ECB Executive Board member Isabel Schnabel said in a speech that despite decline in headline inflation, largely due to unwinding of previous supply-side shocks, “underlying price pressures remain stubbornly high,” with domestic factors now becoming the main drivers of inflation.

Given this backdrop, Schnabel emphasized the necessity of maintaining “sufficiently restrictive monetary policy” to steer inflation back to target. She advocated for a data-dependent approach, stating that the bank will continually assess whether current policy is effective in ensuring “a sustained and timely return of inflation to our 2% target.”

To guide this assessment, Schnabel pointed to the need for a comprehensive risk analysis that looks beyond baseline inflation forecasts. This approach accounts for an “exceptionally large degree of uncertainty” in medium-term inflation projections, with risks on both the upside and downside.

Upside risks include stronger-than-expected growth in unit labor costs, firmer corporate pricing power, and the potential for new adverse supply-side shocks. Conversely, downside risks include possibility that impact of current monetary policy may become more pronounced over the medium term.

Notably, Schnabel also raised the issue of real risk-free rates, which have declined recently as investors reassess their expectations for economic growth and inflation. She warned that this decline could potentially “counteract” the ECB’s efforts to control inflation effectively.

Full speech of ECB Schnabel here.

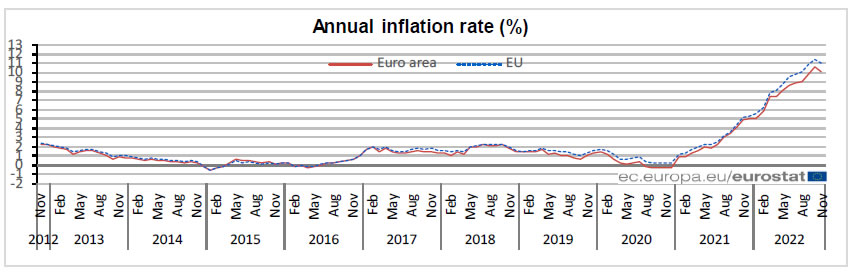

Eurozone CPI finalized at 4.1% yoy in Oct, EU at 4.4%

Eurozone CPI was finalized at 4.1% yoy in October, up from September’s 3.4%. The highest contribution came from energy (+2.21%), followed by services (+0.86%), non-energy industrial goods (+0.55%) and food, alcohol & tobacco (+0.43%).

EU CPI was finalized at 4.4%, up from September’s 3.6% yoy. The lowest annual rates were registered in Malta (1.4%), Portugal (1.8%), Finland and Greece (both 2.8%). The highest annual rates were recorded in Lithuania (8.2%), Estonia (6.8%) and Hungary (6.6%). Compared with September, annual inflation rose in all twenty-seven Member States.

Full release here.