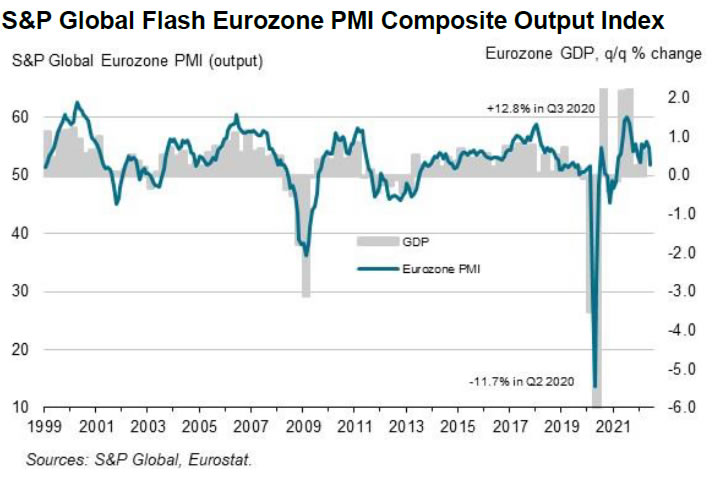

Eurozone PMI Manufacturing dropped from 54.6 to 52.0 in June, below expectation of 53.0. That’s the lowest level in 22 months. PMI Services dropped from 56.1 to 52.8, below expectation of 55.5, a 5-month low. PMI Composite dropped from 54.8 to 51.9, lowest in 16-months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “Eurozone economic growth is showing signs of faltering … Excluding pandemic lockdown months, June’s slowdown was the most abrupt recorded by the survey since the height of the global financial crisis in November 2008…. The slowdown means the latest data signal a rate of GDP growth of just 0.2% at the end of the second quarter, down sharply from 0.6% at the end of the first quarter, with worse likely to come in the second half of the year.”

BoJ Kuroda: Retail level CBDC is an option

BoJ Governor Haruhiko Kuroda said in an online seminar that the central bank has not decided on central bank digital currency (CBDC) yet. But he noted it could be an option for securing a seamless and safe infrastructure.

“CBDC is not the only way, so a national discussion is needed as to how to achieve this goal,” Kuroda said, adding, “retail level CBDC is an option.”

BoJ started the second phase of the CBDC experiments in April. The process will last for around a year.