{kind=link}

Global financial markets are relatively stable heading into the end of the week, with risk appetite showing further signs of improvement. European equities are trading modestly higher, following rebounds seen earlier in Japan and Hong Kong. However, US futures are slightly in the red despite strong earnings reports from tech heavyweights Alphabet and Intel. Still, one supportive development is the continued pullback in US Treasury yields, with the 10-year dipping below 4.3% mark—viewed as a positive sign for US assets.

Meanwhile, the trade war front is seeing renewed speculation, especially regarding US-China tariff relations. According to multiple media reports, China has quietly granted tariff exemptions on some US goods—including integrated circuits—previously subject to its 125% retaliatory duties. While no formal statement has been issued by Chinese authorities, there are reports of internal government consultations with foreign businesses. A list of 131 product categories is circulating on social media is believed to outline those under consideration for exemption. These steps signal a possible softening of Beijing’s stance and a willingness to preserve critical supply chains.

Meanwhile, US President Donald Trump told Time magazine that China is actively engaging in talks with Washington to strike a tariff deal, and claimed that President Xi Jinping had recently called him. However, China’s Foreign Ministry declined to comment on Trump’s statement and previously warned the US to stop “misleading the public” about the status of bilateral negotiations. The conflicting narratives underscore the fog of uncertainty surrounding trade diplomacy, though market participants appear cautiously hopeful that both sides are seeking a path to de-escalation.

In the currency markets, the week’s performance leaderboard remains largely unchanged. Kiwi is holding firmly at the top. Sterling and Aussie are also among the week’s better performers. On the other end of the spectrum, Swiss franc, Japanese Yen, and Euro are lagging—reflecting fading safe-haven demand. Dollar and Loonie sit in the middle.

In Europe, at the time of writing, FTSE is up 0.28%. DAX is up 0.87%. CAC is up 0.65%. UK 10-year yield is down -0.021 at 4.482. Germany 10-year yield is up 0.018 at 2.471. Earlier in Asia, Nikkei rose 1.90%. Hong Kong HSI rose 0.32%. China Shanghai SSE fell -0.07%. Singapore Strait Times fell -0.21%. Japan 10-year JGB yield rose 0.03 to 1.34.

Canada retail sales fall -0.4% mom in Feb, but core spending offers rebound hopes

Canadian retail sales declined by -0.4% mom to CAD 69.3B in February, in line with market expectations. The overall weakness was driven primarily by a -2.6%mom drop in motor vehicle and parts dealers, with all four store categories in the subsector posting declines.

However, beneath the surface, the data showed encouraging signs. Core retail sales—which exclude fuel and vehicle-related sales—rose by 0.5% mom.

Looking ahead, Statistics Canada’s advance estimate points to a 0.7% mom increase in total sales for March.

SNB’s Schlegel: Growth may miss forecasts due to trade uncertainty

Swiss National Bank Chairman Martin Schlegel warned at the central bank’s annual general meeting that high levels of trade policy uncertainty continue to cloud the economic outlook.

“It remains very uncertain how inflation and the economy in Switzerland will develop,” Schlegel said, adding that “an economic slowdown cannot be ruled out.”

Growth forecasts are already under pressure, with SNB’s March projection of 1% to 1.5% GDP growth this year falling below Switzerland’s long-term average of 1.8%.

Schlegel reiterated that SNB stands ready to adjust policy if needed, including interest rate changes and foreign exchange interventions. However, he acknowledged the limits of monetary policy in addressing deeper structural uncertainty.

“Price stability cannot prevent trade policy uncertainty,” he cautioned, but emphasized that maintaining stable prices provides an essential foundation for the broader economy.

UK retail sales rise 0.4% mom in March, 1.6% qoq in Q1

UK retail sales surprised to the upside in March, rising by 0.4% mom, defying market expectations for a -0.3% mom decline.

The unexpected strength was attributed largely to favorable weather conditions, which lifted sales at clothing and outdoor retailers. However, this gain was partially offset by weaker performance at supermarkets.

Looking beyond the monthly figure, the broader quarterly performance painted an encouraging picture of consumer resilience. Retail sales volumes grew by 1.6% qoq 1.7% yoy in Q1. These results indicate that UK consumers remain relatively active despite broader economic uncertainties.

