{kind=link}

The global financial markets are enjoying a modest recovery today, with gains seen across Asia and Europe. US futures also point to a higher open, suggesting the bounce from last week’s dramatic selloff are having further legs. News flow is relatively light, with no major economic data releases, and tariff headlines have also slowed. The next big development on that front is expected to involve semiconductors, but traders will have to wait for details. In the meantime, markets appear to be taking a breather from the chaos.

Several Fed officials are due to speak today, though they are unlikely to provide fresh forward guidance given the highly fluid environment. Fed has so far emphasized the need for patience and data dependence, and that message is likely to be reinforced.

In the currency markets, Swiss Franc is underperforming as risk sentiment stabilizes, followed by Loonie and then Dollar. Sterling leads the day, buoyed by its risk-sensitive nature, while Kiwi and Aussie are also firm. Euro and Yen are relatively steady in the middle of the pack.

Looking ahead, RBA meeting minutes in the upcoming Asian session will be closely watched. The minutes may reiterate that the previous rate cut doesn’t necessarily start a new easing cycle. But the views may already be somewhat outdated, as the meeting occurred just before the US reciprocal tariff announcement and the subsequent market chaos. Still, they could offer insights into whether RBA board is leaning more toward inflation control or concerned about downside growth risks.

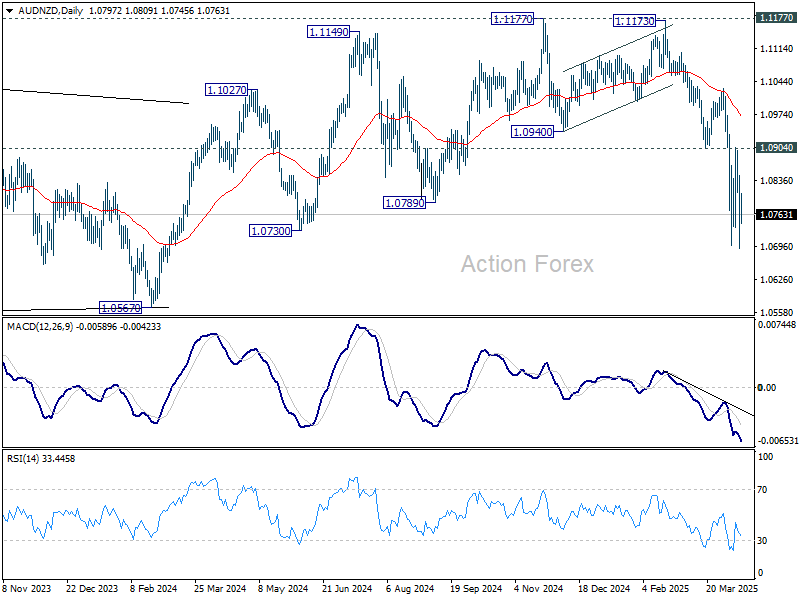

Technically, Aussie remains under pressure. It’s the second-worst performer for the month, trailing only Dollar. Technically, while some extraordinarily volatility was even seen in AUD/NZD, near term outlook stays bearish with 1.0904 support turned resistance intact. Fall from 1.1177 is expected to continue to 1.0567 key medium term support next.

In Europe, at the time of writing, FTSE is up 1.78%. DAX is up 2.56%. CAC is up 2.24%. UK 10-year yield is down -0.102 at 4.665. Germany 10-year yield is down -0.051 at 2.523. Earlier in Asia, Nikkei rose 1.18%. Hong Kong HSI rose 2.40%. China Shanghai SSE rose 0.76%. Singapore Strait TImes rose 1.04%. Japan 10-year JGB yield fell -0.005 to 1.341.

OPEC trims 2025 oil demand outlook, WTI recovers mildly

OPEC has cut its forecast for global oil demand growth in 2025, now expecting an increase of 1.30m barrels per day, down -150k bpd from last month’s estimate.

In its latest monthly report, the group also lowered its projections for world economic growth for both 2024 and 2025, citing mounting uncertainties surrounding international trade policy and rising tariff tensions.

“The global economy showed a steady growth trend at the beginning of the year, however, recent trade-related dynamics have introduced higher uncertainty to the short-term global economic growth outlook,” OPEC noted.

WTI crude oil recovers mildly today. But overall development suggests that it’s still in consolidations above last week’s low at 55.20. Outlook will stay bearish as long as 65.24 cluster resistance holds (38.2% retracement of 81.01 to 55.20 at 65.05 holds. Larger down trend is still in favor to resume through 55.20 at a later stage.

