At a European Parliament committee hearing, ECB President Christine Lagarde said that “the legacy of the financial crisis have driven interest rates down”. Such “low interest rate and low inflation environment has significantly reduced the scope for the ECB and other central banks worldwide to ease monetary policy in the face of an economic downturn”. There were also structural challenges like “environmental sustainability, rapid digitalisation, globalisation and evolving financial structures”. Hence, it’s the “appropriate time” to conduct the policy strategy review.

On the economy , she said there are “tentative signs of stabilisation” in the global economy but uncertainty surrounding the impact of the coronavirus is a “renewed source of concern”. Overall moderate growth performance is “pass-through from wage increases to prices” and inflation remain subdued. Hence, the Eurozone economy “continues to require support from our monetary policy, which provides a shield from global headwinds.”

ECB Monthly Bulletin basically echoes Lagarde’s comments. It noted that Eurozone expansion will continue to be supported by “favourable financing conditions”. Risks remain “titled to the downside” in Eurozone due to ” geopolitical factors, rising protectionism and vulnerabilities in emerging market economies”. But the risks have “become what less pronounced”.

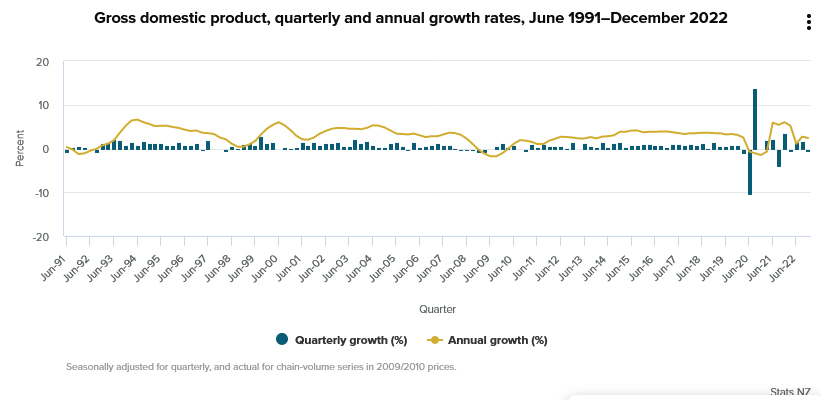

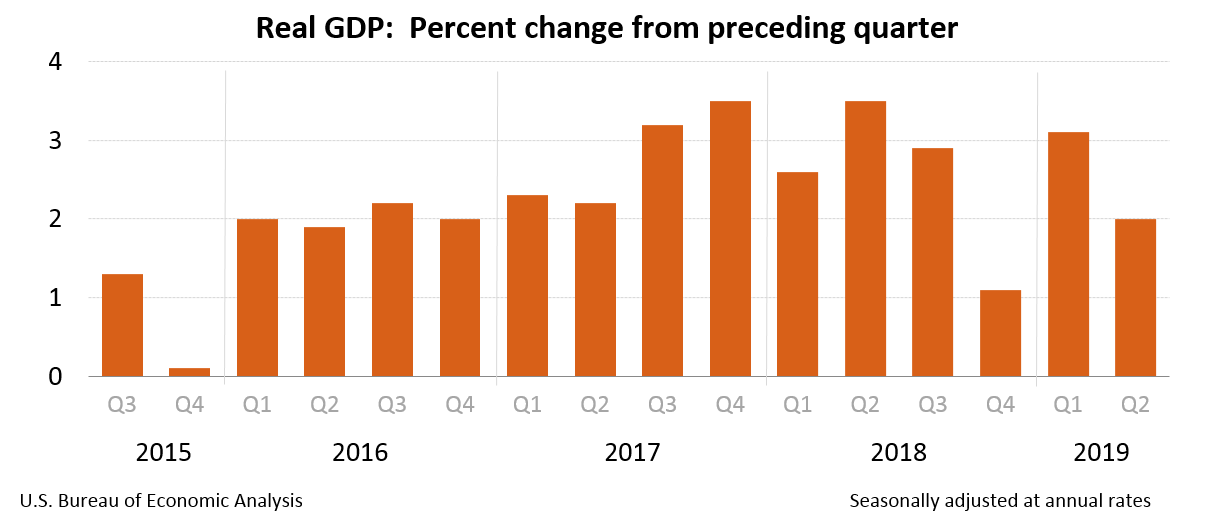

UK GDP grows 0.2% mom in Jan, matches expectations

UK GDP expanded by 0.2% mom in January, matched expectations. Services was up 0.2% mom, and was the largest contributor to growth. Production fell -0.2% mom while construction grew 1.1% mom.

In the three months to January, GDP has fallen by -0.1% 3mo3m. Services was flat. Production fell -0.2% 3mo3m. Construction fell -0.9% 3mo3m.

Full UK GDP release here.