BoC is generally expected to continue with tapering today, reducing weekly asset purchases from CAD 3B to CAD 2B. It’s also expected to maintain the projection that first rate hike would happen in H2 of 2022. The focuses would be on new economic projections, in particular, on whether inflation forecasts would be up graded significantly.

Here are some previews on BoC:

- BOC Preview – Hawkish Stance to Maintain with More Tapering

- BOC Preview: Ready To Continue Tapering, But Does That Mean USD/CAD Will Move Lower?

- Bank of Canada to Taper Again as Loonie Succumbs to Delta Concerns

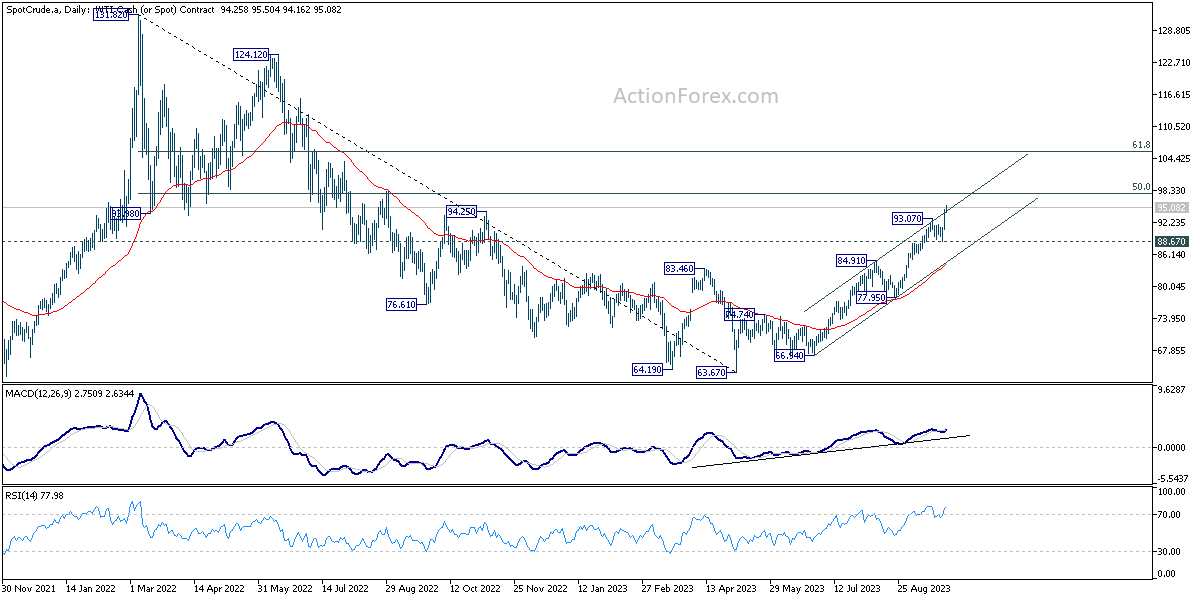

Canadian Dollar’s reaction to BoC’s tapering hasn’t been positive so far. Outlook in EUR/CAD is unclear. Bullish convergence in daily MACD argues that medium term momentum is diminishing. Yet, it failed to sustain above the 55 day EMA, despite rebounding to 1.4913. Also, price actions from 1.4580 are more corrective looking than not. So, we’d see if today’s BoC announce could finally trigger deeper fall back towards 1.4580.

China backs down from tariff escalation, urges continuing negotiations

China’s Ministry of Commerce spokesman Gao Feng said today that “China has ample means for retaliation, but thinks the question that should be discussed now is about removing the new tariffs to prevent escalation of the trade war.” And, “China is lodging solemn representations with the U.S. on the matter.”

Additionally, Gao reiterated the usual rhetoric that “escalation of the trade war won’t benefit China, nor the US, nor the world,” and “the most important thing is to create the necessary conditions for continuing negotiations.” He also repeated Vice Premier Liu He’s comment that China is “willing to solve the problem through consultation and cooperation with a calm attitude, but firmly opposes escalation of trade war.”

The comments suggested that China is backing down from its hard-line stance after recent escalation by US President Donald Trump. Trump tweeted earlier this month that 25% tariffs on some USD 250B in imports from China would rise to 30% come Oct. 1. He also lifted planned levies on USD 300B in Chinese goods due on Sept. 1 and Dec. 15 by 5%.