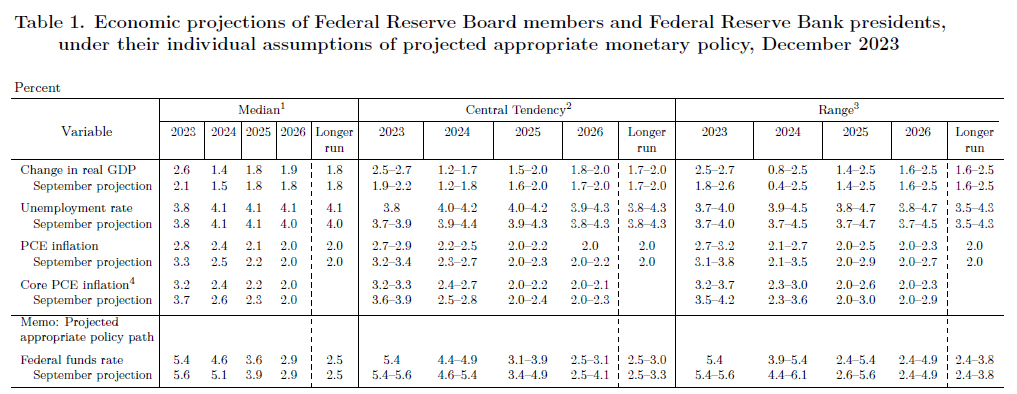

The new economic projections present a detailed outlook. The median forecasts indicate that federal funds rate will decrease from the current 5.4% to 4.6% in 2024, further reducing to 3.6% in 2025, and eventually to 2.9% in 2026. The longer-run federal funds rate is held steady at 2.50%. The central tendency for 2024 is at 4.4-4.9%, suggesting a relatively narrow range, and stable rate expectation.

The projections for GDP growth show a slowdown from 2.6% in 2023 to 1.4% in 2024, followed by a rebound to 1.8% in 2025 and 1.9% in 2026. The unemployment rate is expected to increase from 3.8% in 2023 to 4.1% in 2024 and then stabilize at this level through 2026.

Regarding inflation, headline PCE inflation is forecasted to decrease from 2023’s 2.8% to 2.4% in 2024, 2.1% in 2025, and 2.0% in 2026. Similarly, core PCE inflation is projected to slow down from 3.2% in 2023 to 2.4% in 2024, and then to 2.2% in 2025 and 2.0% in 2026.

Some FOMC reviews here.

US new home sales rose to 692k, highest since Nov 2017

US sales of new single-family houses rose to 692k in March, up from 662k, well above expectation of 647k. That’s also the highest level since November 2017. Also from US, house price index rose 0.3% mom in February, below expectation of 0.6% mom.