{kind=link}

The relentless selling pressure in global markets shows no sign of abating, with European stocks and US futures once again under fire today. China’s latest retaliatory move to hike tariffs on US goods from 34% to 84% has reignited investor fears, just as the US implemented its own increase to a staggering 104% on Chinese imports. The ongoing trade war escalation between the world’s two largest economies is now moving rapidly from trade tension to a global financial shock.

China is clearly signaling it has no intention of backing down. Beyond higher tariffs, Beijing’s commerce ministry added multiple US entities to an export control list and labeled several more as “unreliable.” It also filed a pointed complaint with the WTO, accusing Washington’s “reckless move” of destabilizing global trade.

An unusual element of this market meltdown is the rare simultaneous collapse of all major US assets: stocks, Dollar, and Treasuries. In particular, yields on the 10-year note have surged back above 4.4%, up from 3.9% just last week. This sharp move has sparked fears of forced liquidation, margin calls on leveraged positions, which could drastically tighten up liquidity in the markets.

Market watchers have floated multiple theories as explanations for the sudden jump in yields. Some see it as a predictable consequence of the US push to reduce bilateral trade imbalances, which may curb or even reverse foreign demand for American debt. Besides, Treasuries could become a retaliatory tool in a geopolitical standoff. While each theory differs in detail, all point to an erosion of liquidity and confidence in a market once considered the bedrock of global finance.

Technically, 10-year yield’s break above 4.387 resistance is alarming. It suggests that fall from 4.809 has completed as a three-wave corrective move at 3.886. Risk will now stay heavily on the upside as long as 55 D EMA (now at 4.321) holds. Further rally could be seen back to 4.809 resistance. Firm break there could pave the way back to 4.997 high.

In the currency markets, Dollar is again the worst performer of the day. Sterling and Kiwi trail close behind, the latter pressured further by RBNZ’s rate cut and its dovish forward guidance. Yen and Swiss Franc are once again the preferred safe havens, with the Aussie showing surprising resilience—likely more a pause in its decline than a sign of strength. Euro and Loonie sit somewhere in the middle.

At the time of writing, FTSE is down -3.57%. DAX is down -4.03%. CAC is down -4.07%. UK 10-year yield is up 0.199 at 4.818. Germany 10-year yield is down -0.005 at 2.622. Earlier in Asia, Nikkei fell -3.93%. Hong Kong HSI rose 0.68%. China Shanghai SSE rose 1.31%. Singapore Strait Times fell -2.18%. Japan 10-year JGB yield rose 0.003 to 1.282.

ECB’s Villeroy: Trade uncertainty threatens financial stability, strengthens case for rate cut

French ECB Governing Council member Francois Villeroy de Galhau warned today that mounting economic uncertainty from escalating trade tensions is posing risks to financial stability, particularly increasing credit risks for some financial institutions.

While he emphasized the resilience of French banks, he noted that leveraged hedge funds could come under significant liquidity pressure.

Writing in his annual letter to President Macron, Villeroy assured that both Bank of France and ECB are “fully mobilised” to safeguard financial stability and ensure adequate liquidity.

Speaking to journalists, Villeroy said the recent US announcement of sweeping “reciprocal” tariffs only adds to the case for further monetary easing. “We still have room to cut rates,” he stated.

ECB’s Knot: Trade war a stagflationary shock, inflation impact will rise over time

Dutch ECB Governing Council member Klaas Knot warned today that the escalating trade war constitutes a “negative supply shock” and should be considered “stagflationary” in nature.

Knot also cautioned that as time progresses, the economic impact is more likely to “more inflationary rather than deflationary”.

ECB’s priority, he said, is to monitor how and when these tariffs start to meaningfully affect economic activity and corporate decision-making. However, next week’s policy meeting would be too soon to revise projections.

Knot also noted that despite the growing market stress, financial market functioning has so far been “preserved”. He credited the hedge fund sector’s proactive deleveraging for this resilience, saying they were well-prepared for the turbulence and capable of meeting margin calls—unlike in past market episodes.

BoJ’s Ueda: Rate hikes still on table, but trade uncertainty clouds outlook

BoJ Governor Kazuo Ueda reaffirmed today that the central bank remains open to further rate hikes if Japan’s economic recovery continues as projected. He added that current trends in both the economy and inflation are “roughly in line” with BoJ’s forecasts.

