{kind=link}

Dollar Index started the new year with a pronounced surge. Sterling, Euro, and Swiss Franc bore the brunt of this strength, reflecting the sluggish economic outlook in Europe and ongoing concerns about the impact of new US tariffs. Despite these gains, Dollar’s performance against other currencies, including Yen and commodity-linked peers, was more muted. Consolidations in US Treasury yields and resilient risk sentiment somewhat limited the greenback’s upside momentum.

Behind Dollar’s firmness is an evolving interest rate narrative in the US. Recent economic data has reinforced the idea that Fed will pursue fewer rate cuts this year, providing a steady backdrop of support. Meanwhile, Europe faces a bleaker economic outlook, with political uncertainties amplifying downside risks. This stark divergence in fundamentals would widen the rate gap between Fed and other European central banks, intensifying headwinds for European majors in general in the coming months.

In a somewhat surprising twist, Yen emerged as the week’s best performer, with its outperformance largely stemmed from heavy selling in other majors. Nevertheless Yen’s medium-term vulnerability remains intact given BoJ’s cautious stance on rate hikes. Against Dollar, Yen may face renewed pressure again soon as US yields resume their climb.

Commodity currencies— Aussie, Kiwi, and Loonie—also saw some respite, though much of their strength was a correction from steep losses in December rather than a shift in fundamentals. Notably, Australian and New Zealand Dollars may face renewed pressure if weakness in Chinese markets deepens, especially since China’s bumpy start to the year has already dented investor confidence.

Dollar Kicks Off 2025 with a Boost from Hawkish Fed Expectations

Dollar Index began 2025 on a firm footing, posting notable gains as investors price in a gentler path of Federal Reserve easing this year. Recent data highlighting US economic resilience and persistent, though moderated, inflation risks have reinforced the view that Fed may opt for fewer rate cuts than previously anticipated.

Compounding this sentiment are heightened expectations around the incoming Trump administration’s pro-growth measures—ranging from deregulation and tax reforms to stricter immigration policies and tariffs—which could further lift economic activity and stoke inflationary pressures.

Current fed fund futures indicate almost 90% chance that Fed will keep rates at 4.25–4.50% later this month. More importantly, there is 85% probability of just one additional cut to 4.00–4.25% for the entire year. By contrast, ECB is widely forecast to slash rates by as much as 100 basis points over the same period. This stark divergence in central bank policy has underpinned the Dollar’s appeal among traders.

Technically, Dollar Index’s rally from 100.15 reaccelerated, as seen in D MACD, and hit as high as 109.53. Near term outlook will now remain bullish as long as 107.73 support holds. Next target is 61.8% projection of 100.15 to 108.07 from 105.42 at 110.31.

In the bigger picture, there are various interpretations on the price actions from 114.77 (2022 high). It’s unsure if the corrective pattern from there has completed totally, or there would be one more down leg. But in either case, sustained trading above 61.8% retracement of 114.77 to 99.57 at 108.96 would pave the way to retest 114.77 high later in the year.

Meanwhile, US equities have thus far welcomed the recalibration of Fed expectations. S&P 500 is seen as in consolidations only, and larger up trend remains in force with 5669.67 resistance turned support intact. Another rally through 6099.97 is expected at a later stage after the consolidations complete.

However, should the stock market’s risk-on sentiment comes back, it may limit Dollar Index’s upside momentum, particularly above the immediate 110.31 target noted.

Yen Resilient But Vulnerability Persists

While Yen remained resilient against last week, it clearly lacked momentum for a sustainable rebound. The currency remains at risk of further depreciation, and much will depend on how BoJ proceeds with interest rate hikes and whether US Treasury yields continue their rally.

Although BoJ is expected to persist with gradual rate increases, Governor Kazuo Ueda has consistently expressed caution, highlighting the global economic uncertainties—particularly regarding US policy under the incoming administration. These concerns could lead the central bank to adopt a cautious, wait-and-see approach, making a January rate hike increasingly uncertain.

Moreover, market consensus suggests that the BoJ could raise rates only two to three times this year, potentially reaching 1.00%—a milestone not seen in decades. However, such adjustments may do little to strengthen Yen meaningfully, as they would largely reflect policy normalization rather than outright tightening.

Technically, US 10-year yield’s rally from 3.603 stalled just ahead of 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683. Further rally is expected as long as 4.484 support holds,. Decisive break of 4.683 could prompt upside acceleration to 100% projection 5.028. Nevertheless, break of 4.484 will bring deeper correction to 55 D EMA (now at 4.335), and possibly below before the next rise.

