As the week draws to a close, market attention is squarely on the upcoming US non-farm payroll employment report. The sluggish Dollar is in need of a catalyst from the jobs report to spark a meaningful and sustainable breakout from its recent range against major currencies.

Market expectations are set for NFP to show 180k growth o May, with the unemployment rate steady at 3.9%. Average hourly earnings are expected to increase by 0.3% mom.

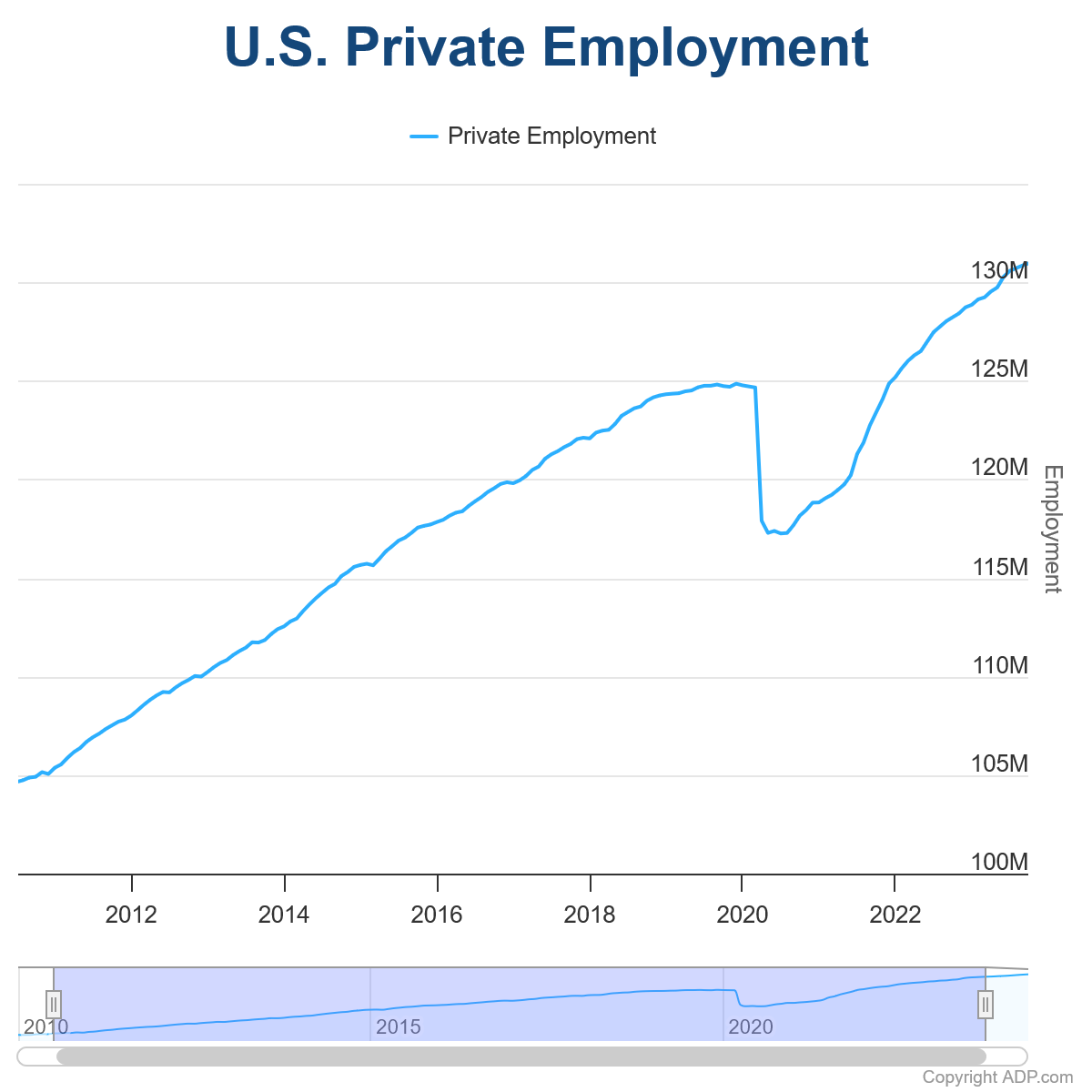

Recent related economic data offers mixed signals. ISM Services employment index rose from 45.9 to 47.1, but still indicating contraction. Conversely, ISM Manufacturing employment index turned to expansion, rising from 48.6 to 51.1. ADP private employment showed a growth of only 152k. Additionally, the four-week moving average of initial jobless claims rose from 210k to 222k, suggesting some softening in the labor market.

While there may be some upside surprises in headline job growth, it is unlikely to significantly exceed expectations. The critical variable remains wage growth, which is essential for gauging underlying domestic inflation pressures, and an important factor influencing the timing of Fed’s first rate cut.

Dollar index dipped to 103.99 this week but struggled to find decisive selling momentum. Further decline is still in favor as long as 105.18 resistance holds. Fall from 106.51 is seen as developing into the third leg of the pattern from 107.34. Any downside acceleration could push DXY through 102.35 support towards 100.61.

However, strong bounce from current level followed by break of 105.18 will revive near term bullishness. Rise from 100.61 would then be ready to resume through 106.51 before reversing.

Australia’s NAB business confidence returns to negative, inflation pressures re-emerge

Australia’s NAB Business Confidence fell from 2 to -3 in May, returning to negative territory. Business conditions also saw a slight decline, dropping from 7 to 6. Specifically, trading conditions decreased from 13 to 10, and profitability conditions fell from 6 to 3. However, employment conditions improved, rising from 2 to 5.

NAB Chief Economist Alan Oster noted pointed out that forward orders are particularly weak in retail, wholesale, and construction sectors, indicating potential challenges ahead. Despite a slowdown in activity, capacity utilization remains above average, suggesting that the “process of bringing supply and demand back into balance remains incomplete”.

Inflationary pressures are re-emerging, with labor cost growth increasing to 2.3% on a quarterly basis, up from 1.5% in April. Purchase cost growth also rose to 1.9%, compared to 1.3% previously. Overall product price growth climbed to 1.1%, up from 0.8%, with retail price growth increasing to 1.6% from 1.0%, and recreation and personal services prices edging up to 1.0% from 0.9%.

Oster concluded that the data presents a “mixed” picture for RBA. There are clear signs of growth challenges, yet inflationary pressures remain a concern. “We expect the RBA to keep rates on hold for some time yet as they navigate through these contrasting risks.”

Full Australia NAB business confidence release here.