He added that the policy board will make decisions with a “without pre-conception” mindset, and assess whether the outlook materializes as expected.

However, Ueda flagged growing concerns over trade developments globally, warning of “heightening uncertainty over developments in each country’s trade policy”.

“We need to pay due attention to risks,” he warned.

RBNZ cuts 25bps, trade barriers as downside risk to both growth and inflation

RBNZ delivered a widely expected 25bps cut in the Official Cash Rate, bringing it to 3.50%. The policy statement highlighted that the recently announced global trade barriers create “downside risks to the outlook for economic activity and inflation” in New Zealand.

The central bank noted that with inflation close to the midpoint of its target range, it is in the “best position” to respond to economic shifts. RBNZ added it has “has scope to lower the OCR further as appropriate”, depending on how the impact of tariffs evolves.

This leaves the door wide open for further easing, particularly if global economic headwinds intensify or domestic data disappoints.

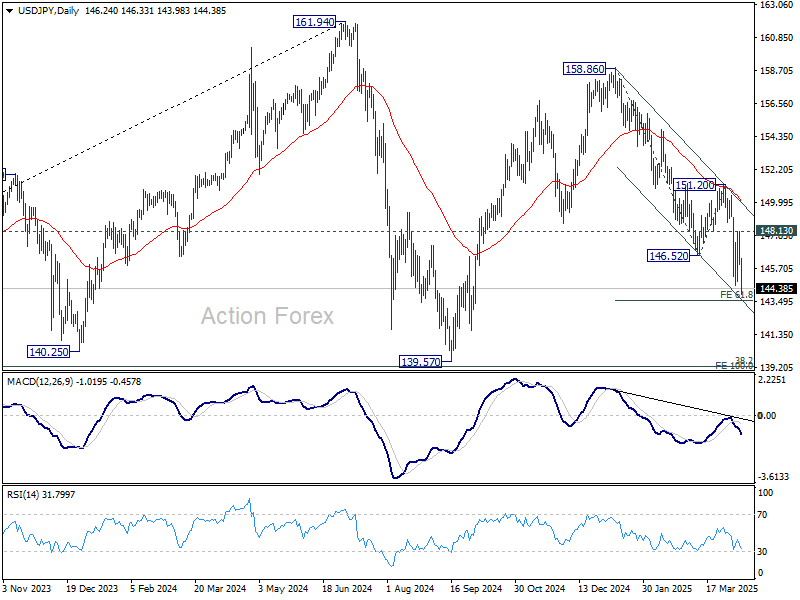

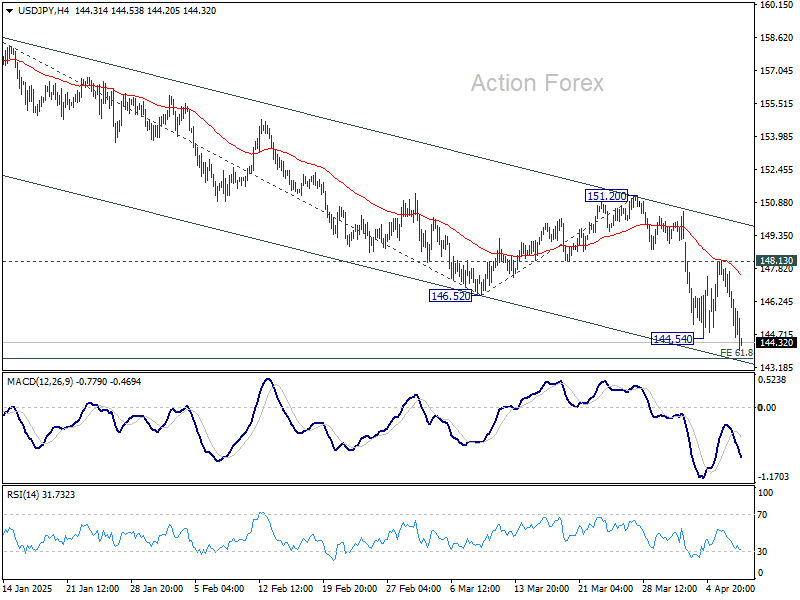

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.46; (P) 146.79; (R1) 147.61; More…

Intraday bias in USD/JPY is back on the downside with break of 144.54 support. Fall from 158.86 is resuming to 158.86 to 146.52 from 151.20 at 143.57. Break there will target 139.57 low. On the upside, break of 148.13 resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.