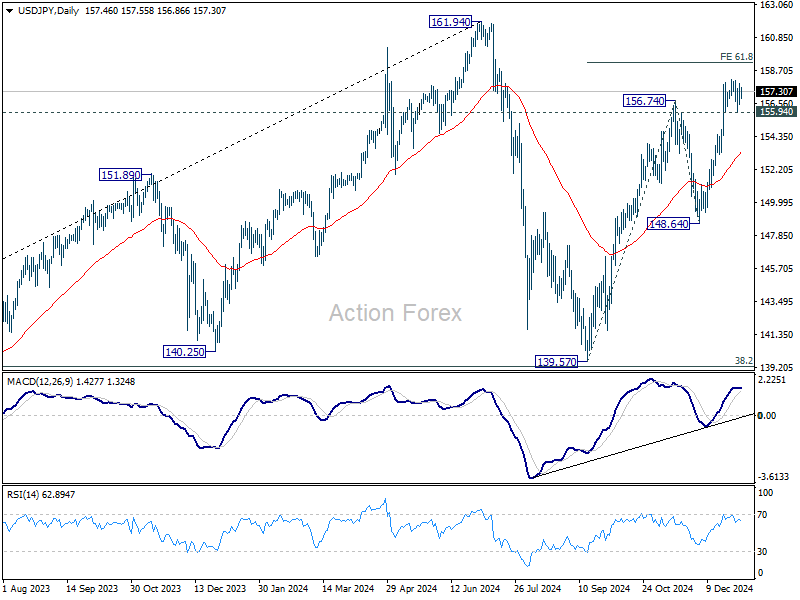

USD/JPY’s outlook is a little bit more complicated. On the one hand, the next move should be tightly correlated with US 10-year yield. Rise from 139.57 should extend to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25, in particular when 10-year yield resumes the rally towards 4.683. However, Japan’s stance on intervention would then be the determining factor on whether USD/JPY could power up further through 161.94 high.

