{kind=link}

Yen continues to be the weakest one today as selloff intensifies in European session. Relieves from immediate risks are still as the major reason driving the Japanese currency down. Australian Dollar continues to be the strongest one with AUD/USD and EUR/AUD taking out key near term levels. Dollar was under some pressure earlier today but is supported by Fed Rosengren’s comments and turned mix entering into US session.

Boston Fed Rosengren: Somewhat more tightening may end up being needed

Boston Fed President Eric Rosengren sounded hawkish in his comments today. Referring to Fed’s projection of two more hikes this year, Rosengren said that “somewhat more tightening may end up being needed”. He expected a “somewhat stronger” economy ahead than the already “quite positive” FOMC projections. He also pointed to solid performance in job creation, falling unemployment and inflation close to Fed’s 2% target. However, Rosengren also pointed out short-run and long-run risks to the positive outlook. Short run risks include trade tensions and overheated “boom-bust” scenario. Long run risks included insufficient fiscal and monetary buffers.

TPP member Japan, Australia, Malaysia told Trump, you’re welcomed but no renegotiation

Ministers of three of TPP-11 members responded to news that Trump is considering to rejoin TPP. While all of the welcomed the news, they also said there will be no renegotiation on what were signed. Australia Trade Minister Steven Ciobo said today that “we welcome the U.S. coming back to the table but I don’t see any wholesale appetite for any material re-negotiation of the TPP-11.”Japan Minister Toshimitsu Motegi said the current deal is a “balanced one, like fine glassware” and it would be difficult to change. Malaysia International Trade and Industry Minister Mustapa Mohamed also warned that renegotiation would “alter the balance of benefits for parties.” These were in response to Trump’s tweet that “would only join TPP if the deal were substantially better than the deal offered to Pres. Obama.”

S&P upgrades Japan’s A+ rating outlook to “positive”

S&P Global Ratings upgraded Japan’s A+ outlook from “stable” to “positive”. S&P noted stronger economy should set the stage for fiscal improvement in Japan. The positive outlook reflects healthier growth prospect, in both real and nominal terms. The current rating also reflect Japan’s formidable external position, diversified economy, political stability and financial system stability. Nonetheless, it also pointed out that While Japan’s external balance sheet is strong, Government finances are weak. And that is a significant constraint of its creditworthiness.

China reported rare trade deficit in March, Q1 imports from EU surged

China reported a rate trade deficit of USD -5b in March versus expectation of USD 27.8b surplus. That’s also the first monthly trade deficit since last February. Imports rose 5.9% yoy while exports dropped -2.7% yoy. Trade surplus with US dropped to USD 15.3b. In CNY terms trade balance came in at CNY -30b deficit versus expectation of CNY 160b surplus. Imports dropped -9.8% yoy while exports also dropped -9.8% yoy.

For the quarter from January to March, 2018, China’s trade surplus came in at USD 49.1b, dropped -23.2% yoy from Q1 of 2017. Exports rose 14.1% yoy. But import grew even stronger by 18.9% yoy. In CNY terms, Q1 trade surplus rose came in at CNY 326.2b with exports increased by 7.4% yoy and imports jumped even stronger by 11.7% yoy.

Also for Q1, export to US rose 14.8% yoy to USD 99.9b while imports from US rose 8.9% yoy to USD 41.7b. Exports to EU rose 13.2% yoy to USD 90.2b while imports from EU rose 17.5% yoy to USD 63.5b.

New Zealand manufacturing PMI signed slower expansion

New Zealand BusinessNZ Performance of Manufacturing Index (PMI) dropped -1.1 to 52.2 in March. That’s also the second consecutive decline in 2018 even though it still signaled expansion. Nonetheless, BusinessNZ’s executive director for manufacturing Catherine Beard noted a positive point that the proportion of positive comments in March (55.1%) picked up from both February (51.4%) and January (50.7%). BNZ Senior Economist, Craig Ebert said that the weak spot in March’s PMI was its production index.

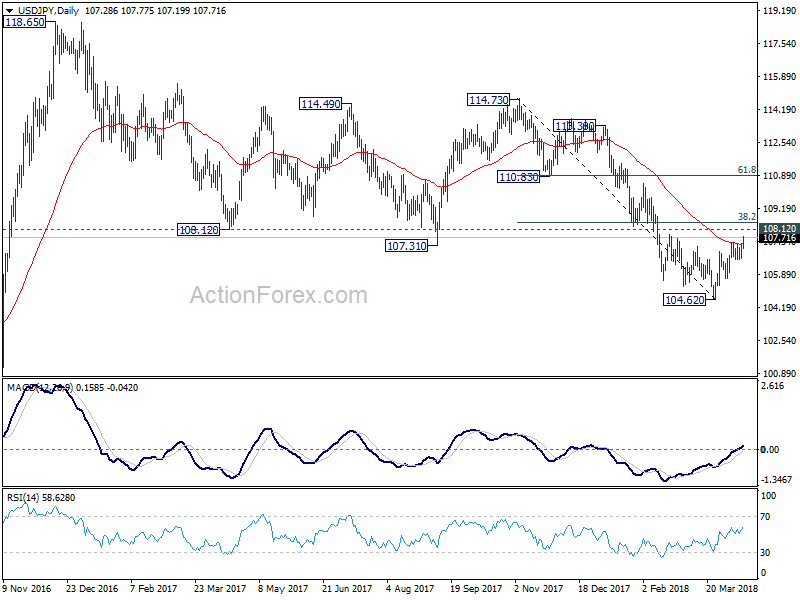

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.88; (P) 107.15; (R1) 107.61; More…

USD/JPY’s rally extends to as high as 107.77 so far. Intraday bias remains on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64 minor support is needed to indicate completion of the rebound. Otherwise, further rise will remain in favor even in case of retreat.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | RBA Financial Stability Review | ||||

| 3:10 | CNY | Trade Balance (USD) Mar | -5.0B | 27.8B | 33.7B | |

| 3:10 | CNY | Trade Balance (CNY) Mar | -30B | 160B | 225B | |

| 6:00 | EUR | German CPI M/M Mar F | 0.40% | 0.40% | 0.40% | |

| 6:00 | EUR | German CPI Y/Y Mar F | 1.60% | 1.60% | 1.60% | |

| 9:00 | EUR | Eurozone Trade Balance (EUR) Feb | 21.0B | 20.1B | 19.9B | 20.2B |

| 14:00 | USD | U. of Mich. Sentiment Apr P | 100.6 | 101.4 |