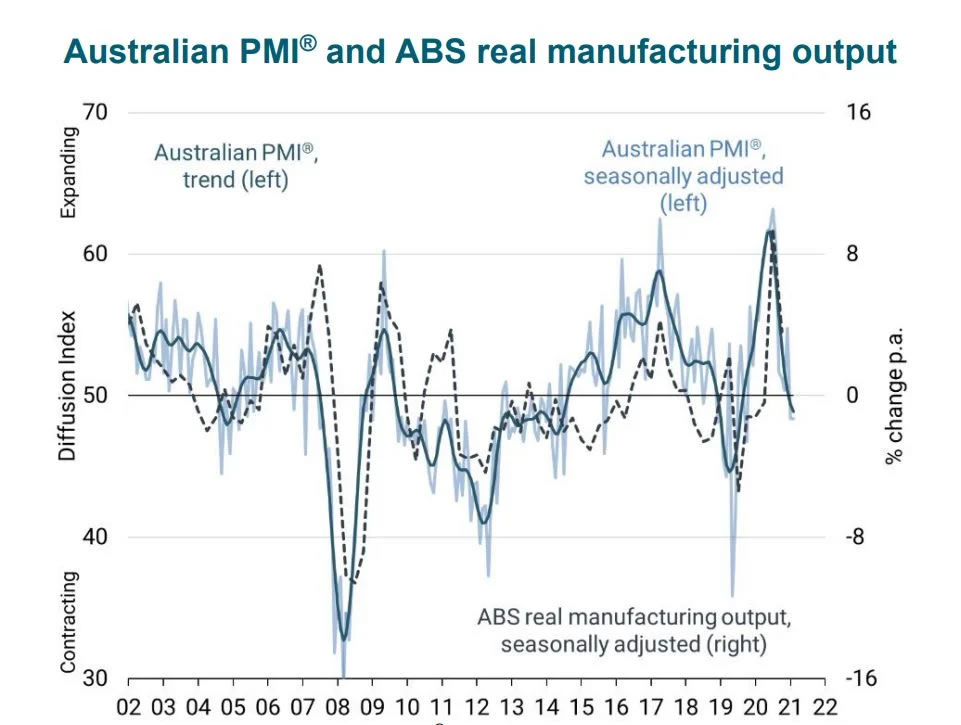

Australia AiG Performance of Manufacturing Index dropped sharply by -6.4 pts to 48.4 in January. Production dropped -0.6 to 51.9. Employment dropped -4.6 to 45.4. New orders dropped -8.0 to 51.3. Supplier deliveries dropped -15.6 to 37.8. Exports dropped -9.5 to 45.1. Input prices rose 4.0 to 82.3. Selling prices dropped -3.3 to 64.8. Wages rose 1.1 to 63.5.

Innes Willox, Chief Executive of Ai Group said: “Australia’s manufacturers reported a modest contraction in performance over December and January as businesses reported further disruptions to supply chains and as staff availability emerged as a major constraint on many businesses. Cost pressures were keenly felt with input prices continuing to rise and the selling prices index indicating only a partial recovery of these costs in the market.”

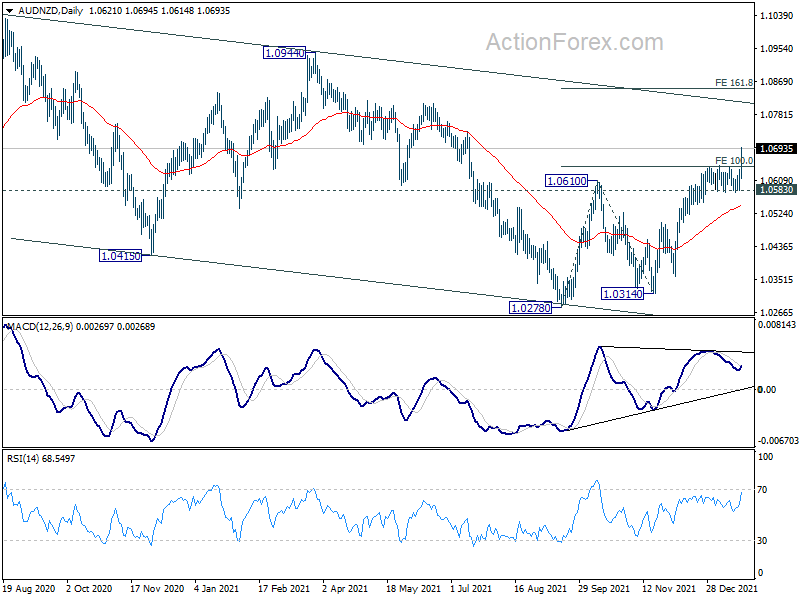

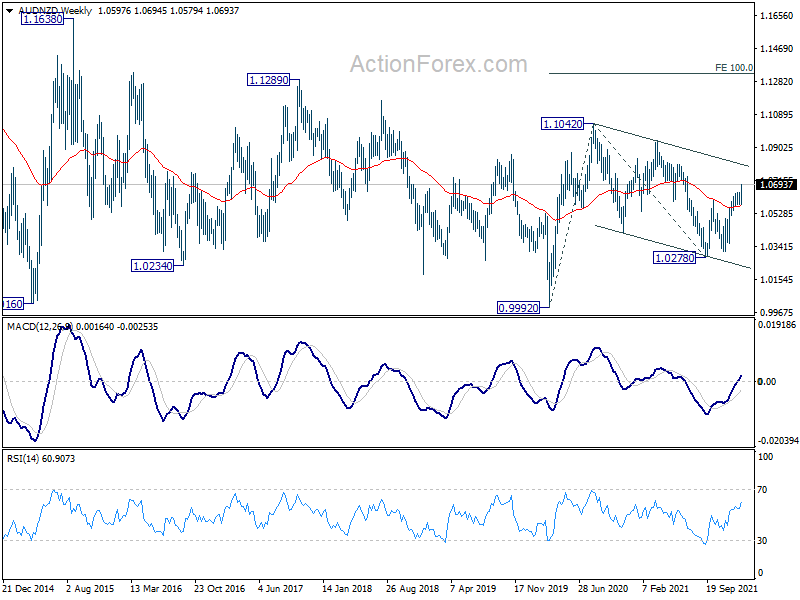

SNB Jordan: Swiss Franc no longer highly valued

SNB Chairman Thomas Jordan said in the post-meeting pressing conference, “the new inflation forecast shows that further increases in the policy rate may be necessary in the foreseeable future.”

“In the current environment, price increases were being passed on more quickly, and are also being more readily accepted, than was the case until recently,” he said. “There is the threat of second-round effects becoming entrenched if inflation remains above 2% for a long period.”

Jordan also noted that the Franc’s strength on safe-haven flow helped dampen the impact on higher fuel and food import prices. But that was less the case following recent decline. “Thus the inflation imported from abroad has increased,” he said. “Another consequence of this depreciation coupled with significantly higher inflation abroad is that the franc is no longer highly valued.”