Commodity Currencies Fragile as Chinese Markets Falter, Yuan Pressured

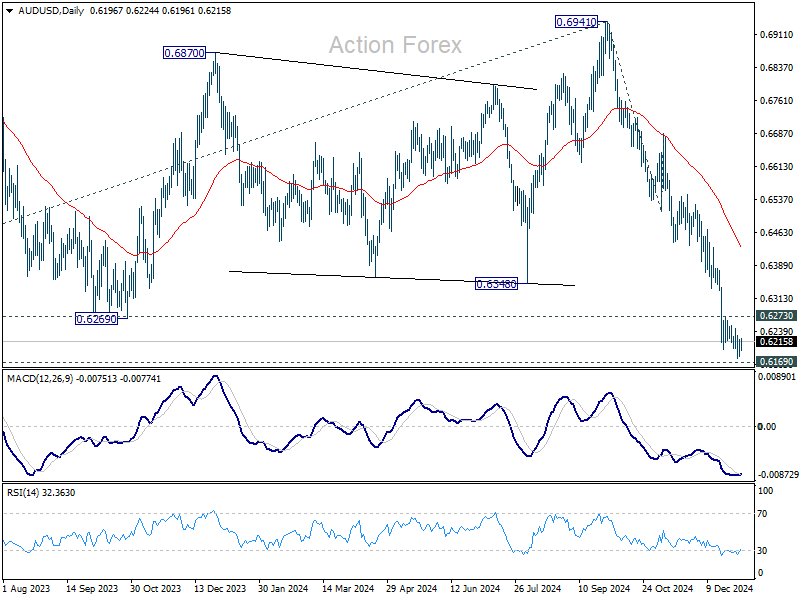

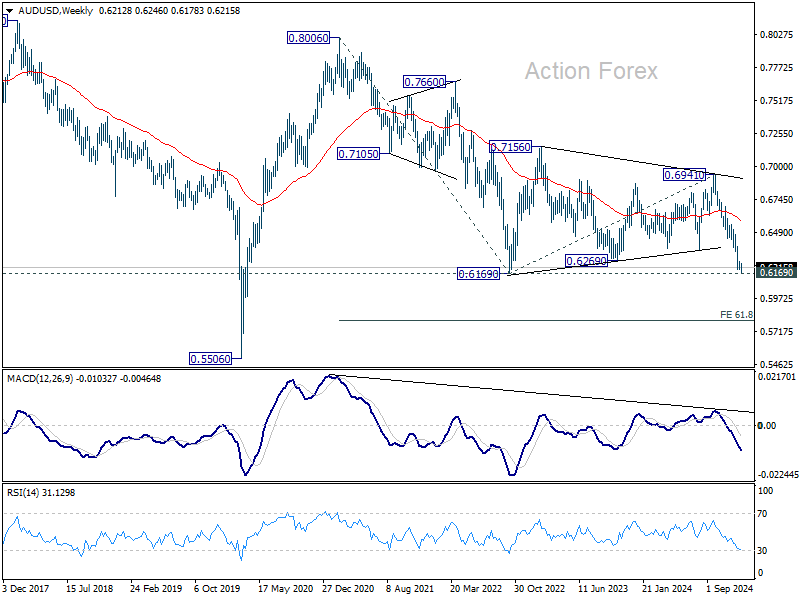

Commodity currencies have shown resilience last week, largely shielded by heavy selling in European majors. However, their vulnerability remains high as 2025 unfolds, especially for Australian and New Zealand Dollars.

The crux of the concern lies in China’s weak market performance at the start of the year. Chinese equities kicked off 2025 with their worst annual opening in nearly a decade, reflecting fragile investor sentiment despite the first full-year stock market gain since 2020.

This cautious mood seems contradictory in light of Beijing’s December policy meetings, which signaled clearer stimulus intentions. Yet many market participants worry about the speed and efficacy of any measures, particularly as meaningful policy action may not materialize until the “Two Sessions” legislative gathering in March.

In addition, domestic deflationary pressures persist, and the threat of renewed US tariffs looms, adding to the downside risks for China’s economy and the commodity currencies that depend on its growth.

Technically, the “free fall” in the Shanghai SSE composite looks rather concerning. Risk will now stay heavily on the downside as long as 55 D EMA (now at 3306.79) holds. Focus is on key support level between 3152.82 and 3174.26. Decisive break there could prompt downside acceleration to 100% projection of 3674.40 to 3152.82 from 3494.86 at 2973.28.

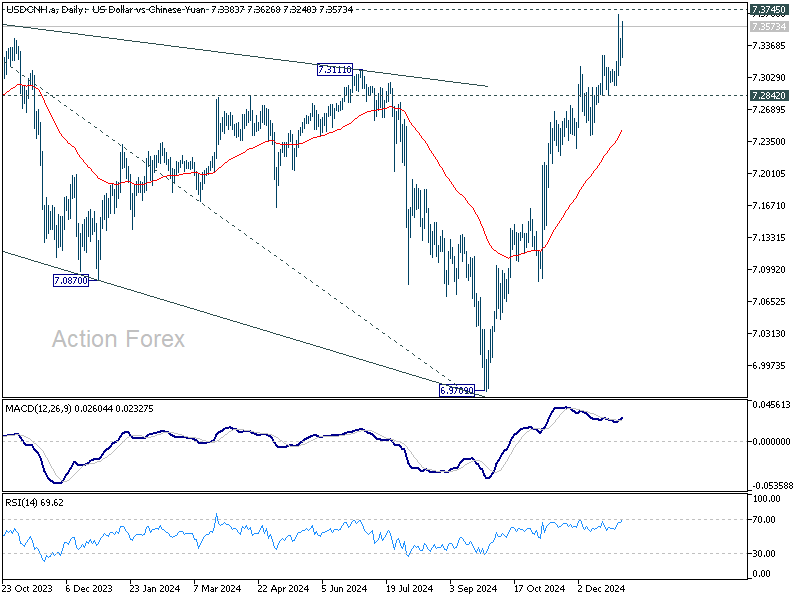

Adding to the concerns, the Chinese Yuan (offshore) is on the verge of breaking through record high with the strong decline in Yuan at the start of the year. While the depreciation of Yuan might be endorsed by the government as counter measures to trade war 2.0 with the US, investor reactions would be uncertain.

Technically, further rally is expected in USD/CNH as long as 7.2842 support holds. Decisive break of 7.3745 will resume the up trend from 6.3057. Next medium term target will be 100% projection of 6.6971 to 7.3679 from 6.9709 at 7.6411.

AUD/USD’s decline slowed ahead of 0.6169 key support (2022 low). But near term risk will stay on the downside 0.6273 resistance holds. Decisive break of 0.6169 will confirm resumption of whole down trend from 0.8006 (2021 high). Next medium term target would be 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. Break of 0.6273 will bring near term corrective rebound first.

