{kind=link}

Risk sentiment turned a bit subdued in Asia today. Markets are broadly soft, continuing to digest the sharp tariff-driven selloff seen earlier this month. Even China’s stronger-than-expected Q1 data, including a 5.4% GDP growth print and robust industrial and retail figures, failed to provide much lift. Market participants appear skeptical, viewing the numbers as a front-loading of activity ahead of the full brunt of US and China tariffs , which are already reaching decoupling levels. The real test for China’s resilience will come in the months ahead as trade disruptions deepen.

In the currency markets, Dollar is broadly weaker once again, giving back recent recovery as sentiment fluctuates. Aussie and Loonie are also underperforming. On the other hand, Swiss Franc has returned to the top of the board, followed by Euro and Yen, as investors rotate back into safer havens. Sterling and Kiwi are holding steady in the middle.

BoC rate decision later today is a major focal point, and markets are evenly split on the outcome. Yesterday’s softer-than-expected inflation data reinforced the view that February’s CPI spike was likely transitory, giving BoC room to cut rates from 2.75% to 2.50%. With US tariffs weighing on global demand and sentiment, a preemptive move to cushion the Canadian economy would be defensible.

However, some argue BoC may prefer to hold for now, especially to assess the medium-term inflationary effects of tariffs. While headline CPI is easing, trade-related supply disruptions and currency depreciation could generate renewed price pressures in the months ahead. Balancing these competing risks will be no easy task, and with the policy rate already cut sharply from its 5.00% peak, the central bank has room to wait for greater clarity.

Gold, meanwhile, continues to benefit from the uncertain backdrop, with prices pushing to new all-time highs. Technically, D MACD suggests that the up trend is still in upside acceleration phase. Near term outlook will stay bullish as long as 3167.60 resistance turned support holds. The question is whether overbought condition would cap upside at 161.8% projection of 2293.45 to 2789.92 from 2584.24 at 3387.52. Or Gold would just shoot through the roof.

In Asia, at the time of writing, Nikkei is down -1.36%. Hong Kong HSI is down -2.46%. China Shanghai SSE is down -0.63%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is down -0.052 at 1.323. Overnight, DOW fell -0.38%. S&P 500 fell -0.17%. NASDAQ fell -0.05%. 10-year yield fell -0.041 to 4.323.

BoJ’s Ueda: US tariffs nearing bad scenario, policy response may be needed

BoJ Governor Kazuo Ueda warned that US President Donald Trump’s escalating tariff policies have “moved closer towards the bad scenario” anticipated by the central bank.

“We will scrutinise without pre-conception the extent to which US tariffs could hurt the economy,” he said in an interview with Sankei newspaper.

“A policy response may become necessary. We will make an appropriate decision in accordance with changes in developments,” he added.

Nevertheless, Ueda reiterated that BoJ will continue to raise interest rates “at an appropriate pace” as long as economic and price conditions align with its projections.

On inflation, Ueda said domestic food price pressures are expected to ease. He sees real wages turning positive and continuing to rise into the second half of the year, supporting consumption and price stability.

Still, he warned of dual risks: persistent inflation driven by global supply shocks, or a consumption drag caused by the rising cost of living.

Australia Westpac leading index falls as tariff shock starting to weigh

Australia’s Westpac Leading Index slipped from 0.9% to 0.6% in March. Westpac noted that the index has only just begun to reflect the escalating disruptions caused by US President Donald Trump’s reciprocal tariff announcement on April 2.

While the immediate impact on Australia is seen as limited and manageable for now, “some further softening in the growth pulse looks likely in the months ahead”.

Westpac has revised down its growth forecast for Australia in 2025 to 1.9% from 2.2%, citing the accumulating downside risks.

Looking ahead to RBA’s May 19–20 meeting, Westpac expects the deteriorating global backdrop and clearer signs of inflation cooling will prompt a 25bps rate cut.

Moreover, the tone of the meeting is likely to pivot more decisively “away from lingering questions about inflation to downside risks to growth.” Such a shift would lay the groundwork for additional policy easing in the second half of the year.

China Q1 GDP tops forecasts with 5.4% growth

China’s economy started the year on a stronger footing, with GDP expanding by 5.4% yoy in Q1, surpassing market expectations of 5.1%. On a quarterly basis, growth slowed to 1.2% from 1.6% in Q4.

March’s activity indicators were broadly upbeat. Industrial production surged by 7.7% yoy, well above the 5.6% yoy forecast. Retail sales climbed 5.9%, also ahead of expectations of 5.1% yoy.

Fixed asset investment increased 4.2% year-to-date, modestly exceeding projections. However, persistent weakness in the property sector continues to weigh on the recovery narrative. Property investment fell -9.9% in Q1, slightly worse than the -9.8% decline recorded over the first two months of the year. Private sector investment—a key gauge of business confidence—rose only 0.4%.

Looking ahead

UK CPI and Eurozone CPI final are the main features in European session. Later in the day, US will release retail sales, industrial production and NAHB housing index. BoC rate deision will also be a major focus.

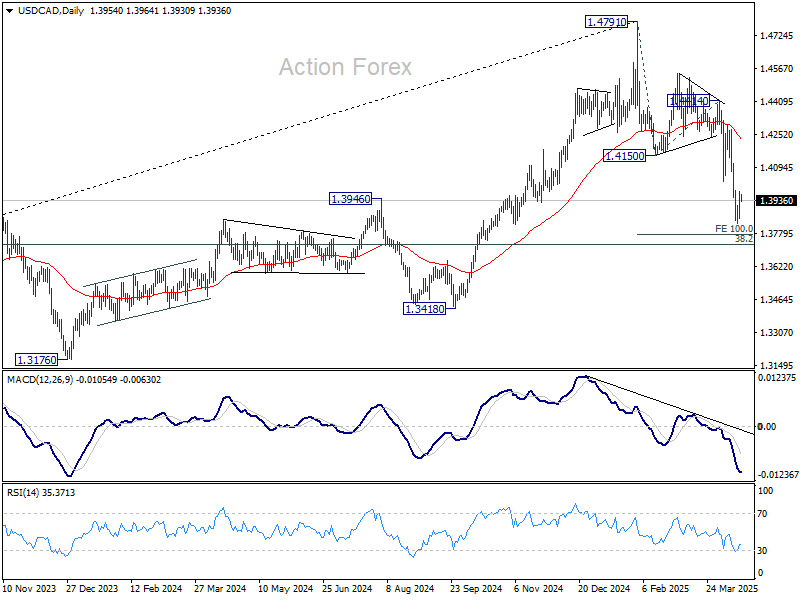

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3882; (P) 1.3930; (R1) 1.4010; More…

Intraday bias in USD/CAD remains neutral and more consolidations could be seen above 1.3827. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.4150 support turned resistance holds. On the downside, break of 1.3827 will resume the fall from 1.4791 to 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3983) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.