{kind=link}

Euro is trading on the softer side in relatively quiet markets today, weighed down by a fresh round of weak economic data. The sharp plunge in German and Eurozone ZEW economic sentiment, triggered largely by mounting uncertainty over US trade policy, has deepened concerns about the region’s growth outlook. Adding to the dovish tone, ECB’s latest bank lending survey revealed that credit standards tightened and corporate loan demand weakened further in Q1, even before the tariff-driven turmoil of early April. Together, these developments strengthen the case for another ECB rate cut when the Governing Council meets this Thursday.

Canadian Dollar is also under some pressure following the latest CPI data, which showed headline inflation slowing more than expected. Core measures, including trimmed and common CPI, also came in softer than forecast. The figures mark a welcome reversal from February’s surprise inflation spike and give BoC added flexibility to stay on hold at its policy meeting tomorrow. However, having already lowered rates from a peak of 5.00% to the current 2.75%, BoC may opt to preserve remaining policy ammunition while assessing the broader impact of US tariffs.

Overall in the currency markets, the New Zealand and Australian Dollars are leading gains for today, buoyed by stabilization in risk sentiment. Sterling is also firmer, as mixed UK labour market data is unlikely to derail BoE’s slow and steady approach to policy normalization. On the weaker end, the Swiss Franc is underperforming the most, followed by Loonie and Euro. Dollar and Yen are trading closer to the middle of the pack.

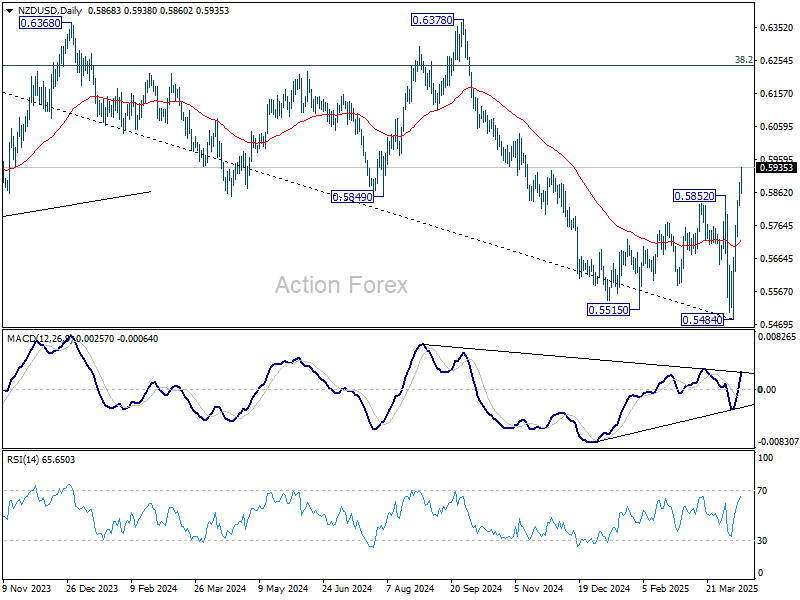

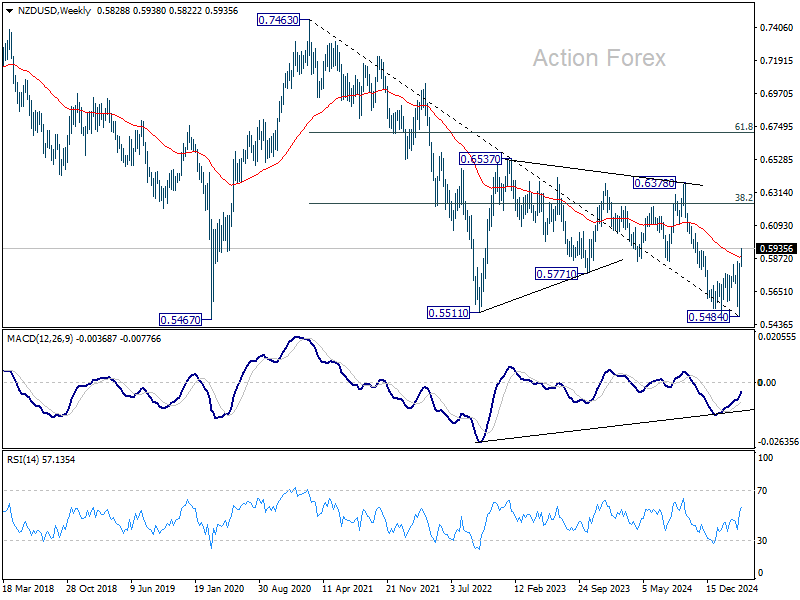

Technically, NZD/USD’s strong break of 0.5852 resistance this week firstly confirms short term bottoming at 0.5484. More importantly, the break of 55 W EMA also suggests that a medium term bottom was formed, just ahead of 0.5467 key support (2020 low). Rise from 0.5484 could now be heading back to 38.2% retracement of 0.7463 to 0.5484 at 0.6240, even as a corrective bounce.

