{kind=link}

Global financial markets are trading with a cautiously positive tone today, with modest gains across Europe and US futures pointing to a higher open. Investor sentiment has improved on the back of US President Donald Trump stepping back from recent aggressive rhetoric—both toward Fed Chair Jerome Powell and on tariffs against China. The perceived softening in tone has provided much-needed relief after weeks of heightened tension, leading to a reversal in safe-haven flows and helping risk assets stabilize.

In the currency space, European majors are lagging, with Euro and Pound among the worst performers of the day. This weakness partly reflects the broader pullback in safe-haven demand but is also driven by disappointing PMI services data. Both Eurozone and the UK saw service sector activity slip back into contraction. Conversely, Aussie and Kiwi are leading the pack, buoyed by the improved risk mood. Dollar is mixed—holding steady alongside Loonie and Yen. Traders are closely watching whether the recent dollar weakness has bottomed out.

One development that has raised eyebrows is the abrupt cancellation of a planned diplomatic meeting in London involving US Secretary of State Marco Rubio, European leaders, and Ukraine. The talks were meant to address an endgame to Russia’s war in Ukraine but were downgraded to a lower-level “technical” discussion after Rubio withdrew. Reports suggest sharp divisions between Washington and European allies, particularly over Trump’s proposals to recognize Russian control over Crimea and large parts of eastern Ukraine—conditions deemed unacceptable by Europe. Observers suggest this could mark a significant shift in US posture, from active mediator to a more unilateral stance, further straining transatlantic cohesion over the handling of the war in Ukraine.

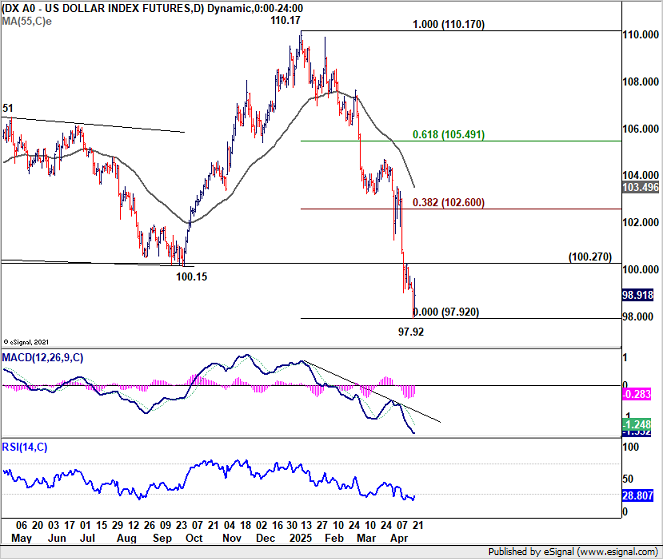

Technically, the focus of Dollar Index will be on 100.27 resistance in coming days. Firm break there should confirm short term bottoming at 97.92, and open up further rebound back to 38.2% retracement of 110.17 to 97.92 as a corrective move. However, before that, risk will stay on the downside for extending recent decline through 97.92 sooner rather than later.

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 2.45%. CAC is up 2.07%. UK 10-year yield is down -0.054 at 4.506. Germany 10-year yield is up 0.028 at 2.476. Earlier in Asia, Nikkei rose 1.89%. Hong Kong HSI rose 2.37%. China Shanghai SSE fell -0.10%. Singapore Strait Times rose 0.97%. Japan 10-year JGB yield rose 0.013 to 1.324.

UK PMI composite plunges to 48.2, recession fears, pressures BoE to cut rates

The UK private sector contracted sharply in April, with the flash PMI Composite falling from 51.5 to 48.2, the lowest reading in 29 months. PMI Manufacturing dropped from 45.3 to 44.0, a 20-month low. PMI Services slipped from 52.5 to 48.9, the weakest in 27 months.

According to S&P Global’s Chris Williamson, the downturn marks the steepest fall in output in nearly two and a half years, with data now pointing to a potential quarterly GDP decline of -0.3%.

Also, business sentiment has sunk to its lowest level since late 2021, and even beneath the post-Brexit vote lows. The slump in exports, tied to weak global demand and escalating trade tensions, is adding to domestic burdens. Rising staffing costs—partly due to changes in National Insurance and minimum wage rules—have further squeezed margins.

The sharp contraction and collapsing sentiment pose “red flags” for policymakers and could tip BoE toward cutting rates at its upcoming May meeting.

Eurozone PMI Composite slips to 50.1, services contract but manufacturing unfazed by tariffs

Eurozone economy showed signs of stagnation in April as its Composite PMI slipped to 50.1, down from 50.9 in March—a four-month low. The decline was driven primarily by a downturn in the services sector, which contracted for the first time in five months, with the PMI falling from 51.0 to 49.7. In contrast, manufacturing showed unexpected resilience, with PMI ticking up slightly from 48.6 to 48.7, reaching a 27-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that manufacturers appear “not too fazed” by the recent imposition of broad US tariffs, including 10% general duties and 25% on autos.

He pointed to falling energy prices, driven in part by US recession fears, and planned increases in defence spending as factors supporting the manufacturing sector. However, the decline in services activity has dragged down overall output, pushing the Eurozone economy into what de la Rubia called “stagnation territory.”

ECB may find some comfort in the latest inflation signals. While input costs in services remained elevated, the pace of selling price increases eased. In the goods sector, input prices fell, breaking a four-month trend of rising costs, while output prices saw only a modest rise.

