{kind=link}

Australian Dollar and New Zealand Dollar jump broadly as another week starts in full risk-on mode. Japanese Nikkei opened sharply higher and is trading up 1.4% at the time of writing. Hong Kong HSI is also up close to 1.5%. That followed the strong 1.77% rise in DOW on Friday on the job report that’s “perfect for stocks”. Aussie is additional supported as the country is exempted from US President Donald Turmp’s steel and aluminum tariff. Meanwhile, sentiments are not so positive for the greenback as it’s under broad based selling pressure. The markets might be a bit quiet today but a key focus will remain on 1.2268 minor support support in EUR/USD, which will determine the next near term move.

EU sought clarity on steel tariffs, but Trump warned “we TAX CARS”

European Commissioner for Trade Cecilia Malmström met U.S. Trade Representative Robert Lighthizer over the weekend to seek clarity on the steel and aluminum tariffs of the US. However, Malmström expressed her frustrations afterwards complaining that the meeting delivered “no immediate clarity”. She tweeted “As a close security and trade partner of the U.S., the EU must be excluded from the announced measures. No immediate clarity on the exact U.S. procedure for exemption however, so discussions will continue next week.”

German Economy Minister Brigitte Zypries also warned that “Trump’s policies are putting the order of a free global economy at risk.” And, “he does not want to understand its architecture, which is based on a rule-based system of open markets. Anyone, who is questioning this, is jeopardizing prosperity, growth and employment.”

However, Trump stepped up his rhetoric again as he tweeted “the European Union, wonderful countries who treat the U.S. very badly on trade, are complaining about the tariffs on Steel & Aluminum.” He added “if they drop their horrific barriers and tariffs on U.S. products going in, we will likewise drop ours. Big Deficit. If not, we Tax Cars etc. FAIR!”

AU PM Turnbull: We’re exempted, why complain?

Following Canada and Mexico, Australia was exempted from the steel tariff of the US. Prime Minister Malcolm Turnbull said there were no strings attached to the exemption. He said that “I know exactly what was discussed and there is no, sort of, request for any change or addition to our security arrangements.” He also said that Australia is not going to initiate any complain to the WTO regarding the tariffs. He added that “obviously as a country that will be exempt from those tariffs, we don’t have a basis to bring a complaint,” he said. Trump tweeted over the weekend that Turnbull is “committed to having a very fair and reciprocal military and trade relationship. Working very quickly on a security agreement so we don’t have to impose steel or aluminum tariffs on our ally, the great nation of Australia!

North Korea quiet on meeting with US

North Korea leader Kim Jong-un is set to meet with Trump by the end on May on the topic of denuclearization. It’s reported that Kim would want to have a peace treaty with the US. But other than that, the country is so far very quiet on the topic. South Korea’s Ministry of Unification spokesman Baik Tae-hyun said today that “we have not seen nor received an official response from the North Korean regime regarding the North Korea-U.S. summit.” And, “I feel they’re approaching this matter with caution and they need time to organize their stance.”

Japan BSI sentiments dropped broadly

Japan business sentiments weakened generally in Q1. Large all industry index dropped to 3.3, down from 6.2. Large manufacturing index dropped to 2.9, down from 9.7. Large non-manufacturing index dropped to 3.4, down from 4.5. Outlook for Q2 showed further deterioration. But large companies are expectation a rebound in Q3. Deteriorations are also seen in sentiments of small and mid sized companies for Q1.

The week ahead

The economic calendar is not particularly busy this week. Major focuses will firstly be on CPI and retail sales from US. SNB quarterly rate decision will also be featured but unlikely to be inspirational. BoJ will also release meeting minutes. Other than that, some China growth data and New Zealand GDP will also be watched. Here are some highlights:

- Tuesday: Australia NAB business confidence, home loans; Japan tertiary industry index; UK annual budget release; US CPI

- Wednesday: New Zealand current account; BoJ minutes; China industrial production, fixed asset investment, retail sales; Eurozone employment change, industrial production; US retail sales, PPI, business inventories

- Thursday: New Zealand GDP; SNB rate decision; US Empire state manufacturing index, Philly Fed survey, import prices, jobless claims, NAHB housing markets index

- Friday: New Zealand BusinessNZ manufacturing index; Eurozone CPI final; Canada manufacturing sales; US housing starts and building permits, industrial production, U of Michigan sentiments.

