{kind=link}

Commodity currencies, including Australian, New Zealand, and Canadian Dollars, are trading broadly higher in today’s Asian session, buoyed by continued recovery in global stock markets. Sterling is also advancing alongside, supported by improving risk sentiment. Meanwhile, traditional safe havens like the Swiss Franc, Japanese Yen, are on the back, along with the greenback foot. Swiss Franc is particularly soft, pulling back after recent strong gains. Euro remains directionless in the middle of the pack, showing little inclination to break out against Dollar yet.

In RBA’s minutes policymakers explicitly citing China’s response as a pivotal factor shaping Australia’s economic outlook and, by extension, future rate decisions. Given that China remains the only major economy actively retaliating against US tariffs, the fallout from a protracted trade war could be particularly impactful for Australia. While some analysts read the RBA’s language as a signal that a rate cut may come as soon as May, the actual odds remain more evenly balanced than market consensus might suggest. Tomorrow’s Australian employment report could help clarify the picture, at least a little bit.

Fed Governor Christopher Waller’s speech is worth a read. It offered a structured view of the unfolding US tariff regime. Waller outlined two potential paths: one focused on reshoring manufacturing and reducing trade dependency—implying a prolonged period of elevated tariffs. The other, a route aimed at leveraging tariffs to negotiate lower trade barriers from other countries. The ultimate outcome hinges on the political objectives of the Trump administration. But in reality, the likely result may lie somewhere between those extremes.

Technically, Bitcoin is showing signs of stabilizing after its recent pullback. It remains well supported by 73812 cluster support (38.2% retracement of 15452 to 109571 at 73617) for now. Bullish convergence condition in D MACD is raising chance of a near term reversal. Firm break of 88769 resistance will argue that correction from 109571 has completed already, and the larger up trend remains intact. Retest of 109571 high should then be seen next.

In Asia, at the time of writing, Nikkei is up 0.96%. Hong Kong HSI is down -0.11%. China Shanghai SSE is down -0.17%. Singapore Strait Times is up 1.75%. Japan 10-year JGB yield is up 0.032 at 1.372. Overnight, DOW rose 0.78%. S&P 500 rose 0.79%. NASDAQ rose 0.64%. 10-year yield fell -0.129 to 4.364.

Fed’s Waller weighs two tariff paths

In a speech overnight, Fed Governor Christopher Waller laid out two divergent scenarios for US tariff policy and their economic fallout.

The first scenario assumes high tariffs, near average 25% or more, and remain in place for an extended period. This reflects a structural shift toward domestic production and reduced trade dependence. The second scenario envisions a negotiated reduction in foreign trade barriers, which would lower the average tariff rate back to around 10%, closer to the levels anticipated earlier this year.

Waller warned that if the “high-tariff” regime holds, the US economy is likely to “slow to a crawl” with inflation rising to around 4% before retreating in 2026, assuming inflation expectations remain anchored. In this scenario, the unemployment rate could climb toward 5% next year as business investment weakens under higher costs and persistent uncertainty.

In contrast, if the current pause in reciprocal tariffs leads to meaningful progress in trade negotiations and the easing of barriers, Waller expects a milder economic impact. Under this “smaller tariff” path, the economy would continue to grow—albeit at a slower pace—while inflation would likely stay on a downward trend toward Fed’s 2% target. In such a case, he said, rate cuts could be warranted later this year as a “good news” policy move.

Fed’s Bostic cautions against bold policy moves as trade fog stalls US economy

Atlanta Fed President Raphael Bostic warned that the Trump administration’s tariff measures and broader policy ambiguity have effectively pushed the economy into a “big pause,” making it difficult for the Fed to chart a clear policy path.

Bostic emphasized that this uncertainty argues against any aggressive policy shifts in either direction. “Moving too boldly with our policy in any direction wouldn’t be prudent.” He likened the current climate to a “really, really thick” fog that hampers effective decision-making.

On the inflation front, Bostic acknowledged that tariffs are likely to exert upward pressure on prices. He now sees inflation returning to that level no sooner than 2027, well beyond previous expectations.

Bostic also anticipates that economic growth will decelerate sharply, with GDP expanding just above 1% this year—less than half the pace seen in recent years.

RBA Minutes: Next rate move not predetermined, China’s tariff response a key variable

The minutes from RBA’s March 31–April 1 meeting revealed emphasized that it was “not yet possible to determine the timing of the next move in interest rates.” The Board emphasized the importance that the “next decision was not predetermined”.

Members agreed that the May meeting would offer a more “opportune time” for reassessment, as it would coincide with updated data on inflation, wages, employment, and global tariff developments, as well as a revised set of economic forecasts.

RBA highlighted that the economic outlook could be significantly shaped by how Chinese authorities respond to global tariff developments. Meanwhile, RBA acknowledged that risks to the outlook exist on both sides.

On one hand, global trade uncertainties and softening demand may pose disinflationary pressures, while on the other, risks such as supply chain disruptions and currency depreciation could fuel inflation.

RBA opted to keep the cash rate unchanged at 4.10% at the meeting.

Looking ahead

Germany ZEW economic sentiment, and Eurozone industrial production will be featured in European session. Later in the day, main focus is on Canada CPI. US will release Empire state manufacturing and import prices.

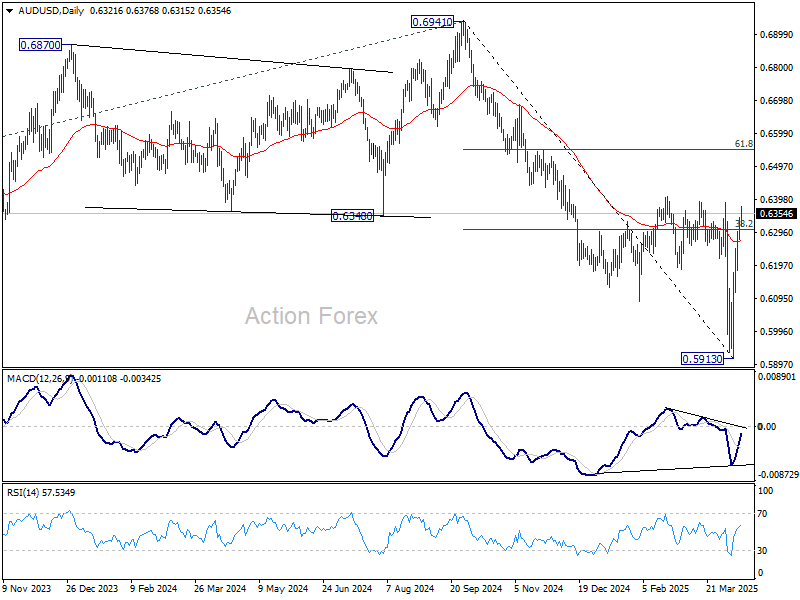

AUD/USD Daily Report

Daily Pivots: (S1) 0.6287; (P) 0.6315; (R1) 0.6355; More...

AUD/USD’s rally from 0.5913 is still in progress and intraday bias stays on the upside. Firm break of 0.6407 resistance will pave the way to 61.8% retracement of 0.6941 to 0.5913 at 0.6548, even still as a corrective move. On the downside, below 0.6180 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6441) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.