{kind=link}

Financial markets showed signs of stabilization since European session, despite another round of retaliatory tariff hikes from China. While the latest move saw China raise levies on US goods to 125% from 84%, the response was widely anticipated and thus well absorbed by investors. Both President Donald Trump and President Xi Jinping have maintained uncompromising stances, so markets had largely priced in another step in the tit-for-tat trade war. The absence of any conciliatory tone keeps tensions high, but the predictability of the escalation appears to have dulled the market impact.

Also, China’s latest move may have reached a symbolic peak. In a strongly worded statement, China’s finance ministry noted that at current tariff levels, “there is no longer a market for US goods imported into China,” implying that further retaliation may be economically futile. “If the U.S. government continues to increase tariffs on China, Beijing will ignore,” it added.

Some of the bearish sentiment from the US-China standoff is being offset by more constructive developments on other trade fronts. Negotiations between the US and both the European Union and Japan appear to be gaining traction. EU trade commissioner Maroš Šefčovič is scheduled to visit Washington on April 14 to meet US officials and continue discussions on tariff matters. Meanwhile, Japan’s newly formed task force, led by Economy Minister Ryosei Akazawa, is preparing for key meetings on April 17 with US Treasury and trade representatives.

Despite the stabilization in broader risk sentiment, Dollar continues to bleed, extending a week-long selloff and positioning itself as the worst performer among major currencies. Sterling is tracking as the second weakest despite a strong UK GDP report. Loonie follows closely behind, pressured by declining oil prices and general risk aversion.

Swiss Franc stands out as the week’s clear winner, underpinned by its status as the undisputed safe-haven, while Kiwi and Euro are also among the strongest performers. Aussie and Yen are positioning in the middle.

Eyes are now on the University of Michigan consumer sentiment report. Any significant surprises in that data could prompt a final reshuffling of currency rankings before markets settle for the weekend.

In Europe, at the time of writing, FTSE is up 0.50%. DAX is down -1.26%. CAC is down -0.45%. UK 10-year yield is up 0.048 at 4.699. Germany 10-year yield is down -0.067 at 2.516. Earlier in Asia, Nikkei fell -2.96%. Hong Kong HSI rose 1.13%. China Shanghai SSE rose 0.45%. Singapore Strait Times fell -1.83%. Japan 10-year JGB yield fell -0.031 to 1.346.

US PPI unexpectedly falls -0.3% mom in March

US producer prices posted a surprise decline in March, with the headline PPI for final demand falling -0.4% mom, well below expectations of a 0.2% mom rise.

The drop was driven largely by a -0.9% mom decline in final demand goods, while final demand services also slipped -0.2% mom.

On an annual basis, PPI slowed to 2.7% year-on-year from 3.2%, also below forecasts.

PPI excludes food, energy, and trade services, rose just 0.1% mom on the month, with the year-on-year rate at 3.4%.

EU’s Dombrovskis: Existing tariffs enough to shave up to 1.4% off US GDP, hit EU by 0.2%

EU Economy Commissioner Valdis Dombrovskis acknowledged the US decision to pause reciprocal tariffs above 10% for 90 days as a positive step that opens the door to negotiations. However, he cautioned that the existing 10% duties still in place on nearly all countries continue to weigh on the global economy. Additionally, the US has not lifted its 25% tariffs on steel, aluminum, cars, and car parts—measures that remain a significant source of transatlantic economic tension.

Dombrovskis pointed to a model simulations indicating that the current US tariff structure could reduce US GDP by 0.8% to 1.4% through 2027. While the economic fallout for the EU is expected to be milder—around 0.2% of GDP—he warned that the damage could escalate dramatically if tariffs become entrenched or retaliatory actions intensify.

Under such a worst-case scenario, Dombrovskis said US GDP could fall by as much as 3.3%, with the EU losing up to 0.6% and global GDP shrinking by 1.2%. The impact on global trade would be particularly severe, with an estimated contraction of 7.7% over the next three years.

UK GDP rises 0.5% mom in Feb, broad-based growth

The UK economy delivered a strong upside surprise in February, with GDP expanding by 0.5% mom, far exceeding market expectations of just 0.1% mom. All three major sectors contributed to the growth: services rose by 0.3% mom, production surged by 1.5% mom, and construction edged up 0.4% mom.

On a three-month rolling basis, real GDP grew by 0.6% to February 2025 compared to the previous three months, driven largely by a 0.6% rise in services output and a 0.7% gain in production. Construction, however, was flat over the period.

NZ BNZ manufacturing falls to 53.2, new orders signal trouble ahead

New Zealand’s BusinessNZ Performance of Manufacturing Index slipped slightly from 54.1 to 53.2 in March, but remained firmly in expansion territory. Production climbed to 54.2, the highest level since December 2021. Employment also posted a robust 54.7, marking its strongest result since mid-2021. However, a decline in new orders, which dipped below the 50-neutral mark to 49.6, raises concerns about the durability of this rebound.

BusinessNZ’s Catherine Beard acknowledged the resilience in activity and employment, but highlighted persistent challenges. Despite improving sentiment, nearly 58% of surveyed manufacturers cited negative conditions, pointing to weak demand, fewer new orders, and uncertainty across both domestic and export channels.

BNZ Senior Economist Doug Steel noted that the PMI data supports the case for manufacturing GDP growth in early 2025. Still, he cautioned that risks to the outlook are clearly tilted to the downside, “given recent extreme volatility on global markets following rapidly evolving US-driven trade policy changes.”

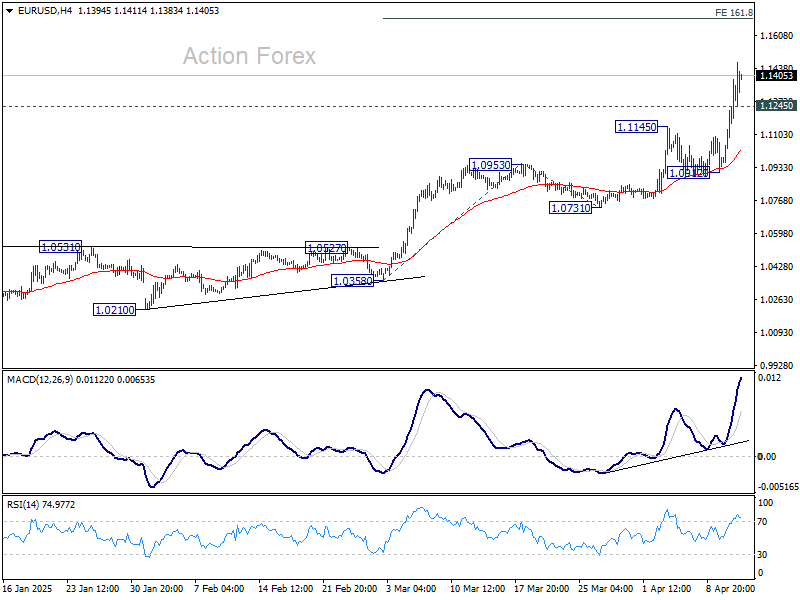

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1129; (R1) 1.1315; More…

EUR/USD’s rally is still in progress and intraday bias stays on the upside. Current rise form 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694. On the downside, below 1.1245 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well above 1.0912 support to bring another rally.

In the bigger picture, break of 1.1274 (2024 high) indicates resumption of whole up trend from 0.9534 (2022 low). Next target is 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 55 D EMA (now at 1.0745) holds.