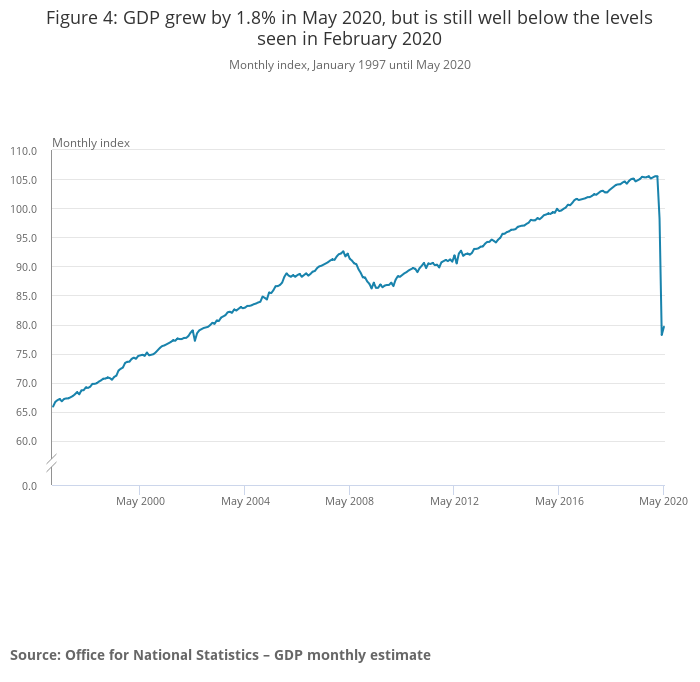

UK GDP grew notably by 1.8% mom in May but the rebound was somewhat disappointing and missed expectation of 5.0% mom. Production jumped sharply by 6.0% mom, with manufacturing up 8.4%. Services rose 0.9% mom while construction rose 8.2% mom. But all were insufficient to recover the contraction in April (production -20.2% mom, manufacturing -24.4% mom, services -18.9% mom, construction -40.2% mom. Agriculture continued contraction by -6.2% mom.

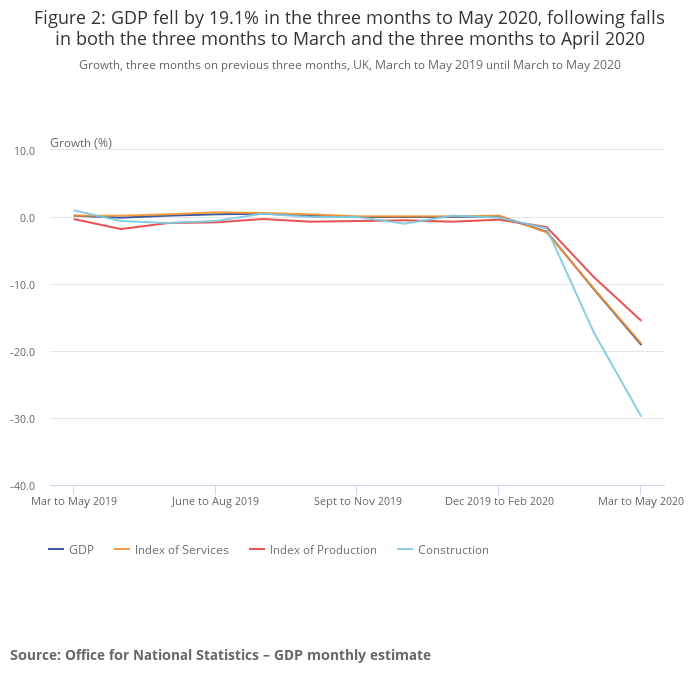

For the three months to May, GDP dropped by -19.1% 3mo3m. Production dropped -15.5% 3mo3m. Manufacturing dropped -18.0% 3mo3m. Service dropped -18.9% 3mo3m. Construction dropped -29.8% 3mo3m. Agriculture dropped -6.3% 3mo3m.

Jonathan Athow, Deputy National Statistician for Economic Statistics, said: “Manufacturing and house building showed signs of recovery as some businesses saw staff return to work. Despite this, the economy was still a quarter smaller in May than in February, before the full effects of the pandemic struck. In the important services sector, we saw some pickup in retail, which saw record online sales. However, with lockdown restrictions remaining in place, many other services remained in the doldrums, with a number of areas seeing further declines.”

Falls in World Trade Outlook indicator could be linked to increased trade tensions

The World Trade Outlook Indicator of the WTO dropped to 101.8 as of May 17, down from 102.3 back in February.

WTO noted that the value remains “above the baseline value of 100” which suggests “continued solid trade growth in Q2. However, it’s “probably at a somewhat slow pace” than Q1.

It also pointed out that the dip in WTOI reflects declines in export orders and air freight. And that “may be linked to rising economic uncertainty due to increased trade tensions.”

Full release here.