In Europe, at the time of writing, FTSE is up 0.88%. DAX is up 0.98%. CAC is up 0.23%. UK 10-year yield is down -0.004 at 4.662. Germany 10-year yield is up 0.037 at 2.548. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI rose 0.23%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 2.14%. Japan 10-year JGB yield rose 0.035 to 1.376.

Canada’s CPI slows to 2.6%, CPI common down to 2.3%

Canada’s headline inflation cooled more than expected in March, with the annual CPI rate easing to 2.3% yoy from 2.6% yoy, below consensus forecasts for no change. The deceleration was largely driven by falling prices in travel-related services and gasoline. On a monthly basis, CPI rose 0.3% mom, undershooting expectations of a 0.7% mom increase.

Core inflation metrics also pointed to moderation. CPI median held steady at 2.9% yoy, in line with expectations. But the trimmed mean slipped to 2.8% yoy from 2.9% yoy, and the common core fell to 2.3% yoy from 2.5% yoy, both coming in below forecast.

German ZEW collapses to -14 as trade uncertainty rattles outlook

Investor confidence in Germany took a sharp turn for the worse in April, with ZEW Economic Sentiment Index plummeting from 51.6 to -14, its steepest decline since the onset of the Russia-Ukraine war in 2022.

The drop came in well below expectations of 10.6 and reflects mounting concerns over US trade policy, which ZEW President Achim Wambach described as marked by “erratic changes.” The Current Situation Index, however, showed a modest improvement, rising from -87.6 to -81.2, slightly better than forecast.

Eurozone also saw a significant deterioration in investor sentiment, with ZEW expectations gauge falling from 19.8 to -18.5, missing the anticipated 14.2 reading. Current Situation Index dropped by -5.7 points to -50.9.

According to ZEW, sectors most vulnerable to trade disruptions—such as autos, chemicals, and engineering—are now under renewed pressure, despite recent signs of stabilization. The growing unpredictability in global trade dynamics is weighing heavily on future expectations, dampening optimism across the bloc.

Despite the worsening sentiment, financial market participants do not foresee a renewed surge in inflation. This perception, ZEW notes, gives ECB some room to continue its easing cycle in an effort to support growth.

Eurozone industrial output surges in 1.1% mom in Feb, driven by consumer and capital goods

Eurozone industrial production posted a stronger-than-expected gain of 1.1% mom in February, well above the 0.1% mom forecast. The increase was largely driven by a 2.8% jump in non-durable consumer goods and a solid 0.8% rise in capital goods output. Intermediate goods also rose modestly by 0.3%, while energy production and durable consumer goods declined by -0.2% -and 0.3%, respectively.

Across the broader EU, industrial production rose 1.0% on the month, with Ireland (+10.8%), Belgium (+7.4%), and Luxembourg (+6.3%) leading the gains. Meanwhile, Croatia (-3.9%), Greece (-3.6%), and Romania (-2.1%) recorded the steepest declines.

UK payolled employment falls -78k, wage growth slows

UK payrolled employment falling -by 78k in March, down 0.3% mom. Median monthly pay growth also moderated to 4.8% yoy from 5.5% yoy, pointing to easing wage pressures. Meanwhile, claimant count rose by 18.7k, less than the expected 30.3k increase.

In the three months to February, unemployment rate held steady at 4.4%, in line with expectations. Wage growth came in slightly below forecasts across the board. Average earnings including bonuses rising 5.6% yoy (unchanged from the previous month) and those excluding bonuses up 5.9%, a touch softer than the anticipated 6.0% yoy.

RBA Minutes: Next rate move not predetermined, China’s tariff response a key variable

The minutes from RBA’s March 31–April 1 meeting revealed emphasized that it was “not yet possible to determine the timing of the next move in interest rates.” The Board emphasized the importance that the “next decision was not predetermined”.

Members agreed that the May meeting would offer a more “opportune time” for reassessment, as it would coincide with updated data on inflation, wages, employment, and global tariff developments, as well as a revised set of economic forecasts.

RBA highlighted that the economic outlook could be significantly shaped by how Chinese authorities respond to global tariff developments. Meanwhile, RBA acknowledged that risks to the outlook exist on both sides.

On one hand, global trade uncertainties and softening demand may pose disinflationary pressures, while on the other, risks such as supply chain disruptions and currency depreciation could fuel inflation.

RBA opted to keep the cash rate unchanged at 4.10% at the meeting.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1289; (P) 1.1357; (R1) 1.1418; More…

EUR/USD dips mildly today as consolidation continues below 1.1472. Deeper pull back might be seen but downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.