At the country level, both Germany and France mirrored the regional trend, with manufacturing output gaining but services activity declining.

Japan’s PMI composite rises to 51.1, service leads while manufacturing drags

Japan’s flash PMI data for April signaled a return to growth in the private sector, with Composite PMI rising from 48.9 to 51.1. The recovery was driven primarily by a rebound in the services sector, where activity rose to 52.2 from 50.0. Meanwhile, manufacturing remained in contraction, though the pace of decline eased slightly, with the PMI inching up from 48.4 to 48.5.

According to S&P Global’s Annabel Fiddes, the divergence between sectors reflected subdued factory output versus strengthening service demand.

A closer look at new business trends revealed further divergence. Manufacturers reported the sharpest drop in new orders in over a year, driven by falling foreign demand and persistent concerns over tariffs and client spending. In contrast, service providers saw their strongest rise in new work since January.

Still, inflationary pressures were strong across the board, with input costs rising at the fastest pace in two years, prompting firms to pass on those costs to customers via higher selling prices.

Overall optimism for output over the next year fell to its lowest level since August 2020, during the early phase of the COVID-19 crisis.

Australia’s PMI composite dips to 51.4, cost pressures emerge

Australia’s flash PMI data for April showed continued, albeit slower, expansion in the private sector, with Manufacturing PMI slipping from 52.1 to 51.7 and Services PMI easing from 51.6 to 51.4. The Composite PMI also declined slightly from 51.6 to 51.4.

Despite the modest pullback, S&P Global’s Jingyi Pan noted that domestic demand remained a “strong proponent” of business activity, supporting further job creation across sectors. The data suggests a solid start to Q2, underpinned by internal momentum, even as external headwinds mount.

However, the impact of US tariffs are starting to show. Export performance weakened, and manufacturers reported “intensification of cost pressures” due to currency fluctuations.

In response, many firms passed on higher costs to clients, pushing overall selling price inflation to a nine-month high.

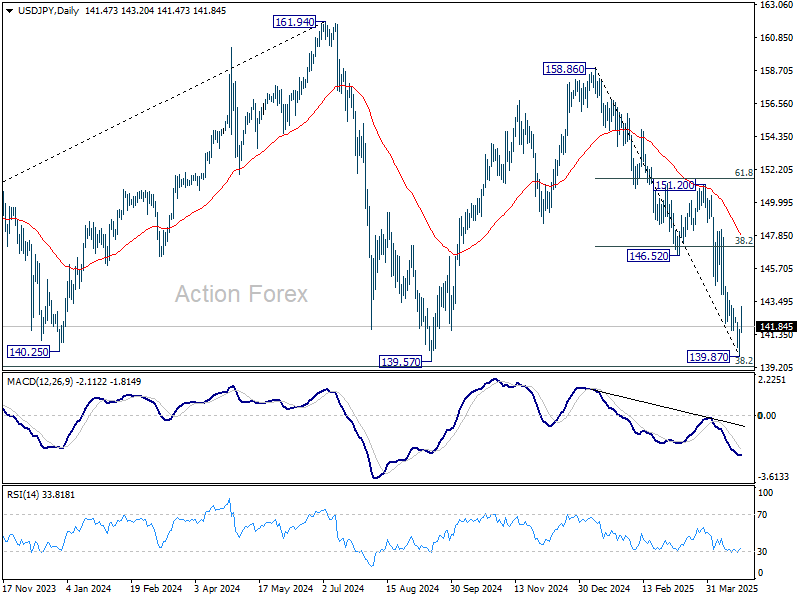

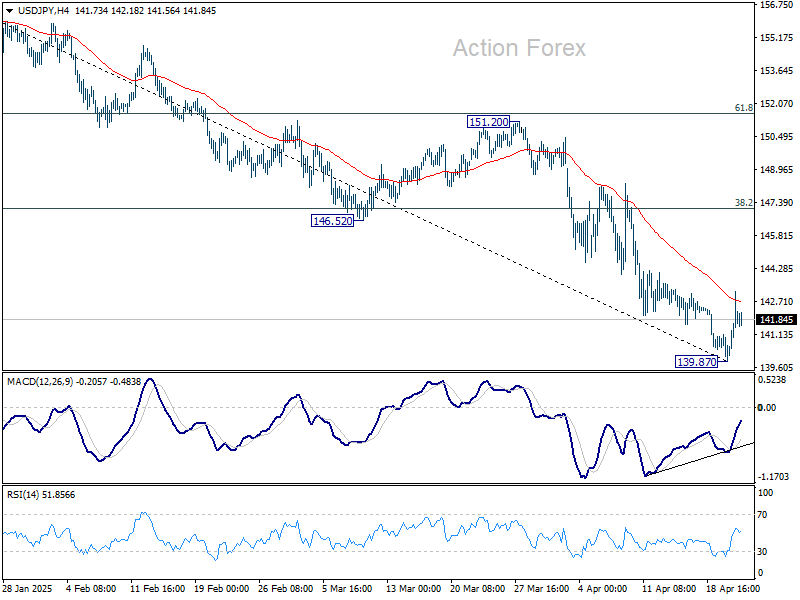

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 140.44; (P) 141.05; (R1) 142.22; More…

Intraday bias in USD/JPY remains mildly on the upside at this point. Rebound from 139.87 short term bottom could extend higher. But overall risk will stay on the downside as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, decisive break of 139.26 will carry larger bearish implications.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.