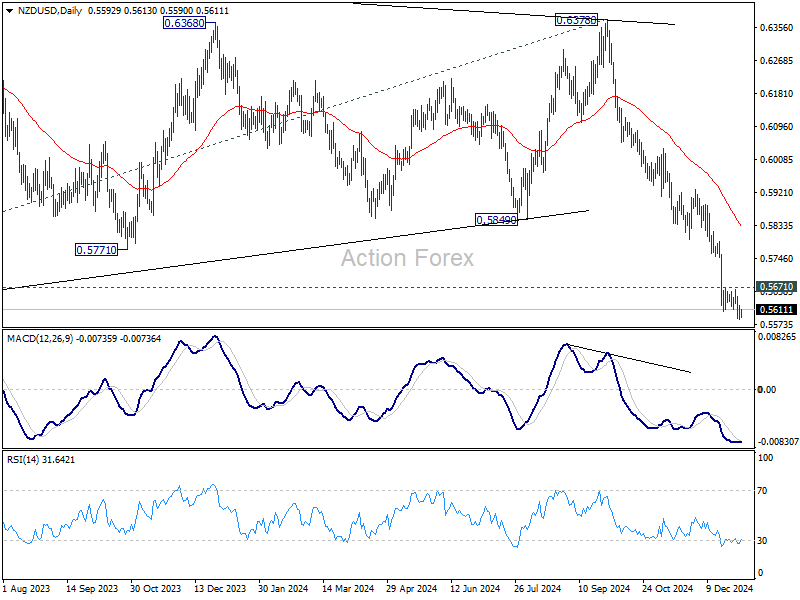

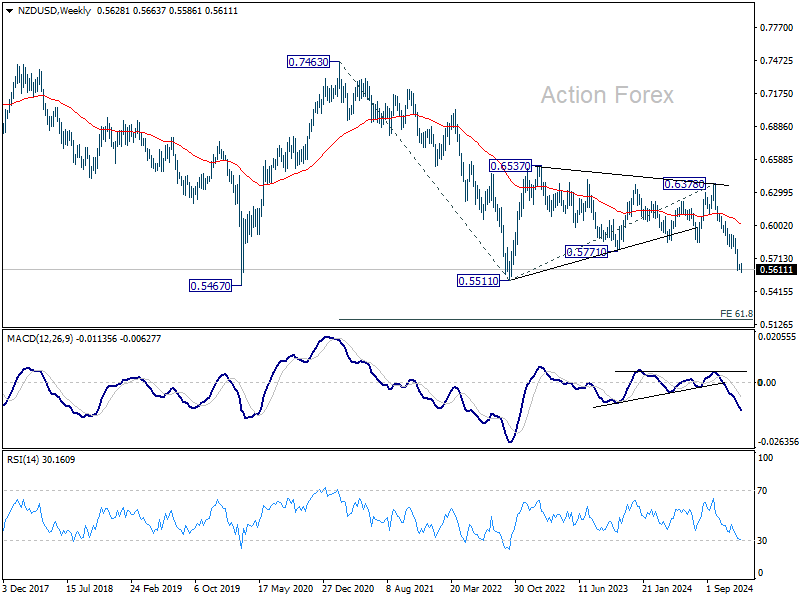

As for NZD/USD, near term risks will stay on the downside as long as 0.5671 resistance holds. Firm break of 0.5511 (2022 low) would pave the way to 61.8% projection of 0.7463 to 0.5511 from 0.6378 at 0.5172. Meanwhile, break of 0.5671 will bring near term corrective rebound first.

