{kind=link}

Sterling reversed earlier gains and weakened broadly overnight after the meeting between UK Prime Minister Theresa May and European Commission President Jean Claude Juncker failed deliver agreements on Brexit. Dollar also softened mildly as boost from tax bill faded. Traders are also cautious as there are still much work to be done to reconcile the House and Senate tax bills. And there are still lots of uncertainties on what the final versions would be. Investors in other markets were also cautious. DOW jumped to record high at 24534.04, but pared back much gain to close at 24290.05, up only 0.24%. S&P 500 rose to record high at 2665.19 too, but closed down -0.11% at 2639.44. Asian markets also trade with an undertone today with Nikkei losing -0.15% at the time of writing.

No deal was made yet on Brexit negotiations

Sterling reversed earlier gains on disappointment that no deal was made between UK and EU on Brexit negotiations. It’s reported that UK Prime Minister Theresa May was forced to pause the lunch meeting with European Commission President Jean Claude Juncker to answer a call from furious DUP leader Arlene Foster. May’s proposal regarding Irish border is believed to have a compromise to allow Norther Ireland to retain the same rules as the Republic of Ireland critical areas. The North Ireland party was deeply worried that the deal would result in "regulatory divergence" between North Ireland and the rest of UK.

May insisted after the the meeting the progress has been made even through "a couple of issues some differences do remain which require further negotiation and consultation". And she sounded optimistic saying "We will reconvene before the end of the week and I am also confident that we will conclude this positively."

European Commission President Jean Claude Juncker said, after meeting with UK Prime Minister May, "it was not possible to reach complete agreement today" despite their "best efforts". Nonetheless, he added that "we were narrowing our positions to a huge extent". And, "I’m still confident that we can reach sufficient progress before the European Council of 15 December." Juncker emphasized that "this is not a failure, this is the start of the very last round", and, "I’m very confident that we will reach an agreement in the course of this week."

Aussie lifted by retail sales, hold gains after RBA stands pat

Australian Dollar was lifted by solid retail sales data today. Sales grew 0.5% mom in October, beating expectation of 0.3% mom. RBA left cash rate unchanged at 1.50% as widely expected. The accompanying statement revealed nothing new and Aussie maintains gain after that. In short, RBA maintained that " holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time." The central bank also maintained that GDP growth would average 3% over the new few years. Employment growth is expected continue to solid but wage growth "remains low". Inflation also remains "low" but RBA expects it to "pick up gradually as the economy strengthens. It also retained the warning that "an appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast." Also from Australia, current account deficit narrowed slightly to AUD -9.1b in Q3.

Elsewhere

China Caixin PMI services rose to 51.9 in November, up from 51.2, above expectation of 51.5. UK BRC sales monitor rose 0.6% yoy in November. Eurozone will release Q3 GDP revision, retail sales and services PMI revision today. UK will also release PMI services. Later in the day, Canada will release trade balance. US will release trade balance and ISM non-manufacturing.

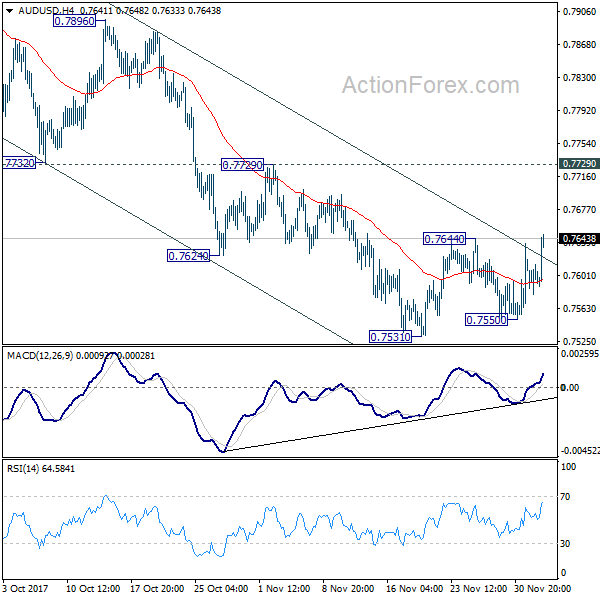

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7580; (P) 0.7597; (R1) 0.7615; More…

AUD/USD recovers today as consolidation from 0.7531 extends. Overall outlook remains unchanged though. As long as 0.7729 resistance holds, near term outlook remains bearish and further decline is expected. Break of 0.7550 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8. Nonetheless, break of 0.7729 will indicate near term reversal, with bearish divergence condition in 4 hour MACD. And stronger rebound would be seen back to 0.7896 resistance and above.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8033). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | 0.60% | -1.00% | ||

| 0:30 | AUD | Current Account Balance (AUD) Q3 | -9.1B | -8.8B | -9.6B | -9.7B |

| 0:30 | AUD | Retail Sales M/M Oct | 0.50% | 0.30% | 0.00% | 0.10% |

| 1:45 | CNY | Caixin PMI Services Nov | 51.9 | 51.5 | 51.2 | |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:45 | EUR | Italy Services PMI Nov | 53.2 | 52.1 | ||

| 8:50 | EUR | France Services PMI Nov F | 60.2 | 60.2 | ||

| 8:55 | EUR | Germany Services PMI Nov F | 54.9 | 54.9 | ||

| 9:00 | EUR | Eurozone Services PMI Nov F | 56.2 | 56.2 | ||

| 9:30 | GBP | Services PMI Nov | 55 | 55.6 | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | 0.60% | 0.60% | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | -0.70% | 0.70% | ||

| 13:30 | CAD | International Merchandise Trade (CAD) Oct | -2.3B | -3.2B | ||

| 13:30 | USD | Trade Balance Oct | -46.2B | -43.5B | ||

| 14:45 | USD | Services PMI Nov F | 55.3 | 54.7 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Nov | 59 | 60.1 |