BoJ’s Ueda: US tariffs add downside risks to Japan through various channels

BoJ Governor Kazuo Ueda warned today that the recently imposed U.S. tariffs are likely to exert “downward pressure” on both the global and Japanese economies through “various channels.”

While he did not specify the transmission mechanisms, the remarks reflect growing concerns that escalating trade tensions could weigh on exports, dampen corporate sentiment, disrupt supply chains, as well as trigger volatility in the financial markets including currencies.

Ueda reiterated BoJ’s commitment to achieving its 2% inflation target sustainably, noting that monetary policy would be guided appropriately based on evolving economic, price, and financial developments. He emphasized that the central bank will maintain a data-dependent approach and continue to scrutinize conditions “without any pre-conception”.

NZ BNZ services rises to 49.1, subdued despite hints of stabilization

New Zealand’s services sector remained in contraction in March, with the BusinessNZ Performance of Services Index inching up slightly to 49.1 from 49.0. This marks another month below the long-run average of 53.0 highlighting the ongoing weakness.

While the headline improvement was minimal, underlying components showed a mixed picture—activity/sales dropped from 49.1 to 47.4. But new orders/business climbed from 49.5 to 50.8, the highest since February 2024, suggesting some pickup in future demand. Employment rose from 49.1 to 50.2, ending a 15-month streak of contraction, and offering early signs that firms may be regaining confidence in hiring.

The share of negative comments from survey participants fell slightly to 56.7%, with ongoing concerns about high interest rates, inflation, weak consumer sentiment, and broader economic uncertainty. Businesses also cited external pressures such as global tariffs and rising input costs.

China’s export surge 12.4% yoy in Mar, imports down -4.3% yoy

China’s exports jumped an impressive 12.4% yoy to USD 313.9B in March, significantly beating expectations of 4.4% yoy and marking a sharp acceleration from the 2.3% yoy growth recorded in January-February.

Particularly notable was the 9.18% yoy rise in shipments to the US, likely due to front-loading ahead of tariff tensions. Exports to ASEAN also strengthened with 11.6% yoy growth , with double-digit growth to major partners like Thailand (27.8% yoy) and Vietnam (18.9% yoy).

However, Vietnam, a key intermediary in China’s export supply chain, is now under pressure to tighten controls on the origin of goods and materials. According to a ministry document, authorities in Hanoi are urging companies to clamp down on origin fraud to avoid punitive US tariffs, highlighting growing scrutiny on Chinese goods routed through third countries.

Meanwhile, the strength in exports contrasted with a -4.3% yoy decline in imports, resulting in a larger-than-expected trade surplus of USD 102.6B.

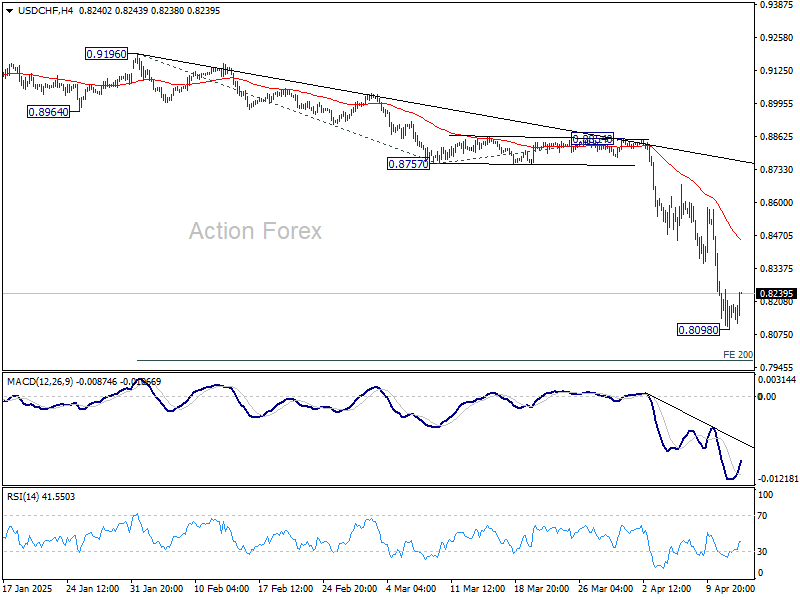

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8079; (P) 0.8173; (R1) 0.8246; More…

A temporary low is formed at 0.8098 in USD/CHF with current recovery. Intraday bias is turned neutral first for consolidations. While stronger rise might be seen, upside should be limited by 55 4H EMA (now at 0.8449) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.