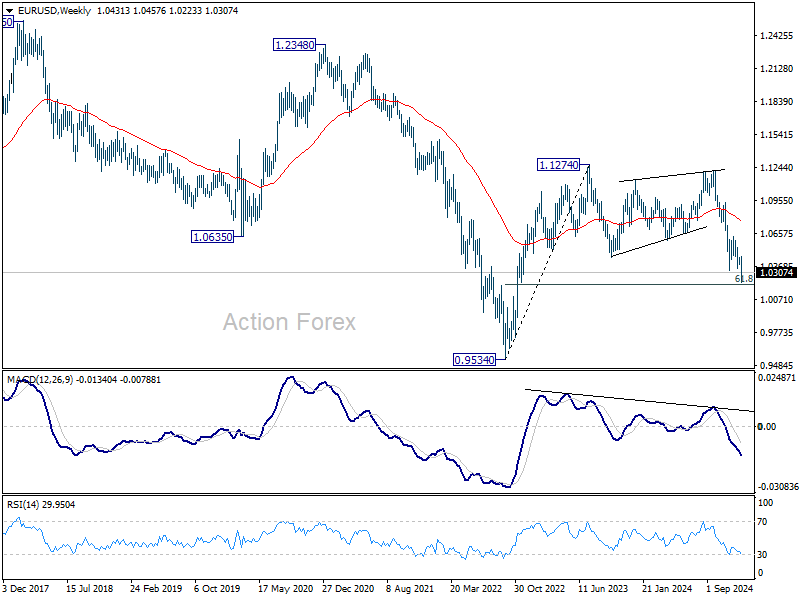

EUR/USD Weekly Outlook

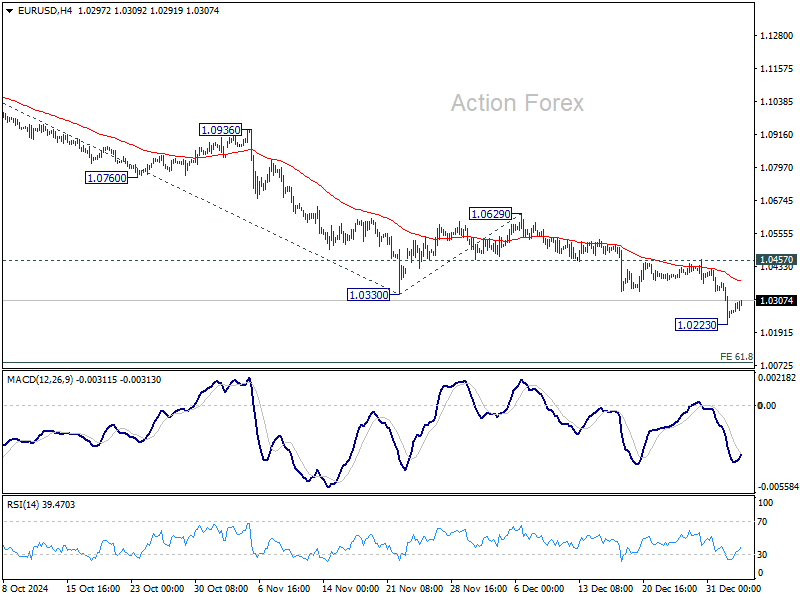

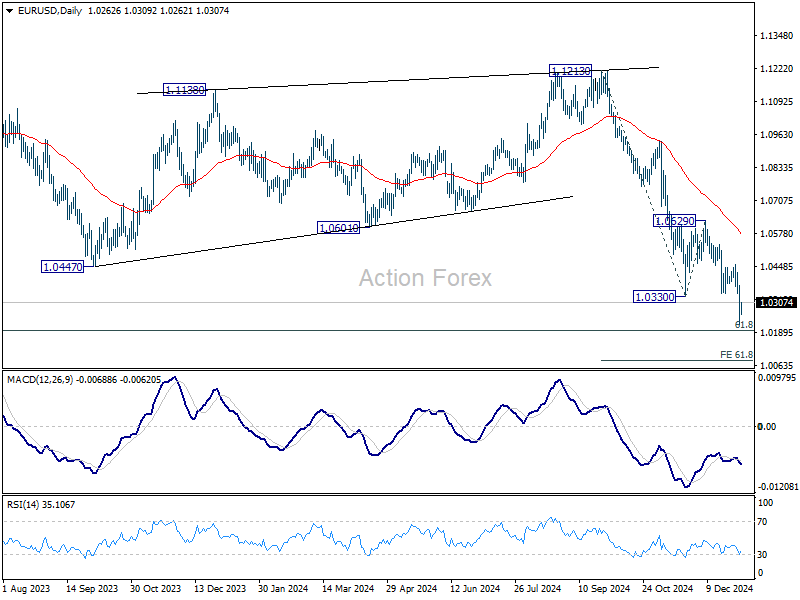

EUR/USD’s decline from 1.1213 resumed by breaking through 1.0330 support last week. A temporary low might be formed at 1.0223 and initial bias is turned neutral this week first. But further decline is expected as long as 1.0457 resistance holds. On the downside, break of 1.0223 will target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0973). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, downside breakout would be mildly in favor.