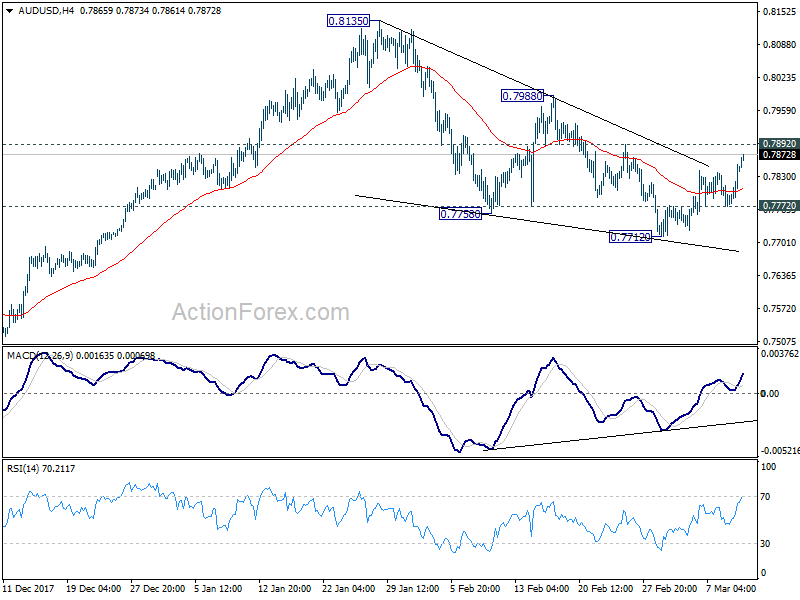

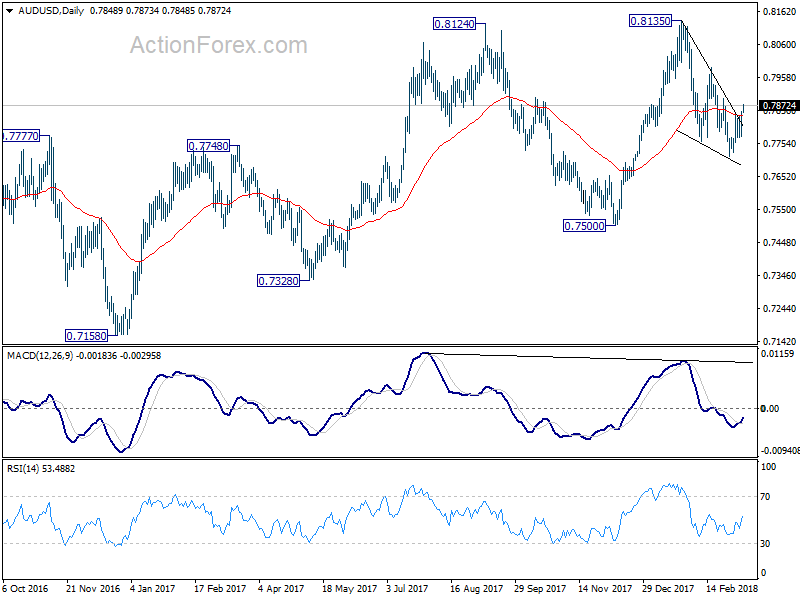

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7797; (P) 0.7825; (R1) 0.7874; More…

AUD/USD’s rebound from 0.7712 extends to as high as 0.7866 so far today. As noted before, the break of f near term trend line resistance is taken as first sign of reversal. Intraday bias remains on the upside for 0.7892 minor resistance first. Break will affirm this bullish case and target 0.7988 and above. On the downside, below 0.7772 will turn bias to the downside for 0.7712. Break there will resume whole fall from 0.8135.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q1 | 2.9 | 10.3 | 9.7 | |

| 6:00 | JPY | Machine Tool Orders Y/Y Feb P | 48.80% | |||

| 18:00 | USD | Federal Budget Balance Feb | -222.3B | 49.2B |