In a statement today, ECB Governing Council member Peter Kazimir highlighted his preference delivering the first rate cut in June. Emphasizing the persistent nature of upside inflation risks, Kazimir pointed to factors such as workers’ pay, energy prices, fiscal policy, and the green transition as ongoing concerns that necessitate caution.

Kazimir’s stance is clear: “Rushing isn’t smart and beneficial,” he remarked, underlining the jeopardy to ECB’s credibility from a hasty policy adjustment.

According to him, “Only in June, with new forecast at hand, will the level of confidence reach the threshold.”

Also, he advocates for a “smooth and steady cycle of policy easing,” suggesting that the decision-making process should be grounded in comprehensive and up-to-date economic forecasts.

“Upside inflation risks are alive and kicking,” he asserted, emphasizing the need for vigilance. “The current picture clearly favors staying calm for the coming weeks and delivering the first-rate cut in summer,” he said. “The slowdown in inflation remains fragile — we can’t take it for granted.”

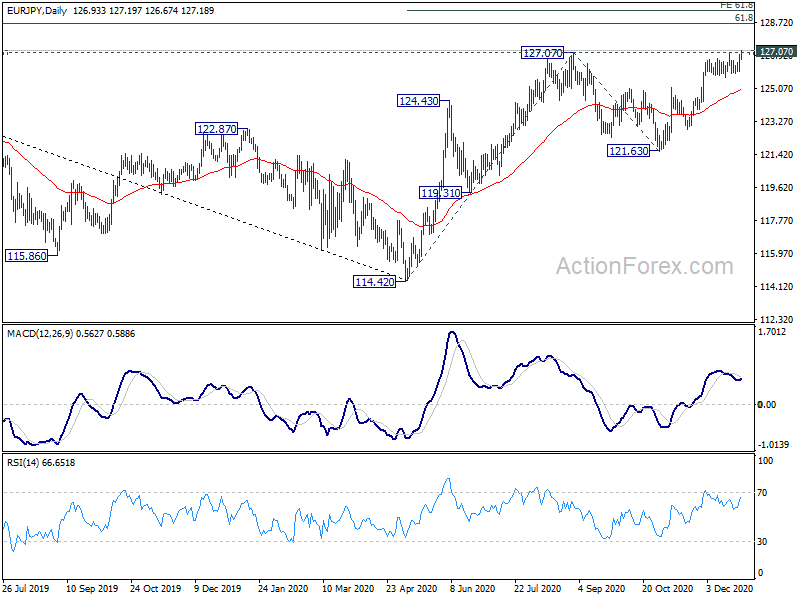

Gold extending decline towards 1817

Gold’s near term decline resumed overnight and broke through 1850.18 support. Near term outlook now stays bearish as long as 1909.57 resistance holds. Next target is 100% projection of 2070.06 to 1889.79 from 1998.23 at 1817.86. The whole fall from 2070.06 is seen as the third leg of the consolidation pattern from 2074.84 (2020 high). Firm break of 1817.86 could prompt more downside acceleration towards 1682.60 to finally finish the pattern.