{kind=link}

Dollar’s recovery continues in early US session and is gathering some extra momentum against Sterling and Euro. But still, there is no clear indication of near term trend reversal yet. Meanwhile, Sterling is under broad based selling pressure. Profit taking after recent strong rally is one of the reasons. Additionally, the pound is weighed down by re-emerging political uncertainties in the UK. Elsewhere in the FX markets, Euro is following as the second weakest one. Kiwi and Aussie are also soft.

Release from US today, personal income rose 0.4% in December versus expectation of 0.3%. Personal spending rose 0.4%, in line with consensus. Headline PCE slowed to 1.7% yoy. Core CPI was unchanged at 1.5% yoy. Released earlier, German import price index rose 0.3% mom in December.

Sterling broadly lower on political uncertainties

Sterling tumbles broadly today on re-emergence of political uncertainties. It’s reported that Prime Minister Theresa May could face another leadership challenge after the House of Lords Constitution Committee criticize3d that May’s Brexit legislation had "fundamental flaws". The committee chairwoman Baroness Taylor said that "we acknowledge the scale, challenge and unprecedented nature of the task of converting existing EU law into UK law, but as it stands this bill is constitutionally unacceptable." And, there is additional complexity because "in many areas the final shape of that law will depend on the outcome of the UK’s negotiations with the EU". The committee added that the method proposed to create a new category of "retained EU law" will cause "problematic uncertainties and ambiguities."

Additionally, regarding the transition deal is set to insist that UK must apply EU laws as if it were a member state during the transition period. And such compliance is expected to be unconditional. On the other hand, the UK is clearly uncomfortable with the demand. Brexit secretary David Davis hinted that he would demand the power to object. As Davis said, "means to remedy issues" are needed if laws were "deemed to run contrary to our interests". But some EU officials see the UK’s position on it being counter productive, in particular as Prime Minister Theresa May is targeting to complete a transition deal in March, as businesses requested.

ECB Praet: Some distance from meeting ending QE

ECB chief economist Peter Praet sounded cautious as he pushed back the idea of ending the asset purchase program. He said that ECB is still "some distance" away from meeting the three measurements on the the program. And the three criteria are:

- Firstly, "headline inflation will have to be on course to reach levels below, but close to, 2 percent by the end point of a meaningful medium-term horizon."

- Secondly, "the Governing Council wants to be sure that the expectation of an upward adjustment in inflation has a sufficiently high probability of being realized and is being met on a sustainable basis."

- Thirdly, "if the inflation outlook is overly dependent on monetary support, the upward adjustment cannot be considered sustained. So we want to verify that the path would be maintained even in less supportive monetary policy conditions."

Praet emphasized that "the transition toward a normalization will begin once we have established that there is a sustained adjustment in the path of inflation." However, "despite the strong cyclical momentum, domestic price pressures remain subdued, as do measures of underlying inflation."

ECB Governing Council member Klass Knot delivered some hawkish comments over the weekend. He said "there is no reason whatsoever to continue" the EUR 30b a month asset purchase program after it ends in September. He added "we don’t have to communicate yet that it will be over after September, but I think that’s where we’re headed." Meanwhile, interest rates would stay low in the coming years. Knot noted that "Interest is mainly low because there are more people that want to save, than that want to invest. This will change as the economy grows, but that will take time."

FOMC to highlight a busy week

The highlight of the coming week is the FOMC meeting. This is also the last time for outgoing Fed Chair Janet Yellen to preside the meeting. While it has been widely expected that no change would be made in the monetary policy, the market focus is on the Fed’s economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed’s long-term target, should have anchored the Fed’s confidence over the economic outlook. We do expect the Fed to address the issue recent USD weakness. On the monetary policy outlook, the market continued to price in over 70% of a rate hike in March.

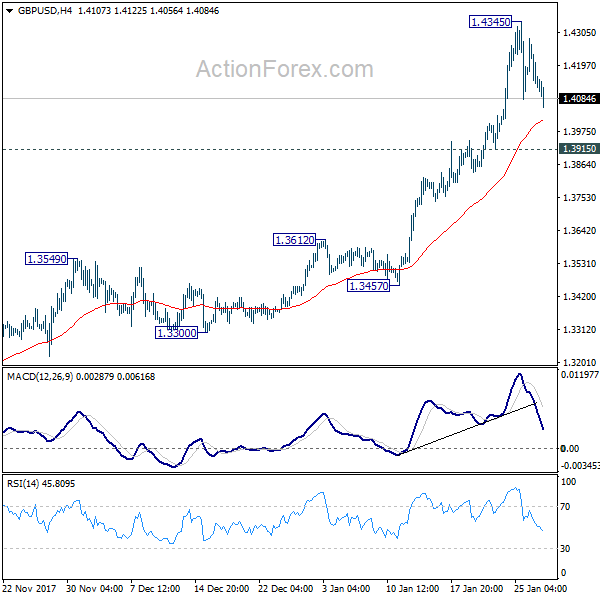

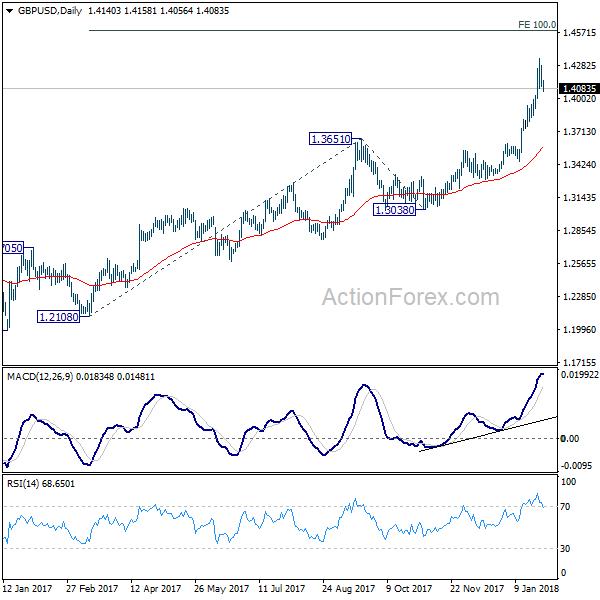

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4180; (R1) 1.4256; More…..

GBP/USD’s retreat from 1.4345 extends lower today but outlook remains unchanged. Intraday bias stays neutral and further rise is still expected with 1.3915 support intact. On the upside, break of 1.435 will extend the up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German Import Price Index M/M Dec | 0.30% | 0.20% | 0.80% | |

| 13:30 | USD | Personal Income Dec | 0.40% | 0.30% | 0.30% | |

| 13:30 | USD | Personal Spending Dec | 0.40% | 0.40% | 0.60% | 0.80% |

| 13:30 | USD | PCE Deflator Y/Y Dec | 1.70% | 1.70% | 1.80% | |

| 13:30 | USD | PCE Core M/M Dec | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | PCE Core Y/Y Dec | 1.50% | 1.50% | 1.50% |