Tokyo CPI core surges to 3.4% in April, strengthening case for BoJ June hike

Inflation in Japan’s capital city surged in April, with Tokyo core CPI (excluding food) accelerating from 2.4% yoy to 3.4% yoy, above the 3.2% yoy forecast. The more domestically focused core-core measure (excluding food and energy) also rose sharply, from 2.2% yoy to 3.1% yoy. Headline CPI jumped from 2.9% yoy to 3.5% yoy.

Despite the upside surprise, BoJ is still expected to hold rates steady at its May 1 policy meeting as it gauges the broader impact of recent US tariffs and awaits progress in ongoing trade negotiations. However, with inflation gathering pace across key categories, market expectations are shifting toward a rate hike as soon as June.

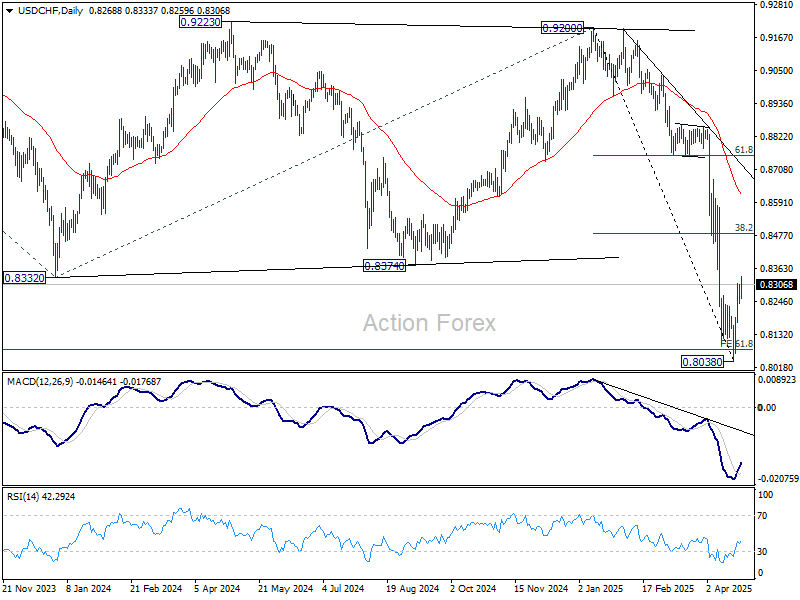

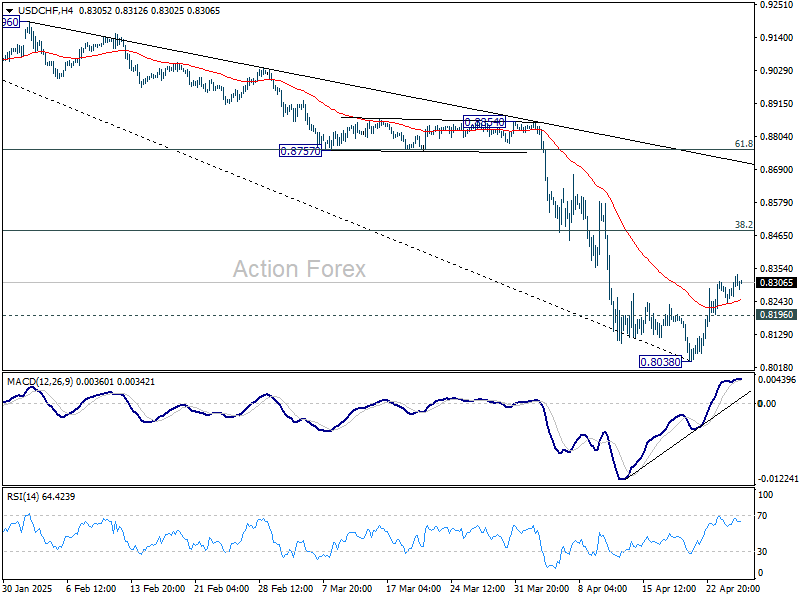

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8237; (P) 0.8273; (R1) 0.8306; More….

USD/CHF’s corrective recovery from 0.8038 is still in progress and intraday bias stays on the upside. Further rise would be seen but upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8794) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.